Most people don’t struggle with money because they’re bad at math. They don’t struggle because they picked the wrong budgeting app. And they usually don’t struggle because they lack intelligence. In my experience, the biggest reason people struggle financially is because they don’t have a system.

Instead, they have bits and pieces of advice collected from all over the place. They hear one thing from TikTok, another from YouTube, another from their neighbor, and something completely different from a financial podcast. Before long, they’re trying to follow five different strategies at once and wondering why they still feel stuck.

The truth is that financial success rarely comes from finding the perfect investment, the perfect budgeting app, or the perfect money hack. It comes from having a repeatable process that helps you make good decisions consistently over time. That’s what separates people who feel in control of their finances from people who constantly feel stressed about money.

The good news is that building a financial system doesn’t have to be complicated. In fact, most successful financial plans are surprisingly simple. They focus on understanding where you are today, identifying what needs improvement, creating systems that work automatically, and staying focused on long-term goals.

That’s exactly what this 90-day financial plan is designed to do. Whether you’re trying to save more, invest more effectively, reduce debt, prepare for retirement, or simply feel more confident about your finances, this framework can help you create momentum over the next three months and beyond.

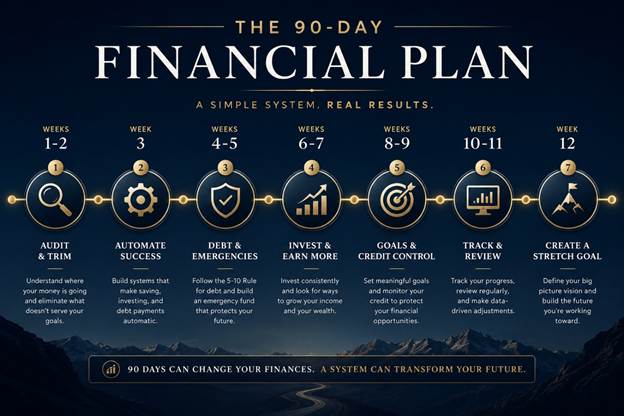

Weeks 1 and 2: Audit and Trim

The first step in any financial plan is understanding where you are today. It sounds simple, but this is where many people get stuck. They know they make money. They know they spend money. But they don’t really know where that money is going.

It doesn’t matter whether you have $5,000, $500,000, or $5 million. Before you can improve your financial situation, you need an honest assessment of your current reality. Think of it like taking a road trip. If you don’t know where you’re starting, it’s impossible to map out the best route to your destination.

When I talk about auditing your finances, I’m talking about understanding your financial habits. How much income comes into your household each month? How much are you spending? What percentage are you saving? Where are your largest expenses? What subscriptions, memberships, or recurring charges are quietly draining money from your accounts every month?

I recently met with a client who hopes to retire at the end of this year. Before we could determine whether retirement was realistic, we had to understand exactly what his spending looked like. The problem was that he had never really tracked it. He knew roughly what he spent, but “roughly” isn’t good enough when you’re making a major financial decision.

That’s why the audit matters. It creates awareness. Once you understand your current situation, you can start making intentional decisions rather than guessing.

After the audit comes the trim. This doesn’t mean eliminating everything you enjoy. It means making sure your money is being directed toward things that actually matter to you.

You may discover streaming services you never use. You may find subscriptions you forgot existed. You may notice spending habits that no longer align with your goals. The objective isn’t to become cheap. The objective is to make sure every dollar has a purpose.

Once you know where your money is going, you can start directing it toward where you want your life to go.

Week 3: Automate Your Success

One of the biggest lessons I’ve learned over the years is that systems beat discipline.

Most people believe they’ll save more money when they become more disciplined. The problem is that life gets busy. Work gets hectic. Kids have activities. Unexpected expenses pop up. Before long, the things we intended to do financially get pushed to the side.

Several years ago, our firm experienced a period of rapid growth. One of our advisors left, and I inherited approximately 100 additional client relationships while continuing to serve my existing clients. My schedule became packed almost overnight.

Like many people, I found myself focusing on everyone else’s needs while my own finances slipped into the background. I had cash sitting in accounts that wasn’t invested. I had money accumulating in my checking account that should have been working harder for me. I intended to move money regularly, but I simply didn’t always get around to it.

The solution wasn’t trying harder. The solution was automation.

I created automatic transfers from my bank account into my investment accounts. Those contributions were then invested automatically. Once the system was in place, everything worked exactly the way it should, whether I was thinking about it or not.

That’s the power of automation.

If you’re serious about improving your finances, look for opportunities to automate:

- Retirement contributions

- Investment deposits

- Emergency fund savings

- Debt payments

- College savings contributions

- Monthly transfers to brokerage accounts

The amount doesn’t matter nearly as much as consistency. Whether you’re saving $100 per month or $10,000 per month, automation helps remove emotion and inconsistency from the process.

When your financial system operates automatically, your money keeps moving forward even when life gets busy.

Weeks 4 and 5: Debt and Emergencies

This is the part of financial planning that most people prefer to ignore.

Nobody enjoys thinking about what happens if they lose their job. Nobody wants to think about a major medical event, a roof replacement, a transmission failure, or an unexpected emergency. Unfortunately, avoiding those possibilities doesn’t make them disappear.

If you want financial freedom, you need a plan for things going wrong.

One framework I often share is what I call the 5-10 Rule. It’s a simple way to think about debt and prioritize where your money should go.

If your debt carries an interest rate below 5%, I generally wouldn’t rush to pay it off. Many savings accounts, money market funds, and conservative investments can generate returns that are reasonably competitive with those borrowing costs. In many cases, your money may be better used building savings and investments.

Debt between 5% and 10% falls into a gray area. This is where personal preference and overall financial circumstances start to matter. Some people may choose to pay it off aggressively. Others may prioritize investing or liquidity.

Once debt climbs above 10%, my opinion becomes much stronger. High-interest debt can become a major obstacle to wealth creation. Every year that debt remains outstanding, it continues working against you.

Imagine carrying $50,000 of debt at 10%. That’s approximately $5,000 per year in interest alone. Before you can invest, save, or build wealth, you’re paying that interest bill.

The higher the interest rate rises, the more difficult it becomes to make meaningful financial progress.

At the same time, make sure you’re building emergency reserves. An emergency fund isn’t exciting. It won’t make headlines. It won’t impress your friends. But it may be one of the most important financial tools you ever create.

A strong emergency fund provides options. It gives you flexibility. It allows you to navigate life’s unexpected challenges without immediately turning to debt.

Weeks 6 and 7: Investing and Earning More

One of the biggest mistakes people make is believing that investing is something they’ll worry about later.

They tell themselves they’ll start investing when they make more money. They’ll start investing after they get a promotion. They’ll start investing after they pay off a certain debt.

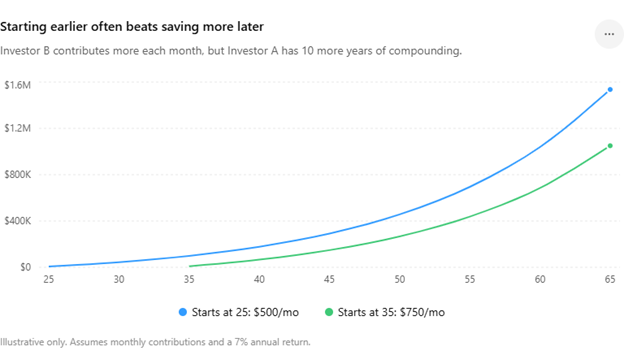

The problem is that time is one of the most valuable assets an investor has.

Someone who starts investing earlier often accumulates significantly more wealth than someone who starts later, even if the later investor contributes more money. That’s the power of compounding. Your money isn’t just growing. It’s growing on top of previous growth.

That’s why getting started matters so much.

You don’t need to have everything figured out. You don’t need a perfect strategy. You simply need to begin.

At the same time, I encourage people to think beyond just saving more. They should also think about earning more.

Many people spend years looking for ways to save an extra $50 per month while ignoring opportunities to increase their income by hundreds or thousands of dollars per year. Sometimes the greatest financial improvement comes from negotiating compensation, improving skills, changing jobs, growing a business, or finding better financial products.

I also encourage investors to be careful about concentrated positions. As someone who helps oversee hundreds of millions of dollars for clients, I generally believe most investors are better served by diversified investments rather than trying to hit a home run with a single stock.

A broad ETF or mutual fund provides exposure to hundreds or even thousands of companies. That diversification can reduce risk while still allowing investors to participate in long-term market growth.

Investing doesn’t have to be complicated. It simply needs to be consistent.

Weeks 8 and 9: Goal Setting and Credit Control

Many people think goal setting is unnecessary. Ironically, some of the most successful people I know take goal setting very seriously.

I have a client worth over $17 million who reviews his goals every single year. He wants to discuss where he’s going, what he’s trying to accomplish, and how his investments support those objectives.

At the same time, I’ve met people with a fraction of that wealth who have never written down a financial goal in their lives.

The difference matters.

Goals provide direction. They create accountability. They help you make better decisions because you have a framework for evaluating opportunities and tradeoffs.

A goal could be retiring at age 60. It could be becoming debt-free. It could be building a million-dollar portfolio. It could be saving for a child’s education or preparing to sell a business.

The specific goal doesn’t matter nearly as much as having one.

Alongside goal setting, I encourage people to make credit management part of their annual routine. Every year, pull your credit report and review it carefully.

You may discover inaccuracies. You may find fraudulent activity. You may identify issues that are unnecessarily lowering your score.

I personally discovered fraudulent activity through an annual review. Someone had somehow gained access to a store financing account tied to my credit. Because I caught it early, I was able to resolve the issue and improve my credit score.

Financial success isn’t just about growing assets. It’s also about protecting what you’ve built.

Weeks 10 and 11: Tracking and Reviewing

Once you’ve established goals, you need a way to measure progress.

This is where many people fall short. They create goals in January and forget about them by March. Then they wonder why nothing changed.

Tracking creates awareness. Reviewing creates accountability.

The good news is that technology has made this easier than ever before. Today, artificial intelligence can help you track progress without requiring complicated spreadsheets or hours of manual calculations.

You can provide AI with your net worth, savings targets, debt payoff goals, and investment objectives. It can help monitor progress, identify trends, and keep you focused on what matters.

I’m currently using AI to help track my health goals. Every day I log my workouts, walking mileage, and biking mileage. It helps me understand whether I’m ahead of schedule, on track, or falling behind.

The same concept can work for your finances.

The objective isn’t to create more work. The objective is to create visibility. When you can clearly see progress, you’re more likely to stay motivated and continue moving forward.

What gets measured often gets improved.

Week 12: Create a Stretch Goal

By week 12, you’ve built a foundation. You’ve audited your finances, automated key processes, addressed debt concerns, started investing, established goals, and created a tracking system.

Now it’s time to think bigger.

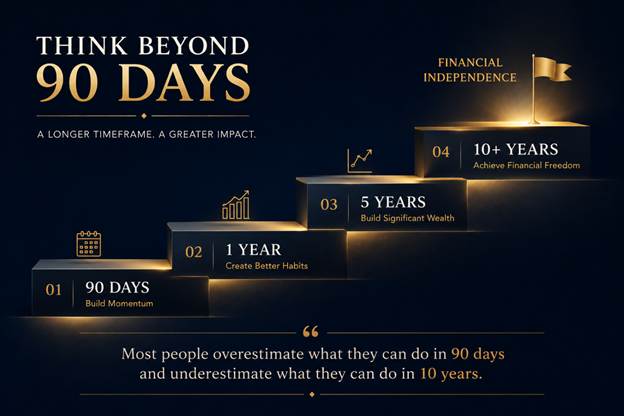

One of the most common mistakes people make is focusing exclusively on short-term goals. They become so focused on the next 90 days that they never define what they’re ultimately working toward.

Research consistently shows that people tend to overestimate what they can accomplish in the short term and underestimate what they can accomplish over longer periods of time.

That’s why I encourage creating a stretch goal.

Where do you want to be in one year? Five years? Ten years?

What would financial success actually look like for you?

Maybe it’s reaching financial independence. Maybe it’s retiring early. Maybe it’s selling a business and creating generational wealth for your family. Maybe it’s having enough flexibility to spend more time doing the things that matter most.

Whatever that vision is, define it clearly.

Your stretch goal becomes the reason you continue after the first 90 days are complete. It becomes the motivation that carries you through setbacks and keeps you moving forward when progress feels slow.

Without a bigger vision, it’s easy to lose momentum. With one, the first 90 days become the beginning of something much larger.

My Final Thoughts

Most people don’t need a more complicated financial plan. They don’t need another budgeting app, another social media money guru, or another hot investment tip. What they need is a system that helps them make consistently good decisions over time.

That’s what this 90-day framework is designed to provide. It starts with understanding where you are today. It moves into creating automation, addressing debt, investing consistently, setting meaningful goals, tracking progress, and building a long-term vision for the future.

Will this solve every financial challenge in your life over the next three months? Of course not. Real financial success is built over years, not weeks. But what this process can do is create momentum, and momentum is often the hardest part.

Once you start making progress, good financial decisions become easier. Saving becomes a habit. Investing becomes routine. Goal setting becomes normal. Over time, those small actions compound into meaningful results.

The people who achieve financial success aren’t necessarily smarter than everyone else. They simply have a process they follow consistently. If you can commit to this 90-day plan and continue building on it after the first three months, you’ll put yourself in a position that most people never reach: you’ll have a system that works for you instead of constantly working against you.

If you’d like help building a financial system that fits your specific goals, reach out to schedule a conversation.