Many people delay investing because they want to find the perfect moment. They watch the headlines, wait for a dip, and hope to buy at the bottom. The trouble is that the perfect moment rarely arrives, and every year spent on the sidelines carries a real and measurable cost. The math consistently rewards those who start early and stay invested over those who try to outguess the market.

This article shows why time in the market matters far more than timing the market, and what waiting actually costs you.

Time Does the Heavy Lifting

Compound growth rewards patience. When your returns start generating returns of their own, your portfolio grows faster each year. The earlier you begin, the longer that snowball rolls, and the larger it becomes. A modest monthly contribution started in your twenties can outgrow a much larger effort started in your forties.

Consider an investor who sets aside $500 each month and earns a 7 percent average annual return. The starting age changes everything.

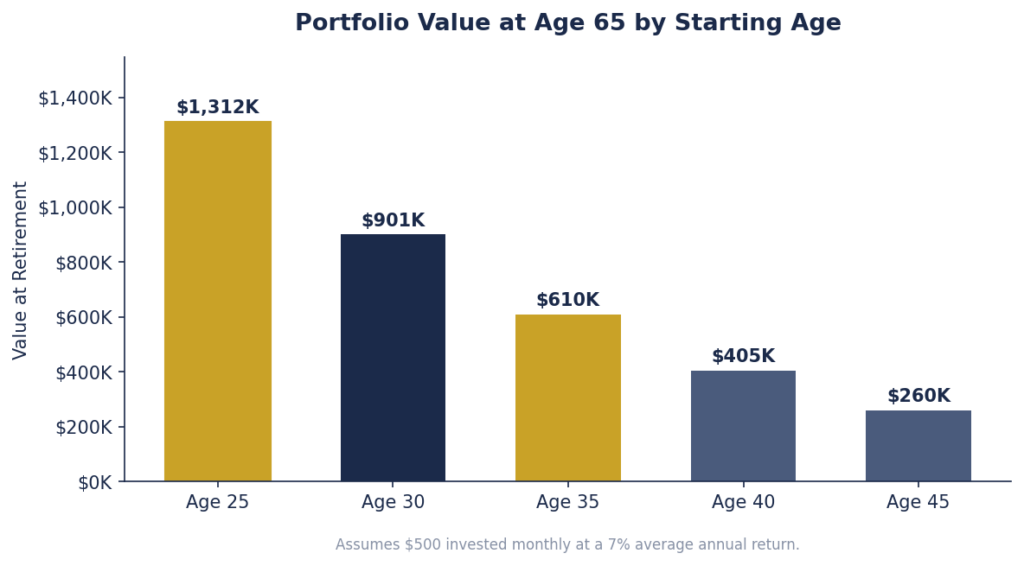

Figure 1. The same monthly contribution produces dramatically different outcomes based on when you begin.

Portfolio Value at Age 65 by Starting Age

| Starting Age | Years Invested | Value at Age 65 |

|---|---|---|

| 25 | 40 | $1,312,000 |

| 30 | 35 | $901,000 |

| 35 | 30 | $610,000 |

| 40 | 25 | $405,000 |

| 45 | 20 | $260,000 |

Assumes $500 invested monthly at a 7% average annual return.

An investor who starts at 25 reaches more than $1.3 million by age 65. Waiting just ten years, until age 35, cuts that result roughly in half. The lost decade is not simply ten years of contributions. It is ten years of compounding that you can never recover.

The Cost of Waiting Adds Up Fast

The gap between an early starter and a late starter widens with every passing year. Early on, the two paths look similar. Over time, the compounding advantage separates them by hundreds of thousands of dollars.

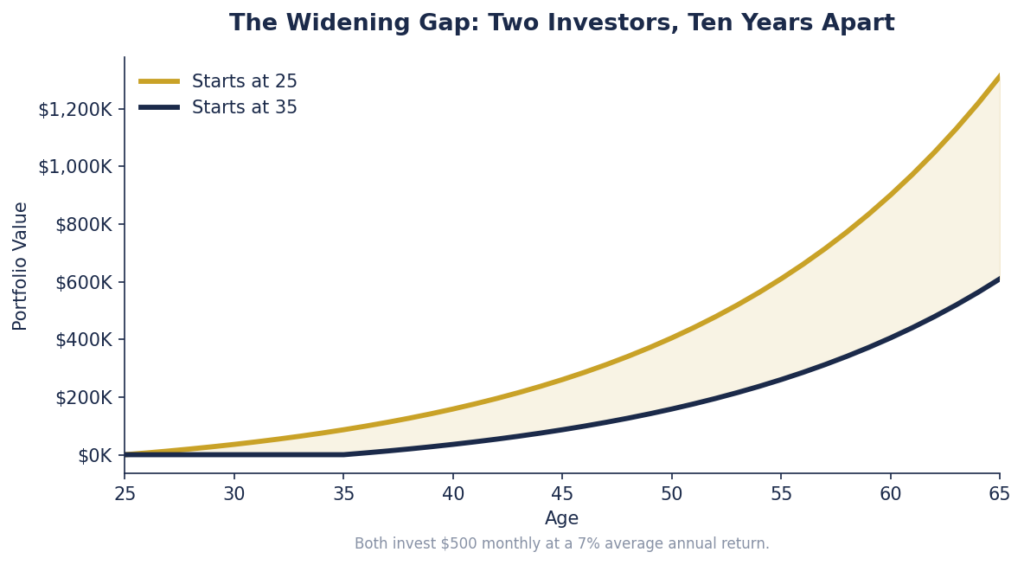

Figure 2. Two investors contribute the same amount each month, but one begins ten years earlier.

Notice how the shaded area grows. That space represents the cost of waiting, and it expands the longer you delay. The investor who starts at 25 does not just finish ahead. That investor pulls further ahead every single year, because the earliest dollars have the most time to grow.

Why Timing the Market Fails

If waiting is costly, many people ask whether they can simply time their entry and exit to capture the gains and avoid the losses. In practice, this strategy almost always backfires. The market’s strongest days often arrive with little warning, and they frequently cluster near the worst days. An investor who steps out to avoid a downturn risks missing the sharp rebound that follows.

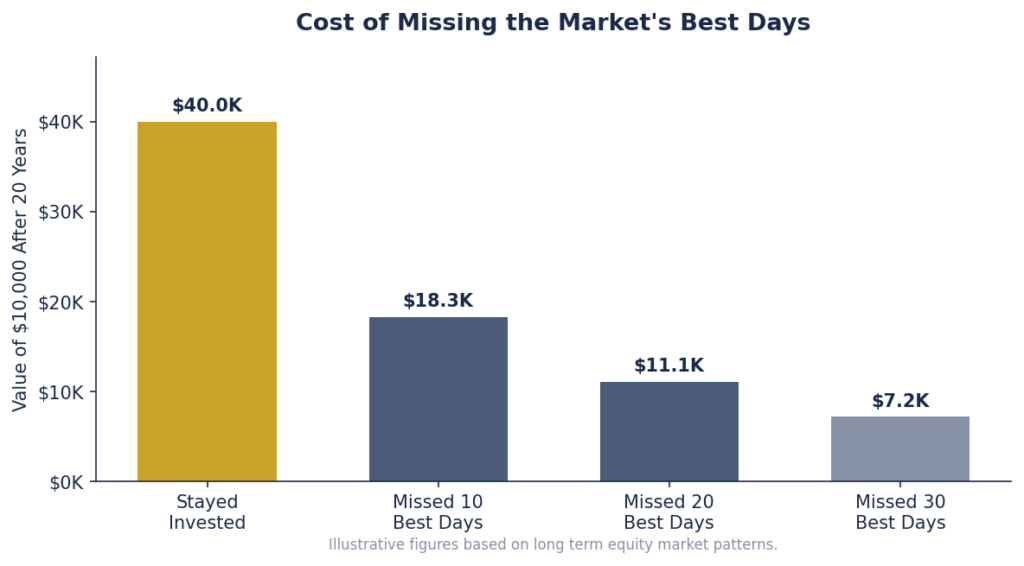

Cost of Missing the Market’s Best Days

| Investment Approach | Value of $10,000 After 20 Years |

|---|---|

| Stayed invested | $40,000 |

| Missed the 10 best days | $18,300 |

| Missed the 20 best days | $11,100 |

| Missed the 30 best days | $7,200 |

Illustrative figures based on long-term equity market patterns.

Missing just the ten best trading days over a twenty-year stretch can cut your final balance by more than half. Miss thirty of the best days and a $10,000 investment ends up at roughly $7,200, less than a fifth of what staying invested would have produced. Since no one can reliably predict which days will drive the biggest gains, staying invested through the ups and downs proves far more effective than jumping in and out.

What This Means for You

The evidence points to a simple and encouraging conclusion. You do not need to be an expert forecaster to build wealth. You need time, consistency, and the discipline to stay the course. A few practical principles follow from the data:

- Start now rather than waiting for the perfect entry point, because time compounds in your favor from the very first dollar.

- Invest consistently through automatic contributions so you keep buying in every kind of market.

- Stay invested during downturns instead of selling, since the best recovery days often follow the worst declines.

- Focus on your long-term plan rather than short term noise, and let compounding do the work.

The Bottom Line

The greatest advantage in investing is not a clever forecast or a perfectly timed trade. It is time. Every year you spend waiting is a year of growth you give away, and no future strategy can fully replace it. The best moment to start was years ago. The next best moment is today.

Ready to put time on your side? The team at Mills Wealth Advisors can help you build a disciplined, personalized plan. Schedule a 15-minute intro call to start the conversation.

Disclosure: This material is for educational purposes only and does not constitute individualized investment advice. The figures shown are hypothetical illustrations based on the stated assumptions and do not represent the performance of any specific investment. All investing involves risk, including the potential loss of principal. Past performance does not guarantee future results.