The second quarter of 2026 looked quite different from the first. After markets struggled in March, stocks bounced back as investors once again focused on artificial intelligence, strong corporate profits and the continued strength of the U.S. economy. Even with the war in Iran, higher oil prices and plenty of uncertainty around the world, markets have remained surprisingly resilient.

That does not mean the risks have disappeared. U.S. stocks, especially many of the large growth companies that have driven returns over the past several years, are now trading at some of the highest valuations we have seen. Markets could certainly continue higher, but the more investors pay today, the harder it becomes to generate the same returns over the next five or ten years.

At the same time, bonds are offering yields we have not seen in years, and areas such as international stocks, real estate and commodities appear much less expensive than the largest U.S. companies. That creates an interesting question for investors: Is now a good time to take a few chips off the table and add a little more defense?

In this quarter’s letter, Mike discusses why it may be time to revisit the amount of risk in your portfolio, where we are finding better long-term opportunities and two new investments we are beginning to add to client accounts.

Please feel free to use the links below to navigate to the different sections of this newsletter.

SECTION I – Quarterly Market Review – Global & U.S. Performance Highlights

SECTION II – Mike’s Commentary, Questions, and Quotes

SECTION III – Tax Corner: Revisit Your Gifting Strategy

SECTION IV – Around The MWA Office

SECTION V – Pictures Worth Looking At

Quarterly Market Review – Global & U.S. Performance Highlights

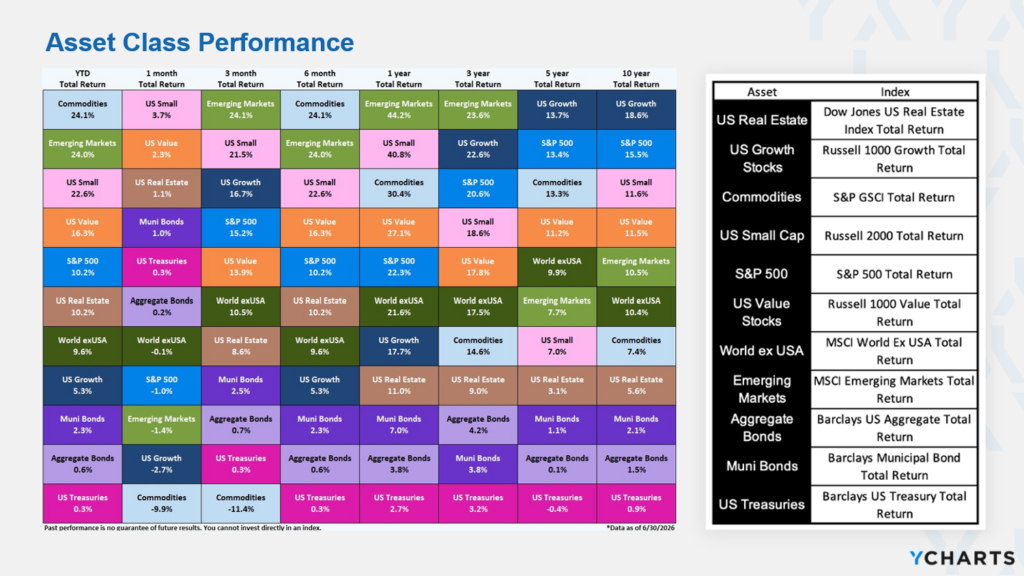

The second quarter of 2026 delivered strong gains across nearly every major market. Emerging markets led the way, surging 24.05%, followed by the U.S. stock market at 15.44% and Global Real Estate at 10.76%. International Developed markets also posted a solid 10.22%. Fixed income markets contributed positive returns as well, with Global Bonds (ex-U.S.) up 1.77% and the U.S. Bond market gaining 0.67%.

Even more encouraging, all of these markets have generated positive returns over the past 1, 5, and 10-year periods, CLICK HERE.

Mike’s Commentary, Questions, and Quotes

Part 1: Client Update

- Part A Valuations: the need to revisit your risk / allocation /time horizon / immunize expenses

- Part B How we are shifting portfolios create exposure to areas that offer good 5-year return set up and characteristics

- Part C Two new investments we are building positions in

Part 2: Client Question

- Should I own Private Equity or Private Credit?

“I think investing is one of the very few fields in life where the harder you try, it’s likely the worse you will do. There’s so much evidence for that, but it’s not like that in almost any other endeavor in life. If you want to be in good physical shape, you got to work hard, you got to sweat, and in investing, there’s just so much evidence that the people who do the best are the ones who just leave it alone.”

–Morgan Housel, author of The Psychology of Money.

(podcast on Motley Fool July 28, 2024.)

I love this quote because it is so true. Ninety-eight percent of the time when accumulating money or investing all you need to do is diversify, keep cost low, and continue to save and winning is almost inevitable. The more risk you assume (if properly diversified) the higher the returns you will experience in the long run. For retirees that are withdrawing money as opposed to saving money the statement above is also true, but the question is, can they wait for the long run to arrive? Large declines in prices are often more painful and potentially much more damaging for retirees (because it can take years or decades for offensive growth assets to grow back after a meaningful decline.)

The math works like this: If you don’t lose much, you don’t have to earn as much back. If you have more defense, you can always shift it to offense if the opportunity set gets big enough. For retirees immunizing expected expenses, matching spending to your investments maturities and balancing the risk of loss with the potential for gain becomes critically important. When large selloffs happen (usually without warning), losses can cause unexpected heartache like the pain of regret, loss of confidence if you are forced to scale back the life you planned on, and loss can affect health and weigh on your important relationships. We think the number one reason clients should create a financial plan is to lay these issues on the table, then create a portfolio strategy that matches future liabilities to the investments inside your portfolio, so that you can unemotionally invest with confidence knowing you have the staying power to ride out the temporary declines that can wear on your soul. Having an advisor that understands your future expenses and cash flow can help you have the confidence to go against the herd at the extremes where markets can overreact and provide opportunity. Investors should expect that they will experience 1-2x large selloffs per decade (the really big ones usually occur every 20-30 years and are really scary and painful).

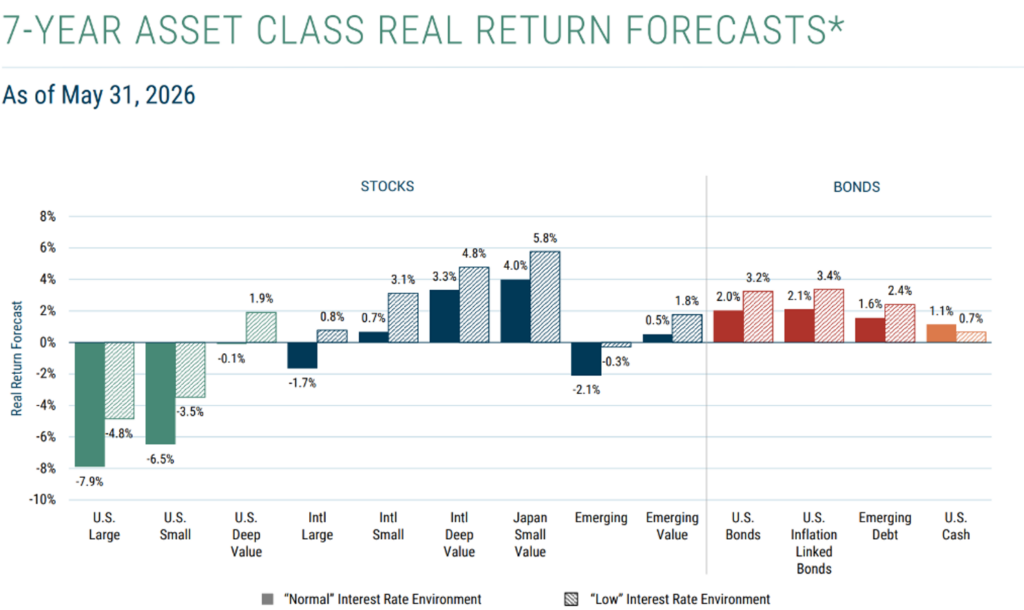

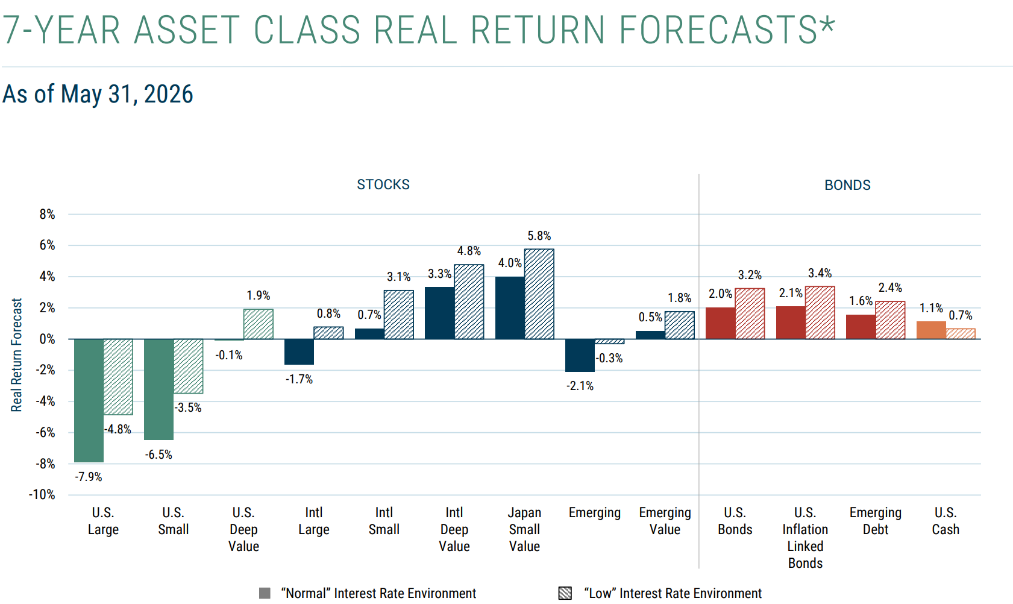

Before I get deeper into why now might be a good time to revisit your plan’s offense and defense, I want to review GMO’s 7-year investment forecast. GMO has been at the forefront of every major market bubble over the last 50 years. Their process for identifying what areas are cheap and which ones are expensive has worked since the 1970s. This is not an exact science, but markets eventually will return to fundamentals. Let’s take a look at what GMO thinks investors can expect. These numbers, even with 2-3% inflation added to them, are depressing.

Figure 1: GMO’s 7-year Real Returns (net of inflation) Return Estimate

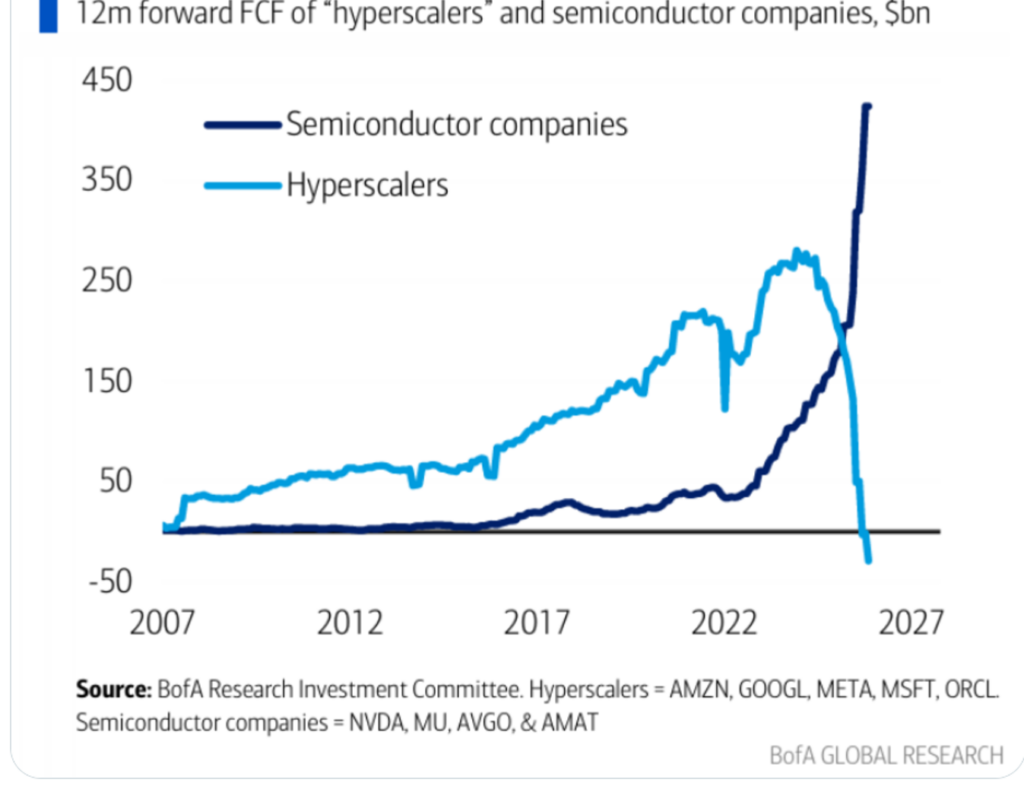

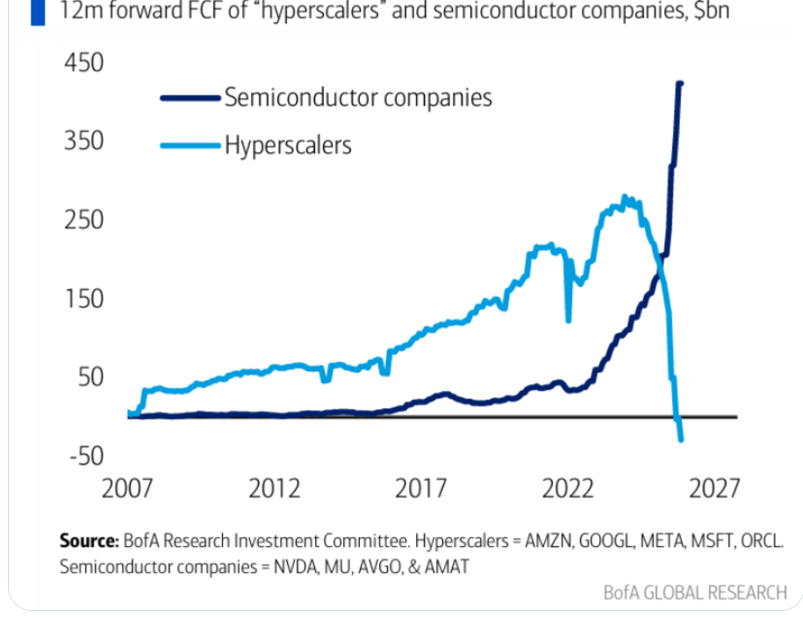

At this point I imagine I sound pretty pessimistic, but I’m actually an optimist. I think AI spending will probably continue to prop up markets into 2027 and hopefully for the foreseeable future. I expect this should continue to fuel US profits, despite higher oil prices and the fighting in Iran. The AI spending boom should benefit global stock markets as many of the commodities, tools, and parts used in this rapid build out will come from countries scattered around the globe. Markets will reward companies that can generate profits and growth. Figure 2 shows how the big hyperscalers are spending money to buy compute. Their spending has ignited the market. How will the market eventually price these businesses as they go from cash flow generators to net borrowers that have less profits to reinvest? How long will the Nvidia chips in the datacenters last? Will these businesses profit even more in the future as these data center investments pay off or will they all compete head-to-head for a winner take all market where only 1-2 win? Will lower profits in 2027 increase their perceived risk or cause their multiples to fall? Because they are such a large weighting in indexes, could a re-rating put pressure on indexes? This is yet another factor I think investors must be aware of as they set their 5-year investment policy.

Figure 2: A Generational Transfer in Free Cash Flows

I personally think the biggest beneficiaries of AI (like most technology revolutions), will be the users of AI. Another positive that I find a little surprising, but it is a bullish sign is how resilient stock markets have been in the face of sticky inflation, war, and US policy changes that could lead to a more volatile geopolitical climate, where might may make right.

The point I have been consistently trying to drive home in my last several updates, to the point that I probably sound like a broken record, is, “Should YOU take any profits?”

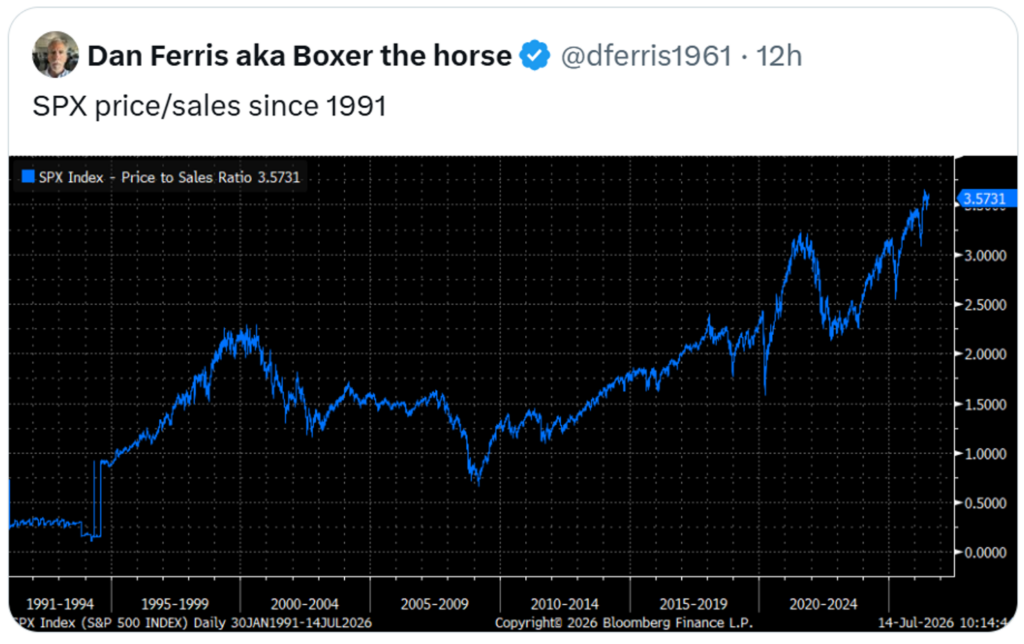

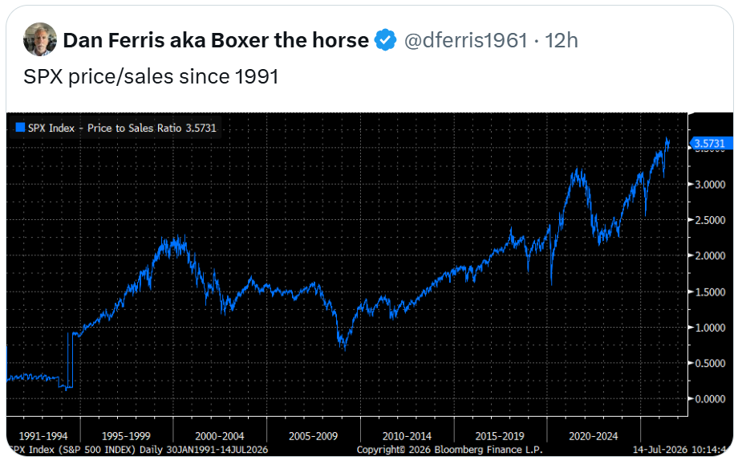

I keep warning of high valuations in US growth stocks that dominate domestic indexes. Most of our clients have some exposure to these widely held, sexy stocks that are now worth more than a trillion dollars. These great businesses are usually found indirectly inside company 401(k) plans, or in trading accounts with large gains, or in parents’ accounts that may be received as a future inheritance. Wherever they are held, the reason I have continued to beat this drum is because I want investors to know that in the past when prices got this high, or indexes got concentrated in a few names, like today, future returns were lousy. Boring and safer investments, like bonds, often provided higher returns over 5-10 years than equities. In the figure below Dan Ferris shows the Price to Sales Ratio over the past 35 years. Price to sales is a good metric because sales are hard to manipulate. It is a pretty simple metric, what price are we paying for today’s company sales. 3.57 is the highest on record, higher than in Dot Com bubble or 2021 peak.

Figure 3: Price to Sales S&P 500, 1991-June 2026

Now I want to switch gears for a moment and talk about defense. Vanguard maintains that “high-quality bonds (both taxable and municipal) offer compelling real returns given higher neutral rates.” (4) Similarly to the early 70s (Nifty 50), or in the late 90s (Internet boom), we never know if the next correction is 1 year away or 5 years away, so I think the only prudent thing to do is to continually revisit your tolerance for risk and capacity to bear losses. Ask yourself what is “safe” to you?

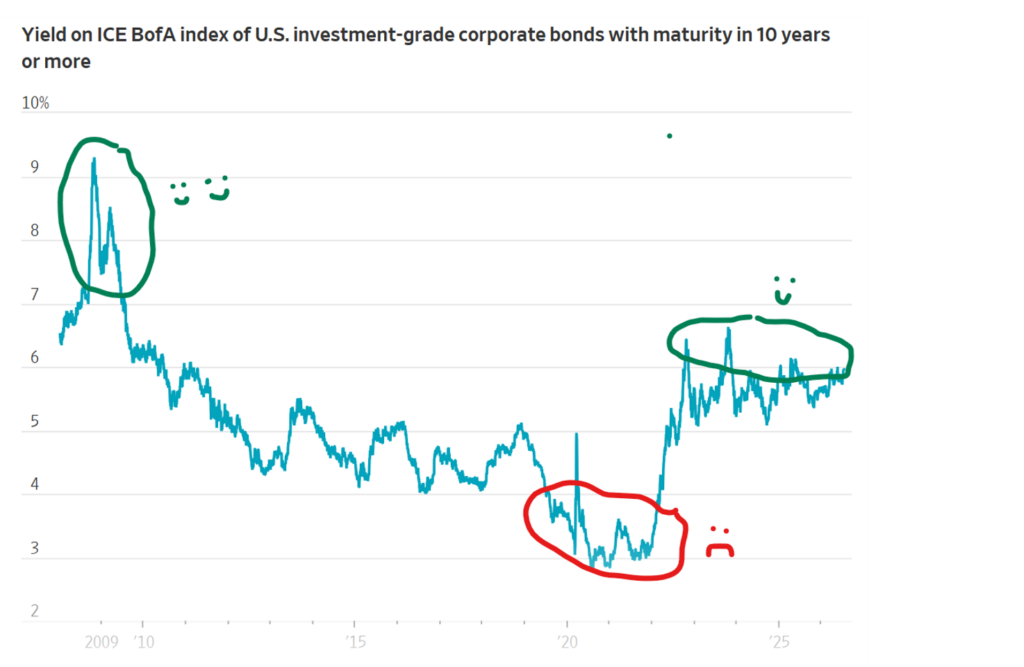

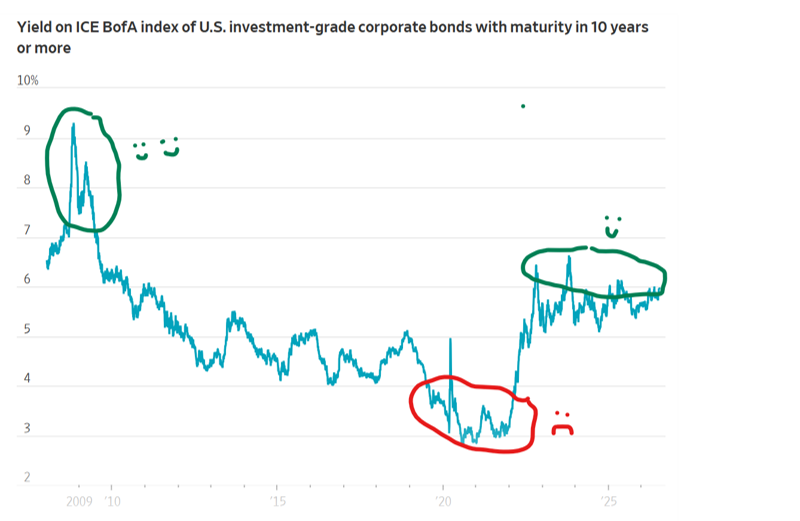

In Figure 4 you can see that Investment grade corporate yields greater than 10 years have risen above 6%, and if interest rates eventually fall, investors would likely get a boost in returns that could make total returns over 5 years approach 8% or so. Our retired clients typically need about 4.5%/year to meet their spending goals, so a 6% current yield is enough to make these bonds well worth owning. As a general rule, we like to increase portfolio durations when we can lock in negatively correlated assets that will often rise when equities fall. “Bonds are back.” Take a look at the green circle on the right in Figure 4. Rates are high enough to extend portfolio duration.

Figure 4: Yields on Investment Grade Debt

Have you asked yourself what is “safe”? I think “safe” is relative because even the most risky investments can be safe at some price or in some combination with other investments, just like the safest businesses (IBM, Kodak, Coke and others in the Nifty 50 in the 1970s) ended up feeling risky as it took nearly two and a half decades to claw back compared to other investments. That’s a long time to wait. I think simply diversifying wider and adding exposure to less expensive areas can offer portfolios much more protection from changes in prices.

I’m going to highlight a few pictures that will show how US growth investors might be like a frog in a slow boiling pot that is continuing to get warmer and warmer as valuations creep higher, moving tomorrow’s returns into our pockets today. We want to make sure investors hang onto some of these gains should markets experience volatility.

Figure 5: A Simple Valuation Framework Warren Buffett Likes

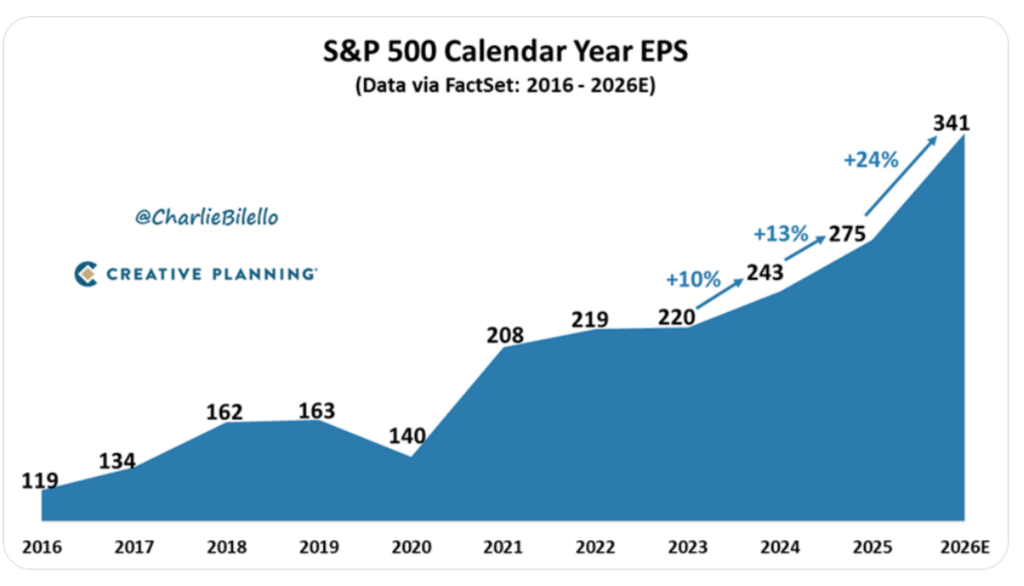

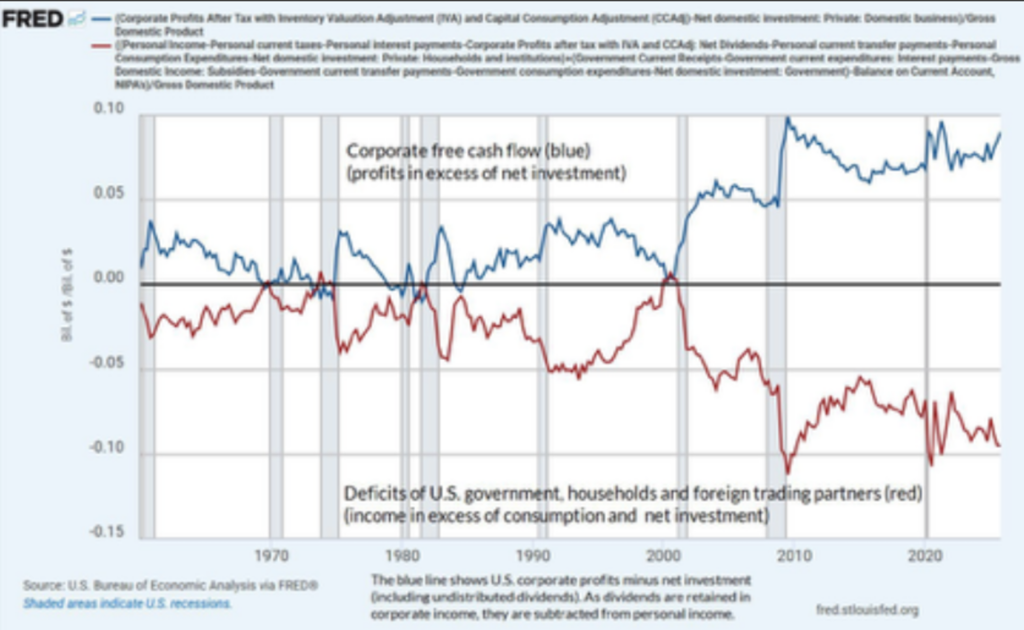

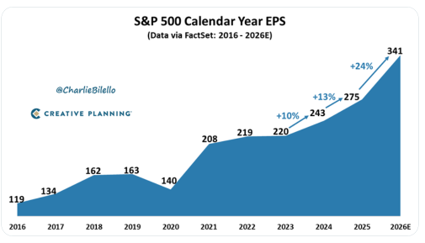

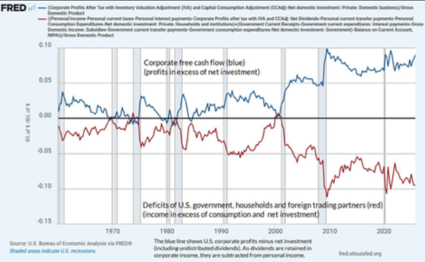

Over the years since the financial crisis US stocks valuations have grown back to some of the highest on record, at the same time profits have continued to grow to the highest profits on record fueled by productivity and deficit spending, buybacks, and shrinking supply of stocks, and as a result of these factors money from around the world has poured into US markets. The US as the reserve currency has a printing press, higher interest rates and therefore we are perceived as the “safest” game around. Remember we created AI and the chip designs that power it. All of these inventions and technology have helped fuel our markets. This increase in profits is easily seen in Figure 6 EPS and Figure 7: Corporate Free Cash Flow relative to Government Spending, and Net Investments.

Figure 6: Earnings Per Share of the S&P 500

Figure 7: Corporate Free Cash Flow from Profits Relative to Deficit Government Spending and Net Investment Into the US.

We have the best technology in the world. AI is going to be a game changer for sure, but is this not why we are trading at record multiples and record valuations? If you think about today’s markets relative to past markets highs…Is there leverage in the system, are individual investors gambling on markets? Are foreigners’ big buyers of our stocks and real estate? I always like to ask myself, “Who is the incremental next buyer?” Is whatever people are excited about “known”? Is “it” priced into markets? Like the quote above basically points out, functioning markets work in the long run. Prices are usually right because all of us are smarter than any one of us. Markets reward bearing risk, but I think the key question investors must ask before and after large gains is, are “you” bearing the right amount of risk? Are “you” willing to wait a decade for prices to go higher?

MIKE’S BIG ASK – Schedule 15-30 minutes to revisit risk in your portfolio.

Is now a good time to pay off some debt? Is it worth paying some tax to sell equities that have had strong gains to buy other investments that are much cheaper (and probably safer in the long run)? Should we change your allocation? Or should we sit tight and let markets do their thing…slowly match higher in the face of uncertainty.

I think investors must understand that AI and the datacenter buildout could cause prices to continue to rise, but what could cause US prices to stop rising (or fall) by negatively affecting valuations?

War – (deficit spending)

Global instability

Weaponizing the Dollar

Reshoring supply (deglobalization)

Higher oil prices

Higher commodity prices

Foreign governments selling some US Treasury’s and buying Gold etc

Lack of labor

Higher interest rates for longer

More Supply of Stock from Stock Issuance (Large IPOs)

And several more that I did not list

If you are ever going to take a few chips off the table, now feels like an ok time to me, even if you are early and markets keep rising. If you do sell some gains, what would you do with it? Should you pay off any debt, or build up a little defense, that could be selectively redeployed if prices were to get cheaper. (If you are not going to lean a little more defensive today, I would encourage you to write down exactly when will you take a few chips off the table, if ever?) The US economy looks strong today, but there are a few cracks that we need to be aware of. As you know, markets can change on a dime, and they often overreact to both the upside and the downside. I’d much rather see clients build up 10% of extra defense today than feel regret if market sentiment changes.

Today the US Treasury 10-year interest rates have risen above normal retiree withdrawal rates, and the equity risk premium is lower than bond yields (another statistic that shows optimism in stock prices). With the war in Iran heating back up, oil prices, which are in everything, may keep inflation higher than normal. Maybe we are in the proverbial “hot pot” and getting some out by leaning a little more conservative is probably warranted (even if you miss out on some future gains with some of your money.) This is not the 1st time optimism has been high because of new technology that could change how business is conducted. Revolutions causing productivity booms are not new. In 1929 the tech boom of the day was RCA (Radio Corporation of America). The excitement caused market prices to run ahead of long-term fundamentals, and investors had to wait so long for earnings to catch up with prices that a generation of investors refused to own equities. Will it be different this time? I hope so. Are we in the 5th inning or the 8th? I’m not smart enough to try and answer that question, but I’m sure we have experienced nice gains. In the bible I believe it said something about stocking up when you are experiencing the “7 plentiful years”, in order to prepare for the “7 lean years.” I still believe diversification is the key to winning and safety

comes from owning productive assets at lower valuations relative to what they are likely to produce in the future. If you look at GMO’s 7-year forecast above you can see that they are not predicting 8%/year returns for most assets. US markets have now had 15 years of growth well above most decades, so don’t get too greedy.

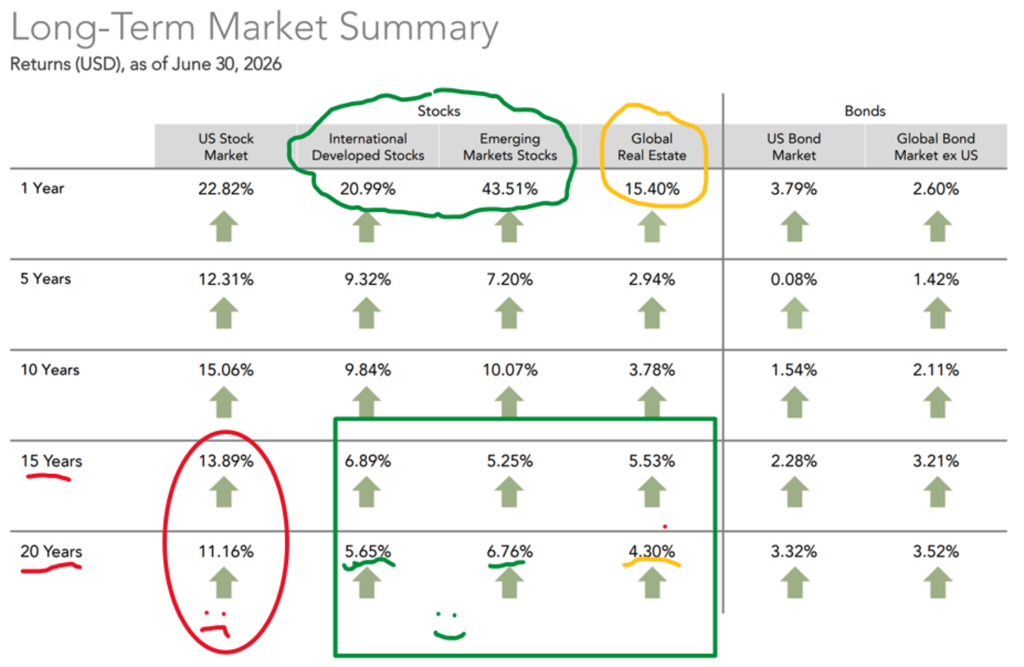

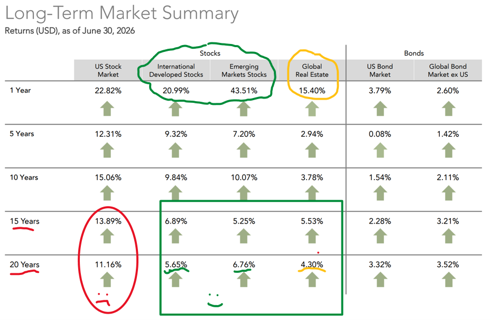

| Over the longer-term most broad markets will earn around 10%, I think this slide helps illustrate how much cheaper international markets are relative to the US Markets, despite the strong returns last year. In order to get the 20-year average ROR up 5.65% to just 10% International Markets need to rise much more than they have recently risen because many of their businesses are still much cheaper relative to their earnings. |

Figure 8: Reversion to the mean – strongest force in finance

Voltaire said, “history never repeats itself, but man always does.”

In Figure 8, I wanted to use 20-year returns compared to current returns to show how much more returns will likely be realized in the broad market areas. US stocks have returned about 11.6%/year for 20 years when 10% is closer to normal, meanwhile look at the 20 year returns of international stocks, emerging markets and real estate to get to 10% it is going to take much more gains than 50%. At some point investors will experience a bear market and while we hope it is not today, we know they are often hard to spot coming, so preparing in advance is prudent.

In Vanguard’s report on AI they said “…let us be clear: Risks are growing amid this exuberance, even if it appears “rational” by some metrics. More compelling investment opportunities are emerging elsewhere even for those investors most bullish on AI’s prospects.” (4)

The investment landscape may have changed, but our discipline hasn’t. Even though AI is the talk of the town, we are always trying to look 5 years down the road to best position you and your funds to generate the highest safest returns to make your plan succeed, so we can help you educate kids, travel, and live the life you have imagined.

Here are a few details on 2 new additions to portfolios that we are funding from gains from US Stocks mostly in tax deferred accounts or with new money when it’s added to accounts.

Real Estate (Public Real Estate Investment Trust)

Cohen & Steers believes listed real estate offers much more attractive relative valuations than broad global equities today and expects market leadership to broaden beyond the narrow group of mega-cap winners that have led over the last decade. They also see long-term demand drivers in data centers, towers, senior housing, and logistics properties. This aligns with both GMO 7-year forecast and reversion to the mean data as well.

After the financial crisis long-term US interest rates fell below 3% which pushed commercial real estate prices up to levels that we felt were not worth owning it. After lousy performance for nearly a decade, we feel that real estate once again deserves a place in diversified portfolios both as a way to reduce risk, but also to potentially add to returns. Today, many public REITs trade at approximately 90% of the underlying net asset values of their properties. Historically this has been a great time to add real estate to portfolios. We expect to own about 50-60% in passive format using Dimensional’s global REIT and about 40%-50% in an actively managed investment by Cohen & Steers. We think forward returns could be between 7-10%/year.

Commodities

Another new small sliver you may notice in portfolios is a dedicated commodities fund. While this will be a small position, commodities have been under-invested in for over a decade. Because adding new supply to natural resources like mines can take 5-10 years to bring on meaningful new supply. The AI infrastructure buildout discussed above will continue to create demand for rare earth minerals and other natural resources. We think strategically adding exposure, especially on weakness can help protect the fixed income in portfolios from inflation, as well as give our equities more protection from reduced profits if input costs rise (like from an extended War in Iran.) Commodities can be hard to own short-term, but over a full investment cycle they can make portfolios more resilient.

Part 2: Client Question:

Should we add Private Equity or Private Credit to portfolios?

That ship has probably sailed. When politicians who are active in private equity start changing rules to allow it to be owned in retirement plans, it is probably safe to assume that there isn’t anyone left to buy and that is an asset that should most likely be avoided. GMO wrote an interesting article on why today’s private equity funds probably won’t produce the kinds of returns like the ones we bought in 2007-2009 when we were buying businesses at 4-6x EBITDA. Today vast sums of money have been raised to invest in private markets and competition is extreme, and costs to invest are very high. This set up rarely produces great long-term outcomes. Mike’s recommendation = AVOID

Bibliography

- GMO 7 year asset forecast gmo.com

- Exhibit 6 – X hyperscalers cash flow

- Price to Sales – X Tobias Carisle https://x.com/Greenbackd/status/2077180355837321373

- Vanguard AI exuberance: Economic upside, stock market downside https://investor.vanguard.com/investor-resources-education/article/ai-exuberance-economic-upside-stock-market-downside

- WSJ Corporate Bonds Have the Best Yields in Years. They Still Aren’t Enough.

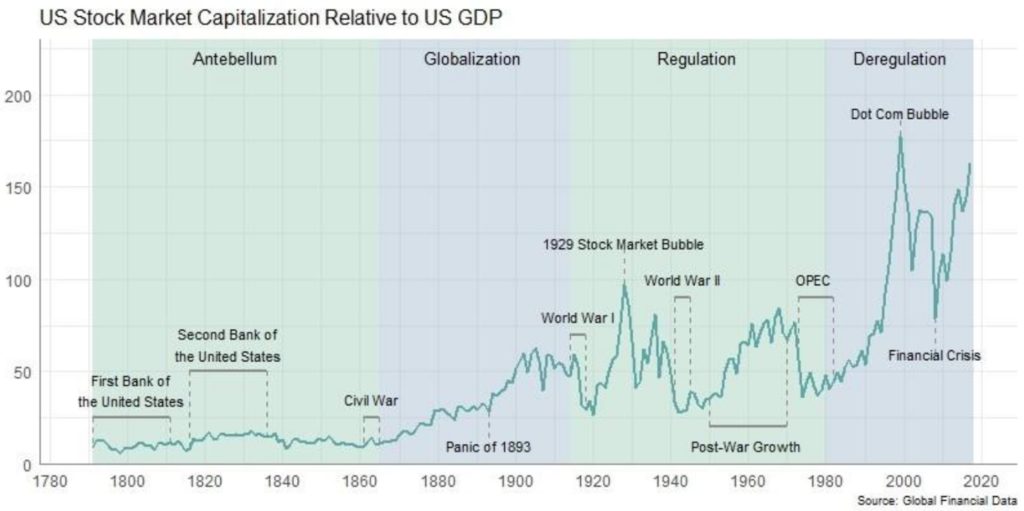

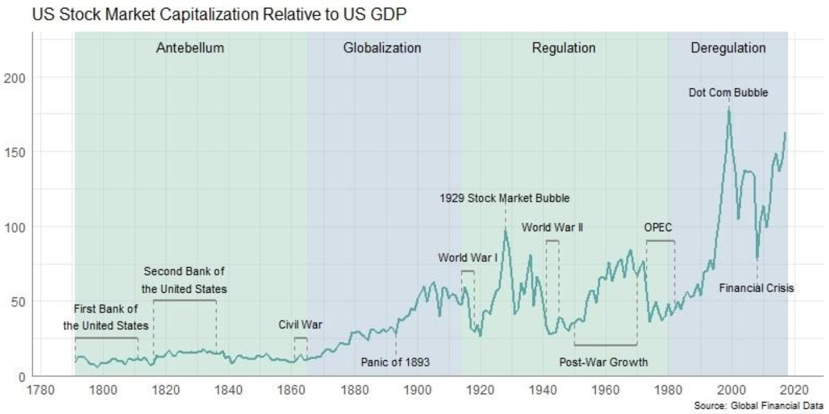

- Global Financial Data: US Stock Capitalization Relative to US GDP

- Higher long-term yields might not compensate for the higher risks By Telis Demos July 14, 2026 5:30 am ET https://www.wsj.com/finance/investing/corporate-bonds-have-the-best-yields-in-years-they-still-arent-enough-aa391e8b?mod=WTRN_pos2

Tax Corner: Let’s Revisit Your Giving Strategy

Last year, we highlighted several changes to the charitable deduction rules that would take effect in 2026. At the time, the focus was on understanding what was coming. Now that those rules are in effect, it is time to determine whether they should change how you approach charitable giving before year-end.

Beginning in 2026, taxpayers who itemize can deduct only the portion of their charitable contributions that exceeds 0.5% of adjusted gross income. For example, a taxpayer with $500,000 of adjusted gross income would not receive a deduction for the first $2,500 of charitable contributions.

The standard deduction also remains an important factor. Even when a charitable gift qualifies, it may not produce an additional federal tax benefit unless your total itemized deductions exceed the standard deduction. As a result, making the same contribution every year may not always provide the most efficient tax outcome.

One strategy to consider is combining, or bunching, several years of charitable gifts into a single tax year. A donor-advised fund can help accomplish this by allowing you to make a larger deductible contribution now and recommend grants to charities over time.

You may also consider donating appreciated investments instead of cash. This approach may allow you to receive a charitable deduction while avoiding the capital gains tax that could result from selling the investment yourself.

For IRA owners who meet the eligibility requirements, a qualified charitable distribution may offer another option. A QCD sends money directly from an IRA to a qualifying charity and may satisfy part or all of a required minimum distribution without adding the distributed amount to taxable income.

The best strategy will depend on your projected income, itemized deductions, charitable goals and the assets available to give. Waiting until the final days of December can limit your options, particularly when transferring investments or establishing a donor-advised fund.

Please reach out to us with any questions or to discuss your 2026 charitable giving strategy.

Around the MWA Office

We would like to introduce our 4 new employees (the most we have ever added at once). Tyler Marie, My beautiful and smart middle daughter is a financial planning and economics graduate from Texas A&M. She is going to be stepping into a financial planning analyst role. She will sit for the CFP in November. Griffin, a finance graduate from the University of Louisiana at Lafayette, will also serve as a financial planning analyst. He is initially going to begin on the trading side of the house helping Matt by executing daily trading. Jane will be helping with email, paperwork, metrics, marketing (part of Crystal’s duties) and other back-office tasks as needed. At the front desk, Grace Weber has been temporarily filling in answering phones, paying bills, helping with all of our new HR work, and most importantly keeping me focused. Please help me welcome these talented and smart young professionals to our team.

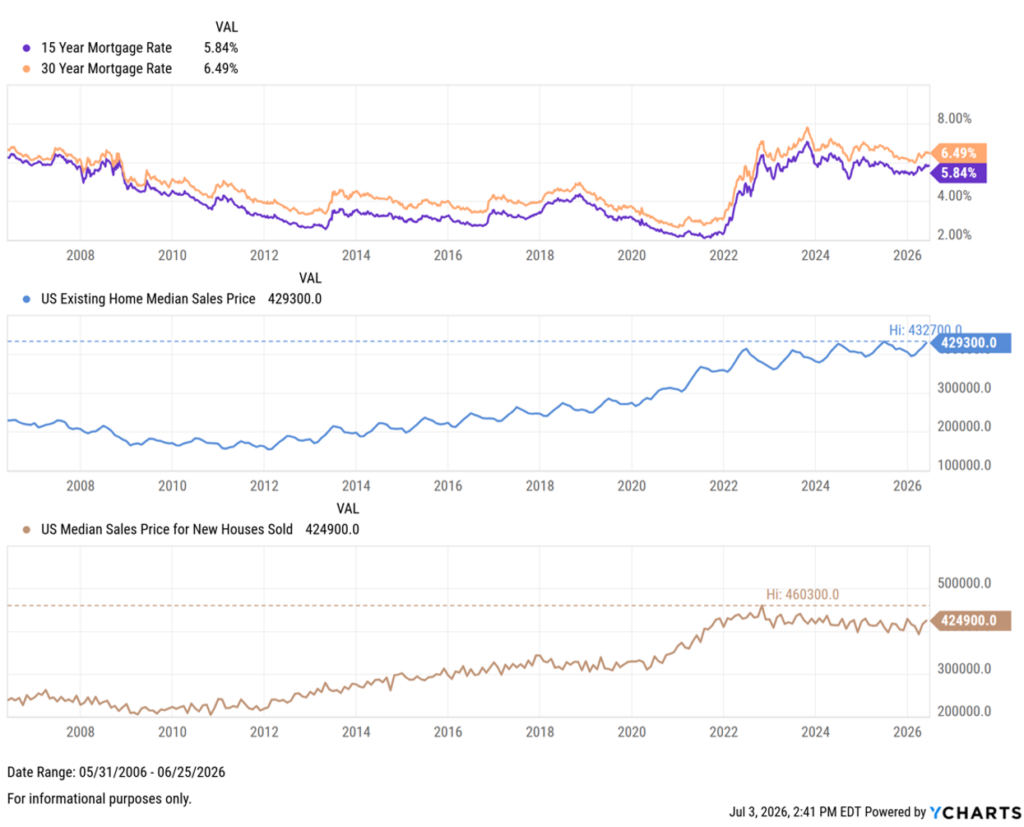

Pictures Worth Looking At