The SECURE 2.0 Act is one of the most significant retirement planning reforms in years. While the legislation was originally signed into law in late 2022, many of its most impactful provisions became effective during 2025 and 2026.

For retirement savers, business owners, and employees participating in workplace retirement plans, these changes create new opportunities to save more, access retirement plans more easily, and potentially improve long-term retirement outcomes.

The challenge is that SECURE 2.0 contains more than 90 separate provisions. Many of them are technical, and most people are unsure which changes actually affect them.

Here are the most important SECURE 2.0 updates that retirement savers should understand in 2025 and 2026.

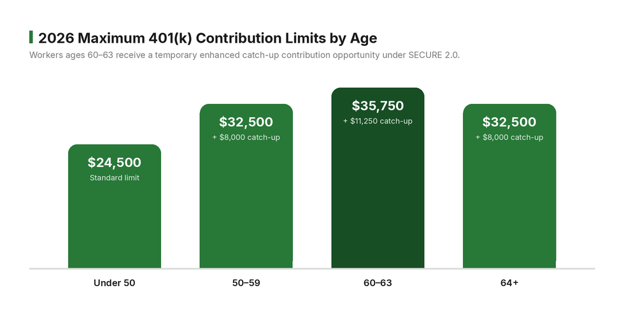

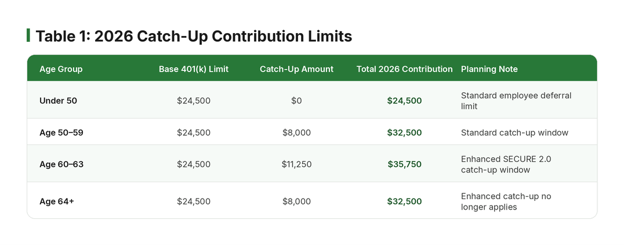

Workers Ages 60–63 Can Save More Than Ever

One of the biggest changes under SECURE 2.0 is the introduction of enhanced catch-up contributions for individuals approaching retirement.

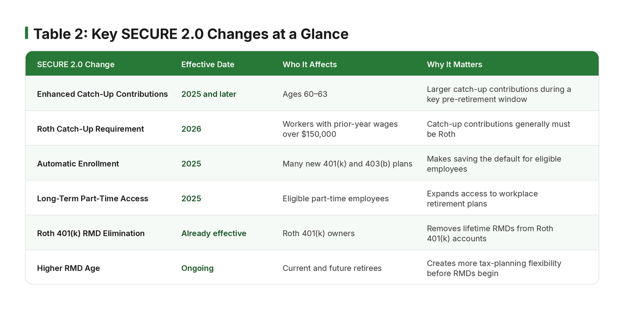

Historically, workers age 50 and older could make catch-up contributions beyond the normal annual 401(k) contribution limit. Beginning in 2025, individuals who turn ages 60, 61, 62, or 63 during the year are eligible for a significantly larger catch-up contribution amount.

For 2025 and 2026, eligible participants can contribute up to:

- The regular 401(k) contribution limit

- Plus a special catch-up contribution of up to $11,250

This enhanced contribution amount is substantially larger than the standard age-50 catch-up contribution.

For someone trying to maximize retirement savings during their highest earning years, this provision creates an opportunity to accelerate savings before retirement. A married couple both between ages 60 and 63 could potentially contribute tens of thousands of additional dollars annually into tax-advantaged retirement accounts.

New Roth Catch-Up Rules Begin in 2026

Another major SECURE 2.0 provision affects higher-income workers who make catch-up contributions.

Beginning in 2026, employees earning more than $150,000 in prior-year FICA wages generally must make their catch-up contributions on a Roth basis rather than a pre-tax basis.

This means:

Before 2026

- Catch-up contributions could generally be made pre-tax

- Contributions reduced taxable income today

Starting in 2026

- Certain higher earners must make catch-up contributions into a Roth account

- Contributions are made with after-tax dollars

- Future qualified withdrawals can be tax-free

For many savers, this will increase current-year tax liability because those contributions will no longer generate an immediate tax deduction.

However, the long-term benefit is that Roth assets can potentially provide tax-free income during retirement, offering greater flexibility when managing future tax brackets.

This change is particularly important for business owners, executives, and highly compensated employees who regularly maximize retirement plan contributions.

Automatic Enrollment Is Becoming the New Standard

One of the primary goals of SECURE 2.0 is increasing retirement plan participation.

Beginning in 2025, many newly established 401(k) and 403(b) plans are required to automatically enroll eligible employees. Participants retain the ability to opt out, but enrollment becomes the default option rather than requiring employees to actively sign up.

Research has consistently shown that automatic enrollment dramatically increases participation rates.

Many employees intend to enroll in retirement plans but delay taking action. By making participation automatic, more workers begin saving earlier and benefit from years of additional compound growth.

For employers, automatic enrollment can help improve employee retirement readiness while also increasing overall plan participation rates.

While some smaller businesses and certain existing plans are exempt, this provision is expected to expand retirement plan participation across the workforce over time.

Long-Term Part-Time Employees Gain Greater Access

Historically, many part-time employees were excluded from workplace retirement plans.

SECURE 2.0 continues efforts to expand retirement plan access by reducing barriers for long-term part-time workers.

Beginning in 2025, more long-term part-time employees become eligible to participate in employer-sponsored retirement plans. This change helps workers who may not meet traditional full-time employment requirements gain access to valuable retirement savings opportunities.

This provision is particularly meaningful for:

- Parents working flexible schedules

- Semi-retired employees

- Seasonal workers

- Employees transitioning between careers

Access to payroll deductions and employer retirement plans can significantly improve long-term retirement outcomes, even for workers with reduced schedules.

Roth Accounts Continue Receiving Better Treatment

SECURE 2.0 further strengthens the attractiveness of Roth retirement accounts.

One of the most notable changes is the elimination of required minimum distributions (RMDs) from Roth 401(k) accounts. Previously, Roth 401(k) participants faced RMD requirements despite the accounts being funded with after-tax dollars.

Today:

- Traditional retirement accounts generally remain subject to RMD rules

- Roth 401(k)s no longer require distributions during the owner’s lifetime

For retirees who do not need immediate income from retirement accounts, this creates additional flexibility and allows assets to continue growing tax-free for longer periods.

It also improves estate planning opportunities because retirees are no longer forced to withdraw funds they may not need.

The Required Minimum Distribution Age Remains Higher

Although the increase occurred earlier, SECURE 2.0 permanently changed the age at which many retirees must begin taking required minimum distributions.

Today, most individuals begin RMDs at age 73. For younger generations, the RMD age will eventually rise to 75.

This seemingly small change can have a meaningful impact.

Delaying RMDs provides:

- Additional years of tax-deferred growth

- More flexibility in retirement income planning

- Greater control over taxable income

- Additional Roth conversion opportunities before mandatory withdrawals begin

For retirees with substantial IRA or 401(k) balances, these extra years can become an important tax-planning window.

Rather than being forced into withdrawals immediately, retirees may have greater ability to strategically manage income and taxes throughout retirement.

SIMPLE IRA Participants Benefit Too

SECURE 2.0 was not solely focused on 401(k) plans.

Individuals participating in SIMPLE IRAs also received enhanced contribution opportunities.

Beginning in 2025, workers ages 60 through 63 can take advantage of larger catch-up contribution limits within eligible SIMPLE plans.

This is particularly important for employees and business owners at smaller companies where SIMPLE IRAs remain a popular retirement plan option.

Historically, SIMPLE plans offered lower contribution limits than many 401(k) plans. The enhanced catch-up provisions help narrow that gap and create additional retirement savings opportunities for older workers.

What Business Owners Should Be Watching

Business owners have several additional considerations under SECURE 2.0.

If your company sponsors a retirement plan, the upcoming Roth catch-up contribution rules deserve particular attention.

Many plan sponsors have spent 2025 preparing systems, payroll processes, and plan documents for the new 2026 Roth catch-up requirements. Employers that wish to continue allowing catch-up contributions for higher-paid employees generally need Roth contribution functionality available within their plans.

Business owners should also review:

- Whether their plan allows Roth contributions

- Employee communication strategies

- Payroll system readiness

- Potential plan amendments

- Opportunities to improve employee participation

The operational side of SECURE 2.0 can be just as important as the planning opportunities it creates.

The Bigger Picture

While many headlines focus on individual provisions, the broader objective of SECURE 2.0 is straightforward:

Help more Americans save more money for retirement.

The legislation seeks to accomplish this through several approaches:

- Expanding access to retirement plans

- Increasing participation through automatic enrollment

- Allowing larger contributions near retirement

- Encouraging Roth savings

- Providing additional flexibility around distributions

- Improving retirement outcomes for part-time workers and small-business employees

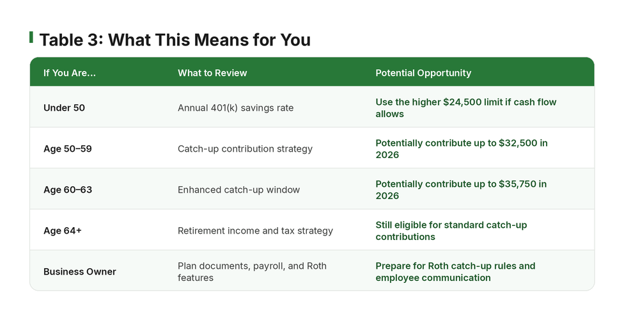

For many households, the biggest opportunities will come from maximizing enhanced catch-up contributions, evaluating Roth strategies, and taking advantage of additional years before required distributions begin.

My Final Thoughts

The SECURE 2.0 Act continues to reshape the retirement planning landscape, and many of the most impactful changes are now taking effect.

While not every provision will affect every retirement saver, several deserve attention, including:

- Enhanced catch-up contributions for ages 60–63

- Roth catch-up requirements for many higher earners beginning in 2026

- Automatic enrollment for many new retirement plans

- Expanded access for long-term part-time employees

- More flexibility surrounding Roth accounts and required minimum distributions

The reality is that retirement planning isn’t just about saving more. It’s about understanding the rules and using them to your advantage.

For some people, SECURE 2.0 creates opportunities to accelerate retirement savings during their highest earning years. For others, it may open the door to Roth strategies, tax planning opportunities, or access to workplace retirement plans that were previously unavailable.

The retirement landscape continues to evolve. The individuals who take the time to understand these changes and adjust their strategy accordingly are often the ones who benefit the most over time.

If you’re unsure how the SECURE 2.0 changes impact your retirement plan, now is a good time to review your strategy and make sure you’re taking advantage of the opportunities available to you.