Retirement is one of life’s most exciting milestones, and honestly, one of the most anxiety-inducing. After decades of saving, the big question shifts from ‘how do I grow my money?’ to ‘how do I make it last?’ That shift can feel quite unsettling, especially when markets are unpredictable and no one knows exactly how long their savings will need to stretch.

The good news is you do not have to figure it out alone, and you do not have to rely on guesswork. A well-constructed retirement income strategy can give you a clear roadmap, one that accounts for your lifestyle, your goals, and the inevitable ups and downs of the market.

In this article, we walk through two of the most popular and effective retirement withdrawal strategies: the Bucket Strategy and the Guardrails Method. Both are proven approaches used by financial planners across the country. Understanding how each one works can help you, alongside your advisor, build a plan that truly fits your life.

Why the 4% Rule is Just a Starting Point

You may have heard of the 4% rule, the idea that you can safely withdraw 4% of your savings each year in retirement without running out of money. It is a helpful benchmark, grounded in real research. But here is the thing: it is a rule of thumb, not a personalized retirement income strategy.

The 4% rule does not account for your specific spending needs, your health, your Social Security timing, whether you carry debt into retirement, or what happens when the market drops 30% in your first year of retirement (a phenomenon known as sequence-of-returns risk). A one-size-fits-all number simply cannot capture the full picture of your financial life.

That is why thoughtful retirees, and their advisors, look beyond the 4% rule to more dynamic, flexible strategies. Two of the most effective strategies are the Bucket Strategy and the Guardrails Method.

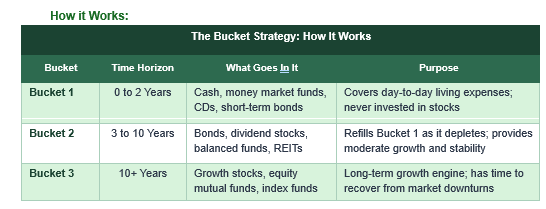

Strategy 1: The Bucket Strategy

What it is:

The Bucket Strategy Retirement approach works exactly the way it sounds: your savings are divided into separate ‘buckets’, each with a different purpose and time horizon. Think of it like organizing your kitchen pantry. You keep everyday staples within easy reach, stock the shelves with items you will need over the next few months, and store bulk goods in the back for the long run.

In retirement, your money works the same way. Each bucket serves a specific role, and together they create a layered system that protects your near-term needs while keeping your long-term savings growing.

When Bucket 1 runs low (usually after one to two years), you refill it from Bucket 2. When Bucket 2 depletes over time, Bucket 3, which has had years to grow, steps in to replenish it. This cycle continues throughout retirement, ensuring your near-term needs are always met regardless of what the stock market is doing on any given day.

Pros:

- Peace of mind: Knowing your next one to two years of expenses are sitting safely in cash means a market drop does not send you into a panic.

- Emotional insulation: You never have to sell stocks at a loss to pay your bills. Bucket 1 handles that.

- Clarity: Many retirees find it easier to visualize and manage their finances when funds are clearly separated.

Cons:

- Requires maintenance: You will need to monitor bucket levels and rebalance periodically, ideally with your advisor’s guidance.

- Cash drag: Keeping too much in Bucket 1, which is low yielding, can limit long-term growth if it is not managed well.

Best For:

The Bucket Strategy is an excellent retirement withdrawal strategy for retirees who prefer a structured, organized approach and who find comfort in knowing exactly where their income is coming from. It works especially well for those who are sensitive to market volatility and want a clear buffer between their daily life and the stock market’s mood swings.

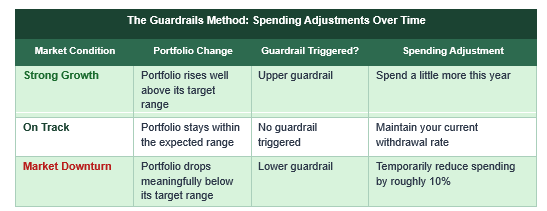

Strategy 2: The Guardrails Method

What it is:

If the Bucket Strategy is about organizing your money into compartments, the Guardrails Method is about staying safely on the road, no matter how winding it gets.

Developed by financial planner Jonathan Guyton, the Guardrails Method is a dynamic retirement withdrawal strategy that sets upper and lower spending limits, like guardrails on a mountain highway. You drive comfortably in the middle, but if you drift too close to either edge, a built-in rule kicks in and guides you back to safety.

How it Works:

You begin retirement with a set withdrawal rate, typically around 5 to 6%, which is slightly higher than the 4% rule allows. From there, your annual withdrawal adjusts based on how your portfolio is performing:

The key insight here is that retirees do not need a perfectly steady income. They need a sustainable one. By agreeing in advance to spend a little more in good years and a little less in lean ones, the Guardrails Method prevents two common mistakes: running out of money too quickly and living too frugally out of unnecessary fear.

Pros:

- Higher starting income: Allows for more spending early in retirement when you are often most active and eager to travel or enjoy new experiences.

- Responsive to reality: Adjusts dynamically to what is happening in your portfolio, changing to accurately depict your current situation, rather than being a static number you set once.

- Protects longevity: Built-in guardrails significantly reduce the risk of outliving your money.

Cons:

- Requires flexibility: You must be willing and able to reduce spending when the lower guardrail is triggered, which can be difficult if your core expenses are fixed.

- More complexity: The math behind guardrail thresholds and implementing them in a way that sustains the duration of retirement works best when set up and monitored with a financial advisor.

Best For:

The Guardrails Method is ideal for retirees who have some flexibility in their lifestyle spending, perhaps discretionary categories like travel, dining, or hobbies that can be scaled up or down without affecting core needs. It rewards those who are willing to let their portfolio performance guide their spending rather than sticking to a rigid, unchanging number.

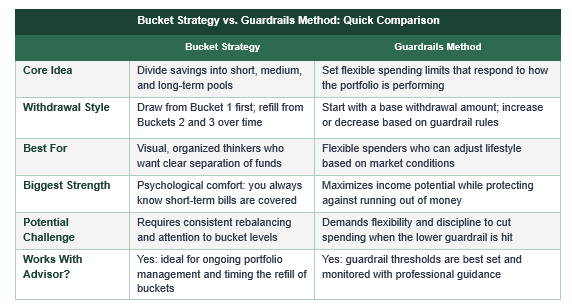

Side-by-Side: Which Strategy Fits You Best

Both the Bucket Strategy and the Guardrails Method are legitimate, research-backed retirement income strategies. They are simply built for different personalities and circumstances. Here is how they compare:

Here is a reassuring truth worth mentioning: these strategies are not mutually exclusive. Many retirees, working with a skilled advisor, use a blend of both. Some clients use a Bucket 1 cash reserve for peace of mind while applying guardrails logic to manage their overall withdrawal rate. The right mix depends entirely on your situation.

The Power of a Personalized Retirement Strategy

Whether you gravitate toward the structured clarity of buckets or the adaptive flexibility of guardrails, what matters most is that your retirement income strategy is personalized, built around your life, your goals, and your comfort level with uncertainty. Market volatility is inevitable. The anxiety that comes with it does not have to be. When you have a well-constructed plan in place, a market correction becomes a moment your strategy already anticipated, not a crisis. That kind of confidence does not come from hoping for the best. It comes from having a plan designed for the full range of possibilities.

At Mills Wealth Advisors, we work alongside you to understand not just your numbers, but your story. When do you want to retire? What does your ideal retirement look like? What would keep you up at night, and what would help you sleep? Those answers shape the strategy we build together.

Ready to Build a Retirement Income Strategy That Works for You?

Whether you are five years from retirement or just getting started, it is never too early to build a thoughtful plan. Our team at Mills Wealth Advisors is here to answer your questions, explain your options, and walk beside you every step of the way. Reach out today to schedule a 15-minute intro call with one of our Wealth Advisors.