Families in Westlake give generously and consistently, supporting their churches, the local schools, youth sports, and the causes that shape the community. Most write checks throughout the year and never think about the tax side of that generosity. That habit feels simple, but it often costs more than it should. With a little planning, the same families can give exactly what they already give and capture meaningful tax savings, simply by changing the timing and the form of each gift.

Why Steady Givers Often Miss the Deduction

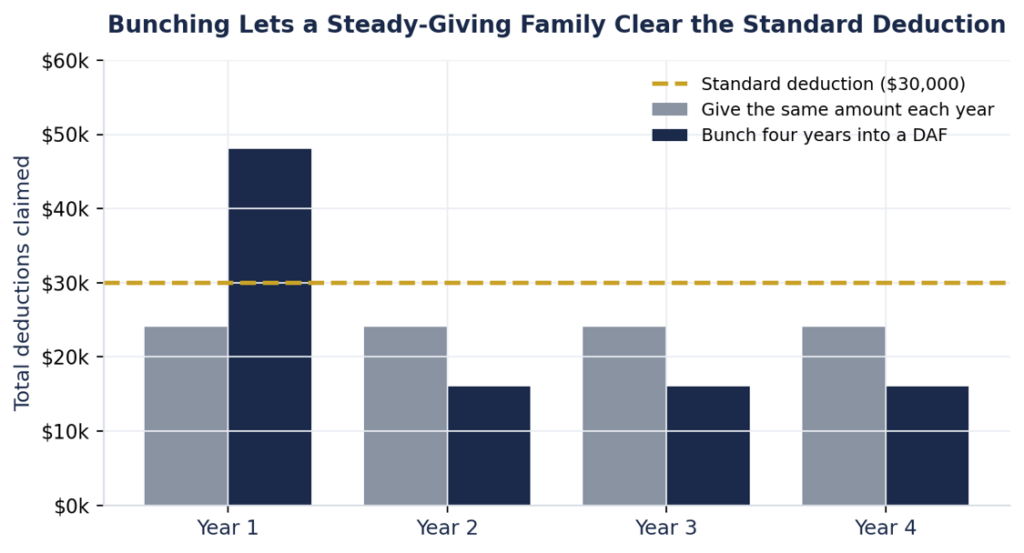

The 2017 tax law raised the standard deduction sharply, and for a married couple it now sits near $32,200. You only benefit from deducting your charitable gifts when your itemized deductions climb above that line. A typical Westlake household with a paid-down mortgage, capped state and local taxes, and $8,000 in annual giving lands below the threshold, so the gifts produce no extra tax savings. You give every year, yet the code rewards you as if you gave nothing. The fix is to concentrate several years of giving into one year so your deductions clear the standard amount, then spread the actual gifts out over time.

Bunch Your Giving and Clear the Threshold

Bunching means combining what you would normally give over several years into one larger contribution. You make that contribution to a donor-advised fund, claim the full deduction in that year, and then recommend grants to your charities on your usual schedule. The community sees no change; your tax return tells a different story.

A family giving $8,000 a year never beats the standard deduction; bunching four years into one DAF clears it with room to spare.

A family that gives $8,000 a year never crosses the $30,000 line on its own. Bundle four years into a $32,000 contribution, and the family sails past the threshold in year one, itemizes, and captures real savings. In the following three years it takes the standard deduction and keeps granting $8,000 to the same organizations from the fund it already filled.

Choose the Right Asset to Give

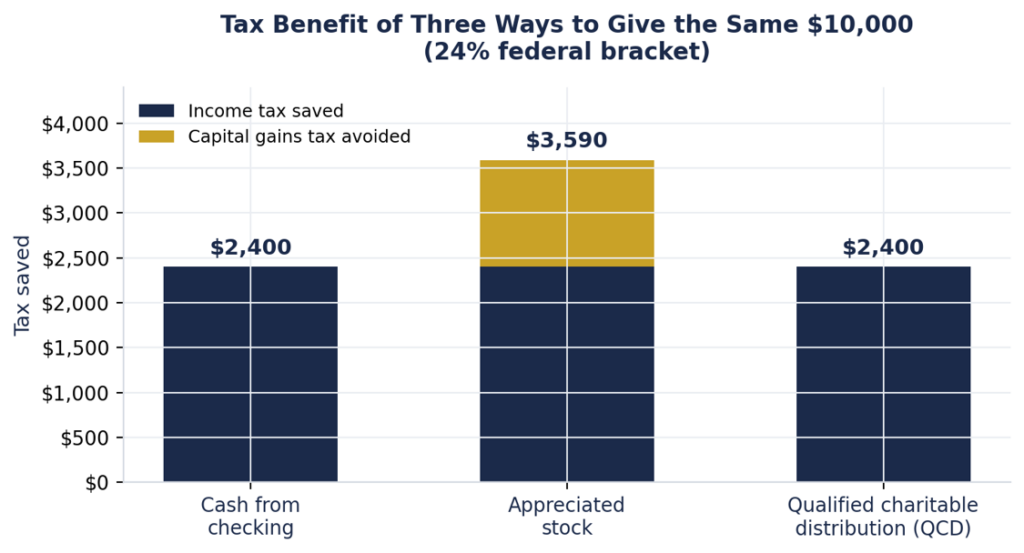

How you fund a gift matters as much as when you give it. Writing a check works, but it is rarely the most efficient route. Two alternatives almost always do better. When you donate appreciated stock you have held more than a year, you avoid the capital gains tax you would owe on a sale and still deduct the full market value, so the charity receives the entire amount. And after age 70 and a half, a qualified charitable distribution sends money straight from your IRA to a charity, satisfies your required minimum distribution, never counts as taxable income, and lowers your adjusted gross income, which can ease taxes on Social Security and trim Medicare premiums.

The same $10,000 gift delivers a bigger benefit when funded with appreciated stock or routed through a QCD.

The chart compares three ways to give the same $10,000 for a household in the 24 percent bracket. Cash and a QCD both save income tax, but the QCD does it while trimming taxable income. Appreciated stock wins outright because it layers capital gains savings on top of the income tax deduction.

Put the Pieces Together Over Time

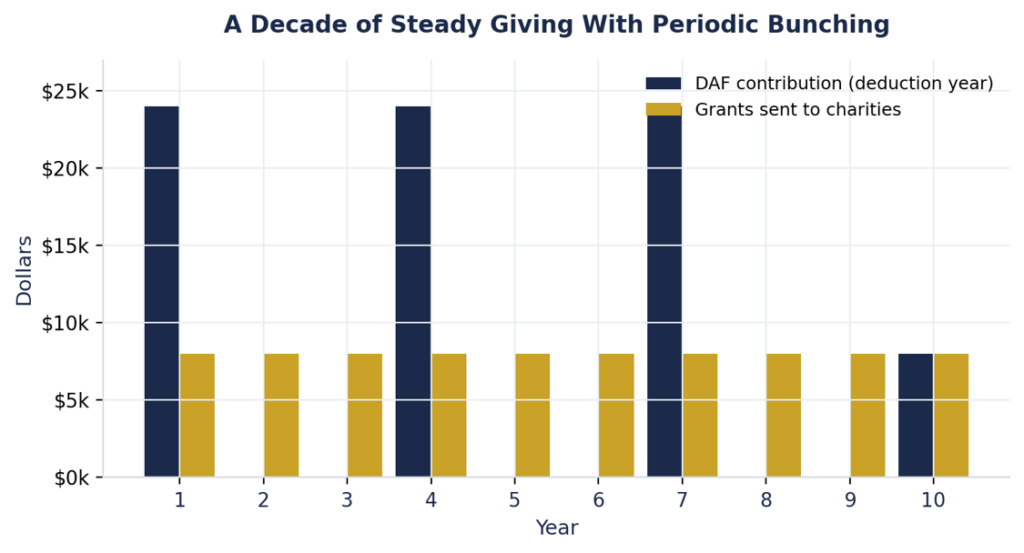

These strategies shine when you treat giving as a long-term plan rather than a year-by-year reflex. Commit to a steady level of support, fund a donor-advised fund every few years to capture the deduction, and grant the same amount to charities each year in between. The chart below shows the rhythm: you contribute in bunched years and grant steadily every year, so the charities feel a constant stream while you claim the deduction when it counts. This approach also simplifies your records, since each contribution generates a single receipt no matter how many charities you eventually support.

A few habits make all of this routine. Review your expected gifts each fall and decide whether a bonus, a property sale, or a strong market year creates the right window to bunch. Lead with appreciated assets before reaching for the checkbook. And coordinate giving with your retirement income and required distributions, where small timing adjustments ripple into real savings. Generosity already defines this community; a modest amount of planning simply lets it stretch further, so the charities win, your family wins, and your giving becomes a deliberate part of your wealth plan rather than an afterthought.