If you are a high-income earner or business owner, there’s a decent chance you’ve looked at your retirement plan and thought:

“Wait… that’s it?”

You max out your 401(k), maybe you do some additional investing in a brokerage account, and then you realize the IRS limits can feel restrictive pretty quickly when your income and savings capacity increase.

That is where the Mega Backdoor Roth strategy starts getting attention.

And despite the complicated name, this is not some secret loophole hiding in the shadows of the tax code. It is a legitimate retirement planning strategy that allows certain individuals to move substantially more money into Roth accounts than most people realize is possible.

The issue is that a lot of people misunderstand how it works.

Some confuse it with a normal Backdoor Roth IRA. Others think only ultra-wealthy people can use it. And many assume their 401(k) already allows it when in reality the plan is not even set up for it.

For the right person though, this strategy can be extremely powerful over time.

Let’s walk through what a Mega Backdoor Roth actually is, how it works, and who should seriously consider using it.

What Is a Mega Backdoor Roth?

A Mega Backdoor Roth is a strategy that allows you to contribute additional after-tax dollars into a 401(k) plan and then convert those dollars into Roth assets.

The key distinction here is that these are not normal Roth 401(k) contributions.

Most people are familiar with these buckets:

- Traditional 401(k) contributions

- Roth 401(k) contributions

- Employer match

- Employer profit-sharing

But some plans also allow:

- After-tax employee contributions

That is the piece that makes the Mega Backdoor Roth possible.

Here’s the basic flow:

- You contribute your normal employee 401(k) deferral

- Your employer contributes any match or profit-sharing

- You then contribute additional after-tax dollars into the plan

- Those after-tax dollars are converted into Roth

Done correctly, this can potentially allow tens of thousands of additional dollars to move into Roth accounts every year.

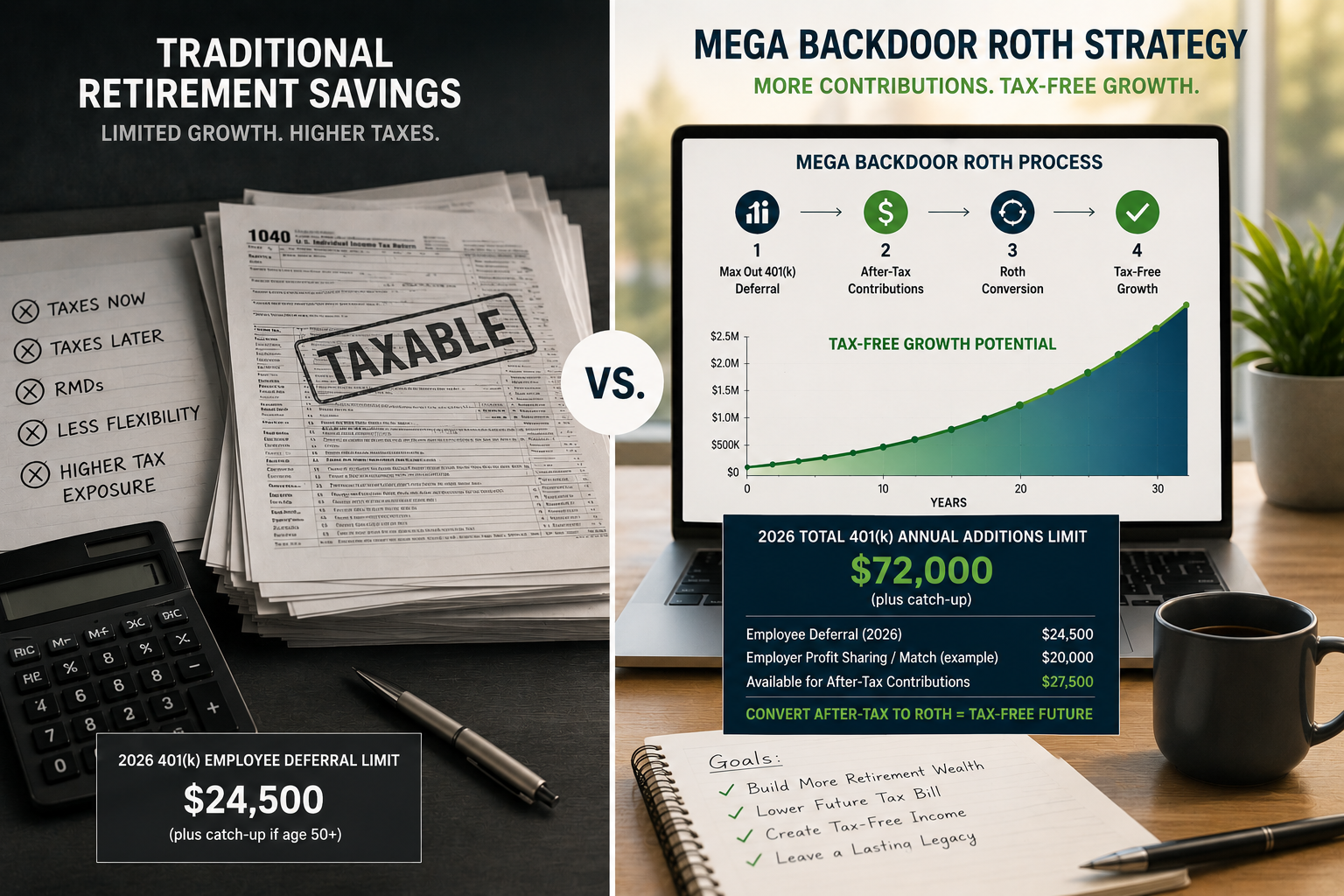

The 2026 Contribution Limits

This is where the math matters.

For 2026, the IRS increased several retirement plan limits.

The employee 401(k) contribution limit is:

- $24,500

If you are age 50 or older, you can also make catch-up contributions.

The standard age 50+ catch-up is:

- $8,000

And under SECURE 2.0, individuals ages 60–63 may qualify for an even larger catch-up contribution:

- $11,250

But the bigger number that matters for Mega Backdoor Roth planning is the total annual additions limit.

For 2026, the total combined 401(k) contribution limit is:

- $72,000

- Or higher with catch-up contributions

That total includes:

- Employee deferrals

- Employer match

- Employer profit-sharing

- After-tax contributions

This is the key.

Most high earners are nowhere near maximizing the full annual additions limit.

A Real Example

Let’s say someone earns $300,000 and their plan allows Mega Backdoor Roth contributions.

In 2026 they contribute:

- $24,500 employee deferral

Their employer contributes:

- $20,000 profit-sharing and match

That means total contributions so far equal:

- $44,500

But the total limit is $72,000.

That leaves:

- $27,500

available for after-tax contributions.

Those after-tax dollars can then potentially be converted into Roth.

That is the strategy.

Over time, this can create a very meaningful amount of tax-free growth potential.

This Is Different Than a Backdoor Roth IRA

People constantly confuse these two strategies.

A normal Backdoor Roth IRA usually involves:

- Making a non-deductible IRA contribution

- Converting that IRA into a Roth IRA

That strategy is commonly used by people who make too much money to contribute directly to a Roth IRA because of income phaseouts.

A Mega Backdoor Roth is completely different mechanically.

It happens inside a 401(k) plan and generally involves much larger contribution amounts.

That is why it is called “Mega.”

Both strategies involve Roth conversions, but that is about where the similarities stop.

Why Roth Assets Matter

A lot of retirement planning conversations focus almost entirely on accumulation.

But eventually retirement planning becomes about taxation and withdrawal strategy.

That is where Roth assets can become incredibly valuable.

Qualified Roth withdrawals can potentially come out tax-free later.

That flexibility matters.

Especially for high earners.

Roth assets may help with:

- Managing retirement tax brackets

- Reducing future required minimum distributions

- Social Security taxation planning

- Medicare IRMAA planning

- Estate planning

- Retirement cash flow flexibility

- Legacy planning for children or heirs

I think one of the biggest mistakes people make is assuming all retirement dollars are equal.

They are not.

The tax treatment of those dollars later matters tremendously.

Someone with:

- Taxable brokerage assets

- Pre-tax retirement assets

- Roth assets

typically has much more planning flexibility than someone who only has pre-tax retirement accounts.

Who Is a Good Fit?

This strategy is not for everyone.

But there are several groups where it often makes a lot of sense.

High-Income Earners Already Maxing Their 401(k)

This is probably the most common fit.

If someone is already contributing the full $24,500 employee limit and still has substantial excess cash flow, the Mega Backdoor Roth may allow them to shelter additional assets from future taxation.

Otherwise, those dollars often end up in taxable brokerage accounts.

And again, there is nothing wrong with brokerage accounts. We use them constantly.

But if someone can move additional long-term assets into Roth buckets, it is often worth evaluating.

Business Owners

Business owners are frequently strong candidates because they may have more flexibility over plan design.

In some situations, we help owners structure retirement plans specifically to allow Mega Backdoor Roth functionality.

This can be especially attractive for:

- Solo 401(k)s

- Owner-only businesses

- Closely held companies

- High-income professional practices

Business owners also often have inconsistent income patterns over time, which makes tax diversification even more valuable.

Aggressive Savers

Some people are simply exceptional savers.

They earn strong incomes, maintain reasonable spending, and consistently have excess cash flow available for investing.

Those are often the people who benefit most from additional Roth capacity.

Especially during peak earning years.

People Concerned About Future Tax Rates

Nobody knows exactly where taxes are headed long term.

But many clients look at:

- Federal debt levels

- Government spending obligations

- Historically low tax brackets

and conclude there is at least a reasonable possibility taxes rise over time.

For those individuals, increasing Roth exposure can feel strategically attractive.

Your Plan Has to Allow It

This is one of the biggest misconceptions I see.

You cannot just decide to do a Mega Backdoor Roth if the plan does not support it.

The 401(k) plan generally needs:

- After-tax contribution provisions

- Roth conversion functionality

- Proper payroll setup

- Administrative support

A surprising number of plans do not allow this.

And honestly, a surprising number of advisors never bring it up even when it may be a good fit.

We regularly see situations where someone theoretically could have been doing this for years, but nobody ever structured the plan correctly.

Administration Matters

This is not a strategy where sloppy execution is acceptable.

The details matter.

You need to properly coordinate:

- Contribution limits

- Payroll coding

- Contribution source tracking

- Roth conversion timing

- Compliance testing

- Plan administration

Especially for businesses with employees, there can be additional complexity involving nondiscrimination testing and plan design.

That is why the TPA and advisor matter.

A good strategy implemented poorly can create operational headaches.

Solo 401(k)s Can Be Extremely Powerful

Solo 401(k)s are often one of the cleanest environments for Mega Backdoor Roth planning.

Why?

Because there are no non-owner employees creating testing complications.

That often gives the owner substantial flexibility.

We regularly see business owners who assume they are already maximizing retirement contributions when in reality they still have significant unused capacity available through after-tax contributions.

For the right business owner, this can become a major long-term wealth accumulation tool.

Timing of the Roth Conversion

Generally speaking, many people prefer converting after-tax contributions relatively quickly.

The reason is simple.

The after-tax contribution itself is not taxable again, but any growth before conversion may become taxable.

By converting sooner, you may reduce taxable earnings accumulating before the Roth conversion occurs.

The exact process depends on the plan setup though.

Common Mistakes

There are several mistakes we commonly see with Mega Backdoor Roth planning.

Assuming the Plan Allows It

Many plans simply do not.

Confusing After-Tax Contributions With Roth Contributions

These are completely different contribution types.

Poor Payroll Coordination

We sometimes see payroll systems incorrectly stopping contributions early or coding sources incorrectly.

Forgetting Overall Financial Planning

Just because someone can contribute aggressively does not automatically mean they should.

We still need to evaluate:

- Liquidity

- Emergency reserves

- Business cash flow

- Debt structure

- Taxable investment accounts

- Upcoming spending needs

Retirement planning should fit inside the broader financial picture.

Is It Better Than a Brokerage Account?

Not necessarily.

This is not an all-or-nothing decision.

Taxable brokerage accounts remain incredibly valuable because they provide flexibility and accessibility before retirement age.

But for someone already building substantial taxable assets, increasing Roth exposure may create meaningful long-term tax advantages.

The right answer depends on:

- Current tax bracket

- Future tax expectations

- Retirement goals

- Estate planning goals

- Time horizon

- Cash flow needs

This is why personalized planning matters.

My Final Thoughts

The Mega Backdoor Roth is one of the most powerful retirement planning opportunities available for high-income earners and business owners, but it is also one of the most misunderstood.

For the right person, it can allow substantial additional dollars to move into Roth accounts every single year beyond the normal contribution limits most people think about.

Over time, that can create enormous tax planning flexibility.

But the strategy only works if the retirement plan is designed correctly and administered properly.

The contribution limits matter. The payroll setup matters. The Roth conversion process matters. And most importantly, the strategy should fit within a broader financial and tax planning framework.

I think this is one of the clearest examples of the difference between simply saving money and proactively designing a long-term financial plan.

A lot of people are contributing to retirement accounts.

Far fewer are strategically thinking through where those dollars should go, how they will eventually be taxed, and what kind of flexibility they want decades down the road.