If you live in Colleyville, I’d imagine you’ve built a strong income or asset base. As a Colleyville financial advisor, I see that from the outside, everything looks like it’s working.

But when I sit down with families in this area, I see the same pattern over and over again. They do not actually have a financial plan. What they have is a collection of accounts, policies, and decisions that were made at different points in time, often without coordination.

That is not a failure. It is normal. Life gets busy, income grows, and things get layered on top of each other. But if your goal is to build meaningful wealth and protect it, you need structure. You need clarity. You need a plan that connects everything.

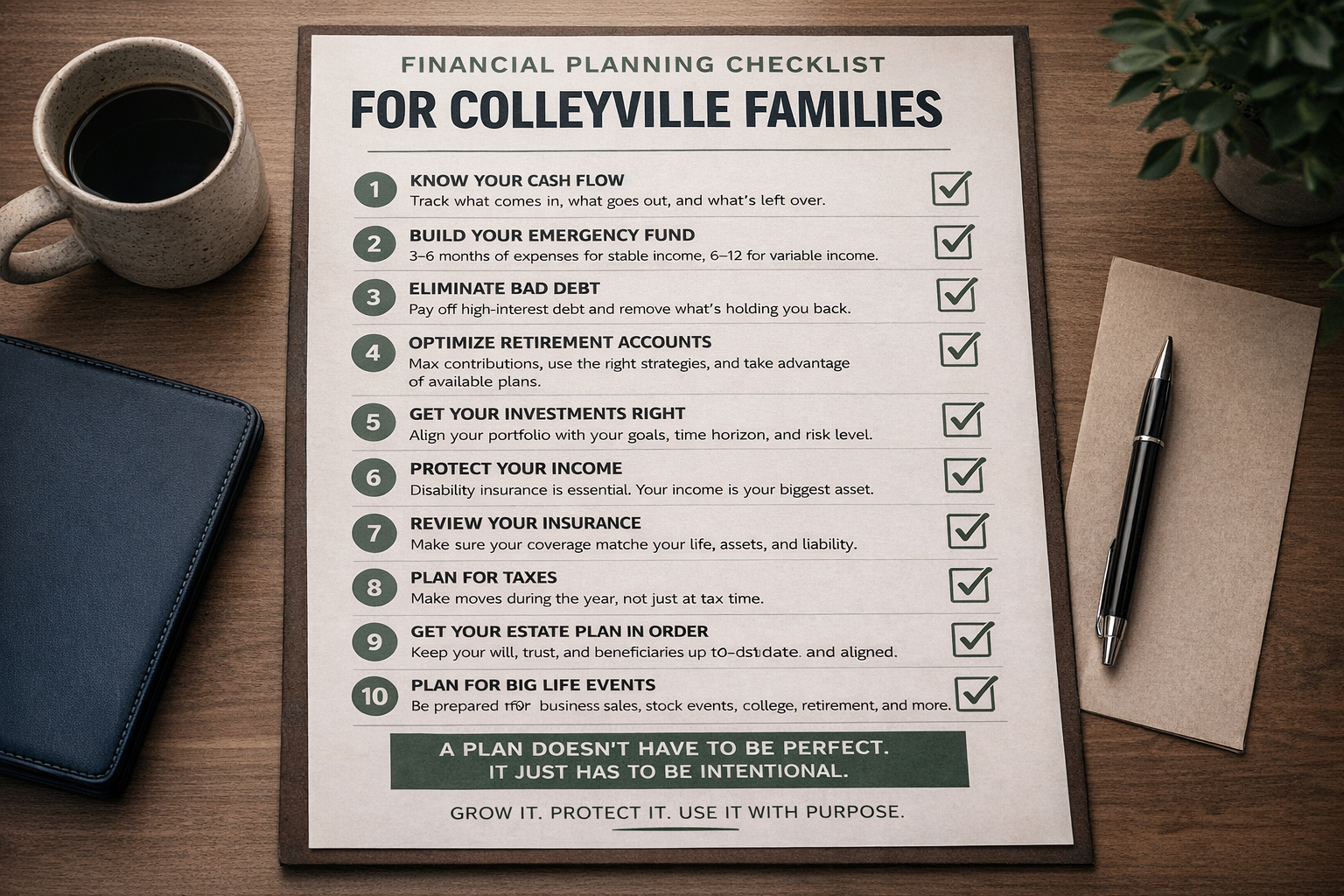

So here is a practical financial planning checklist for Colleyville families. No fluff. Just what actually matters.

12 Steps to Optimize Your Family’s Financial Plan

1. Analyze Your Cash Flow to Build a Wealth Foundation

Most people can tell you what they make. Very few can tell you what they keep. That gap is where problems start.

Wealth is not built on income. It is built on what is left after everything else is spent or used. That means you need to understand your real cash flow, not what you think it is.

Pull actual numbers. Look at the last three to six months. What came in, what went out, and what consistently remained. If you are making $300,000 or $400,000 a year but only saving a small amount, the issue is not income. It is cash flow. Until that is clear, everything else in your plan rests on a weak foundation.

2. Define an Emergency Fund Based on Your Unique Situation

An emergency fund should not be a random number sitting in a savings account. It should reflect your situation.

A dual-income household with stable jobs may need three to six months of expenses. A business owner with variable income should likely be closer to six to twelve months.

This money is not about growth. It is about protection. It exists so that when something unexpected happens, you do not have to make a bad decision under pressure. That purpose needs to be clear.

3. Prioritize Debt Reduction to Protect Your Assets

Not all debt is bad, but a lot of it slows you down. High interest credit cards, personal loans, and expensive car loans quietly erode your ability to build wealth.

What stands out even more is when families with strong incomes and growing net worth still carry consumer debt. At that point, it is no longer a math issue. It is a prioritization issue.

The goal is not to eliminate every type of debt blindly. It is to evaluate whether the debt is helping you move forward or holding you back. If it is not serving a purpose, it needs to be addressed.

4. Optimize Retirement Accounts with Targeted Tax Strategies

This is one of the most misunderstood areas in financial planning. Many people feel confident because they are contributing to a 401(k) and getting a match, but it is a mistake to assume that 401(k) contributions automatically mean tax savings in the long run.

That is participation. It is not optimization.

You need to ask better questions. Are you maxing out your contributions? For 2026, the IRS 401(k) contribution limit has increased to $24,500, with an additional $7,500 catch-up for those 50 and older. Are you using the right mix of pretax and Roth strategies? Determining the right balance in the Roth vs. Traditional 401(k) debate is a key part of true optimization. If you are a business owner, are you using more advanced tools like a solo 401(k) or a cash balance plan.

Most people default into whatever their employer set up. That is not a strategy. It is autopilot. And autopilot rarely produces the best outcome for high income families.

5. Align Your Investment Portfolio with Specific Life Goals

Investment portfolios often look fine on the surface. There are funds, there is diversification, and nothing appears broken. But when you dig deeper, there is often no clear strategy. At Mills Wealth, our investment process is designed to eliminate that guesswork and ensure every dollar has a specific job.

You might see too much cash sitting idle, an overconcentration in one stock, or a mix of investments that were added over time without coordination.

Your portfolio should answer a simple question. What is this money for.

If you cannot clearly define the purpose, then the allocation is based on guesswork. And guesswork tends to work until markets get volatile. That is when the cracks show up.

6. Protect Your Household Income with Disability Insurance

For most families, their ability to earn income is their largest asset. It is the engine that drives everything else.

But it is often underprotected.

Disability insurance is commonly misunderstood or ignored. Many assume their employer coverage is sufficient, but when you look closely, it usually falls short.

This is one of those areas where nothing seems urgent. Until it is. And by the time it becomes urgent, your options are limited. Protecting your income should be a priority early, not something you revisit later.

7. Conduct a Comprehensive Insurance and Liability Review

Insurance is easy to ignore because nothing happens most of the time. That is exactly why it gets overlooked.

As your income grows and your assets increase, your coverage needs to keep up. Many families have policies that were put in place years ago and never revisited.

That creates gaps. Your home may not be insured based on current rebuild costs. Your liability limits may be too low. You may not have an umbrella policy in place. In a litigious environment, a Texas personal umbrella policy provides a critical layer of liability protection above your standard home and auto limits.

I have seen situations where someone was told they did not need additional coverage, only to find out later that they did. These are not theoretical risks. They show up in real life, often when it is least convenient.

8. Implement Forward-Looking Tax Planning (Not Just Filing)

Most families think they are doing tax planning, but in reality, they are doing tax reporting. It is important to realize that your CPA may not be giving you tax advice on how to actually lower your future liability; they are often just recording what already happened.

Tax reporting looks backward. It tells you what happened after the year is already over. That is necessary, but it is not enough.

Tax planning looks forward. It involves making decisions during the year that impact your tax outcome. That could include adjusting income, accelerating deductions, or coordinating investment moves.

If your tax bill surprises you in April, that is a sign that planning did not happen. For higher income families, this is often where the biggest opportunities are missed.

9. Keep Your Estate Plan and Beneficiaries Up to Date

Estate planning is either ignored or outdated for most families. Either there is no plan, or it has not been reviewed in years. To understand the basics of what your documents should cover, the American Bar Association’s guide to wills and estates is an excellent resource for families starting this process.

Having documents in place is only the starting point. Advanced strategies, such as using 529 plans for high-net-worth estate planning, can help you transfer wealth more efficiently while providing for your family’s future. The details matter. Beneficiary designations, account titles, and legal documents all need to align.

I have seen plans that looked solid on paper but failed in execution because the pieces were not connected. That leads to confusion and unintended outcomes.

This is not something you set once and forget. It needs to evolve as your life changes.

10. Plan Ahead for Major Financial Life Transitions

Colleyville families often experience major financial transitions. Whether you are navigating exit planning for a business sale, receiving stock compensation, or approaching retirement, the biggest opportunities for savings exist before the transaction is finalized.

The mistake is waiting until those events are already happening to start planning.

The biggest opportunities exist before the event. For example, if you are planning for education costs, you can research state-specific 529 plan benefits to see how they fit into your overall gifting and tax strategy. That is when you have flexibility. Once things are finalized, many options disappear.

Planning ahead gives you control. Waiting limits it.

11. Coordinate Your Team of Financial Professionals

Most families have multiple professionals involved in their finances. A CPA, a financial advisor, an insurance agent, and an attorney.

The issue is that they often operate independently.

That lack of coordination leads to missed opportunities and conflicting advice. You end up trying to connect everything yourself, which is not realistic.

The best outcomes happen when everyone is aligned. You can learn more about who we are and how we act as the coordinator for your professional team to ensure your plan actually works the way it should. When decisions in one area support what is happening in another. That is when a plan actually works the way it should.

12. Define What Long-Term Financial Success Looks Like for You

This is the step that brings everything together. It is also the one most people skip.

What does success actually look like for you.

When do you want to retire. What kind of lifestyle do you want. What do you want to provide for your family.

Without clear answers, every decision becomes reactive. You are moving forward, but without a defined direction. That makes it difficult to know if you are on track.

How to Get Started with Financial Planning in Colleyville, TX

Most families in Colleyville are doing well. They are earning, saving, and making thoughtful decisions. But doing well is not the same as having a plan.

This checklist is about identifying gaps and bringing structure to your financial life.

The goal is not just to build wealth. It is to grow it, protect it, and use it with intention over time.

That does not happen by accident. It happens when the pieces are connected.

My Final Thought

You do not need to fix everything at once.

Start with one area. Get clarity. Then move to the next.

That is how real financial plans are built. Step by step, with intention.

And if things start to feel more complicated than they should, that is usually a sign that coordination is missing. That is where having the right structure and guidance can make a meaningful difference. If you are ready to stop being reactive and start creating a plan, please contact us today to schedule a conversation.