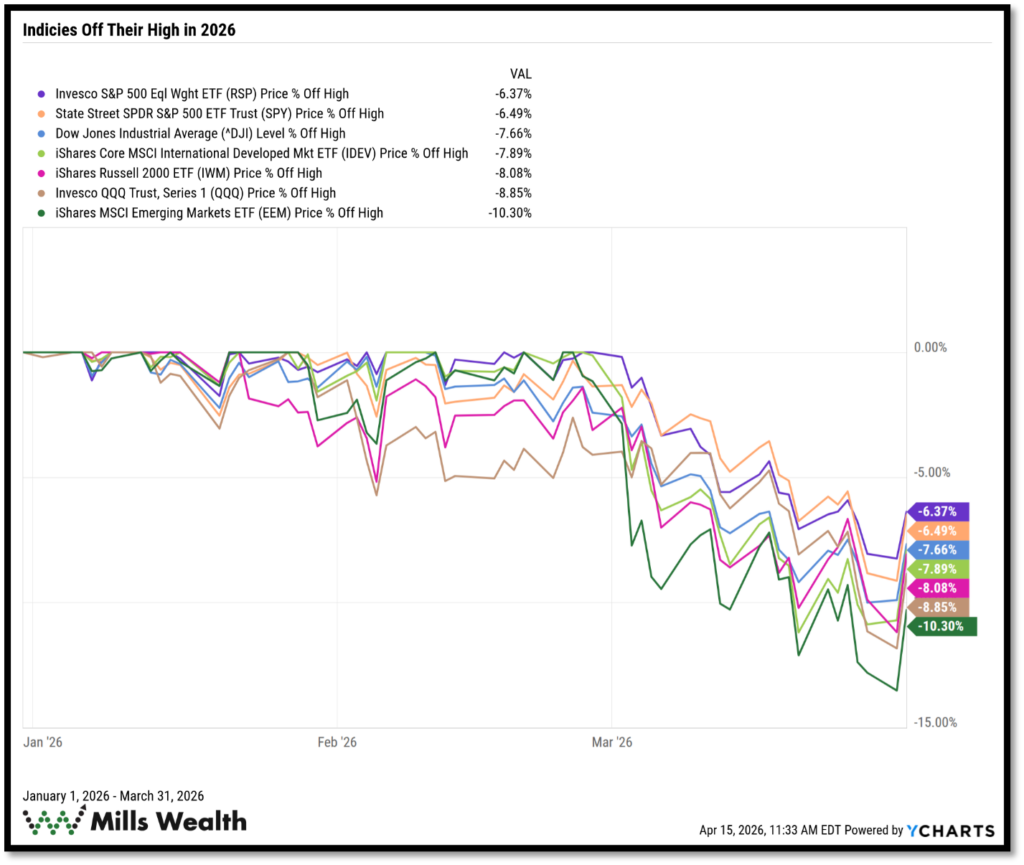

The markets have had their fair share of ups and downs to start 2026, and we’re only in April. In recent history, midterm years have been years of volatility, and it seems that 2026 does not want to buck that trend. Add a conflict with Iran and continual unrest within our own borders, and, as you would expect, the market had quite the reaction.

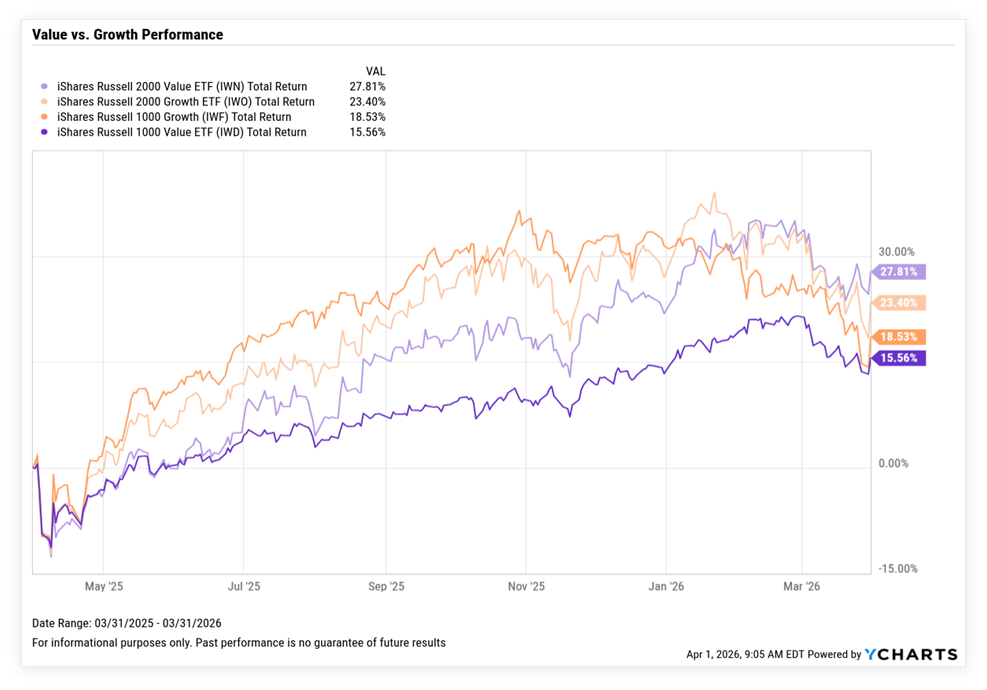

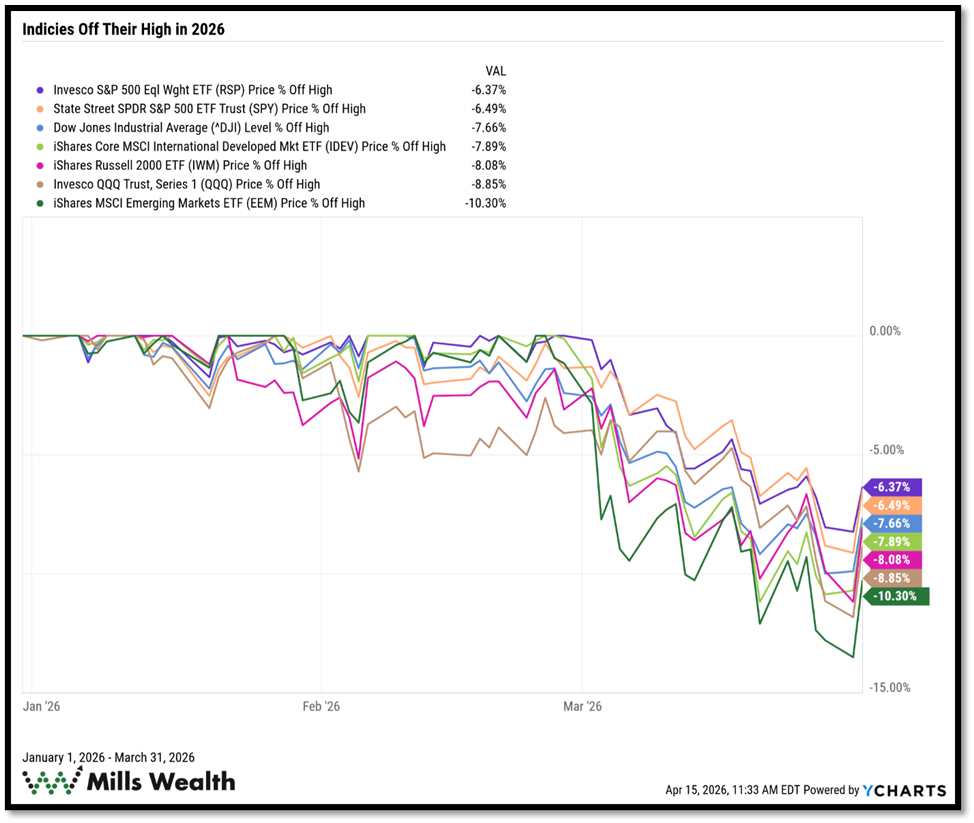

The stock market has been a tale of three cities to start the year. January started off with great returns from multiple places; International and Emerging Markets continued their great run, and US Small Caps joined in. Then, in February, we saw a slight pull-back or a stall, followed by a steep drop-off in March.

This quarter was the 2nd significant negative quarter since Q2 of 2022, along with Q1 of 2025. And just like the tariffs, it’s unclear if the market will continue upwards or fall back based on the geo-political tension in the middle east.

Please feel free to use the links below to navigate to the different sections of this newsletter.

SECTION I – Quarterly Market Review – Global & U.S. Performance Highlights

SECTION II – Mike’s Advisor Commentary, Questions, and Quotes

SECTION III – Tax Corner: Double Check Your Return

SECTION IV – Around The MWA Office

SECTION V – Pictures Worth Looking At

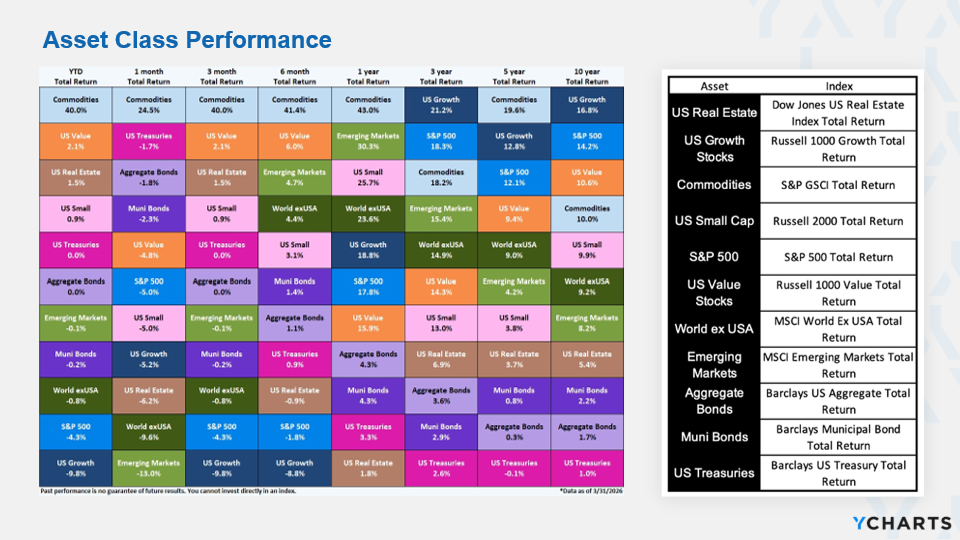

Quarterly Market Review – Global & U.S. Performance Highlights

The first quarter of 2026 presented a more challenging environment, with most major markets posting modest declines. The U.S. stock market led the downturn, falling -3.96%, followed by International Developed markets at -0.94% and Emerging markets at -0.17%. Fixed income markets were also slightly negative, with the U.S. Bond market down -0.05% and Global Bonds (ex-U.S.) declining -0.19%. Global Real Estate was the lone bright spot, delivering a positive return of 0.77% for the quarter. Despite the short-term weakness, all of these markets have generated positive returns over the past 1, 5, and 10-year periods (which is encouraging). To read the full Market Review Deck, CLICK HERE.

Mike’s Advisor Commentary, Questions, and Quotes

Markets have experienced significant volatility as investors wrestle with the economic and market consequences of the war with Iran. Stock prices, broadly speaking, have not fallen much relative to the size of the potential disruption. I believe the oil shock has the potential to last longer than the market currently expects — both sides appear too far apart to agree to a cease fire. A prolonged conflict could force higher oil prices, sustained inflation, and eventually higher interest rates that pressure valuations. The flip side is also true: if the President negotiates a truce, stocks could rally on lower rate expectations (particularly in growth stocks that have been hurt most by inflation fears).

I’m no futurist, but my classmates from the Academy — people who have spent careers thinking about these things — would take the “over” not the “under” on how long this skirmish lasts. After all, Iran and its predecessors have been fighting over that same strait for over a thousand years. As with many complex systems, we want to build portfolios that can succeed in either scenario.

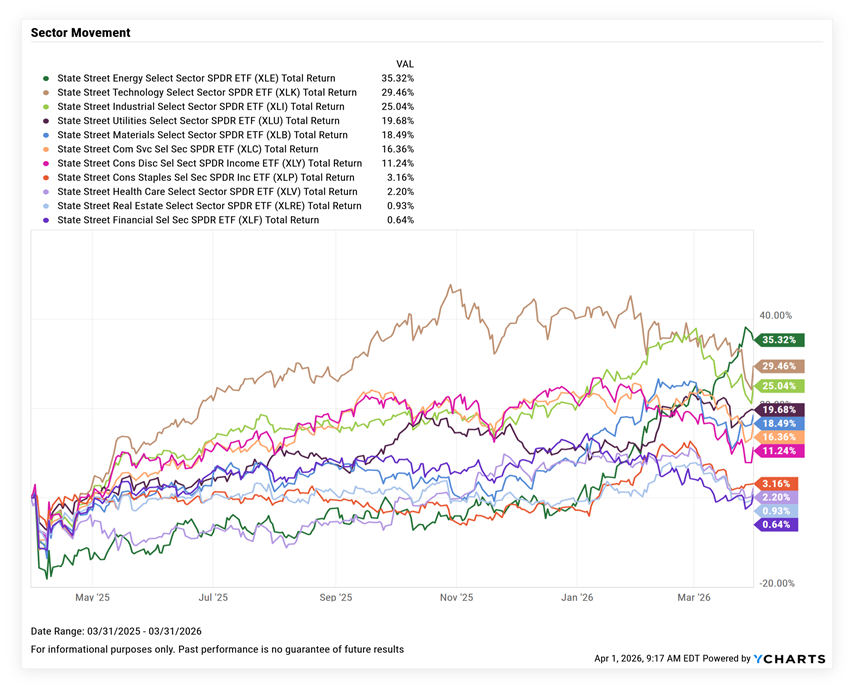

While the broad market is only down slightly, the software sector has fallen nearly 40% on AI fears and valuation compression from higher rates. The largest Mag 7 stocks have repriced from roughly 33x forward earnings to a more reasonable 24x. Six of these seven companies are among the finest businesses ever built and appear far more investable at these levels. Diversification has continued to be rewarded.

The Macro Backdrop: A New Playbook Is Required

Jeffrey Gundlach of DoubleLine Capital recently offered a sobering assessment that resonates with us: the assumptions that guided portfolios for the past two decades may no longer apply. Fiscal imbalances, structurally sticky inflation, and a weakening dollar are rewriting the rules. After thirty years in this business, I find his framing hard to argue with. [5]

On U.S. equities, Gundlach has been unusually blunt — suggesting it may be time to “call it a day” on simply riding the S&P 500. At a price-to-book of 5.6x versus roughly 2.3x for non-U.S. markets, domestic large-cap stocks carry a premium that history suggests is difficult to sustain. Passive flows into a handful of mega-cap names have amplified this distortion. We have been making this same observation in these letters for some time. [5]

On inflation and rates, his preference is for high-quality bonds in the short-to-mid duration range rather than long Treasuries or broad high yield. We also share that view. Additionally, he has issued a clear warning on private credit, which has ballooned to rival the size of the entire high-yield market — describing conditions there as extremely optimistic. We don’t have exposure to private credit, but we would caution you to be careful if you are heavily weighted there. For clients with private credit exposure elsewhere, this is worth a conversation. [5]

Real Assets: Still Early

Gundlach’s strongest conviction is in gold and real assets, describing gold as potentially on a “moonshot” as investors lose confidence in central bank credibility and U.S. fiscal responsibility, with central bank buying continuing at a pace not seen in decades. [5] Goehring & Rozencwajg (a manager we have liked for some time) and Cohen & Steers have both reinforced this view, arguing that despite large moves in some resource stocks, most commodities remain well below their inflation-adjusted historical highs and resource equities remain extremely inexpensive relative to the broader market. Years of underinvestment may have laid the groundwork for a longer-lasting commodity bull market than most expect. [1]

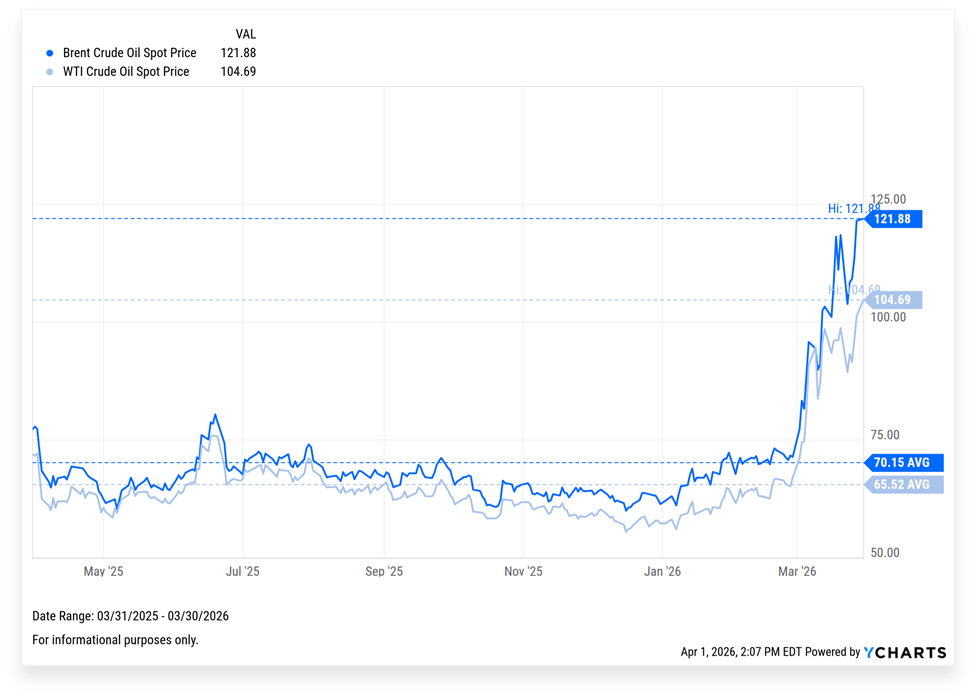

The effective closure of the Strait of Hormuz has created one of the largest physical energy disruptions in modern history, affecting roughly 20% of global oil flows. Goehring & Rozencwajg argue the market was already tighter than widely believed — the spike toward $120 oil reflected a tight market colliding with aggressive short covering, not just headlines. Tactically, they currently favor oil and gas over precious metals in the near term, while gold remains a core long-term holding for protection against fiscal excess and monetary debasement. [1][2][4]

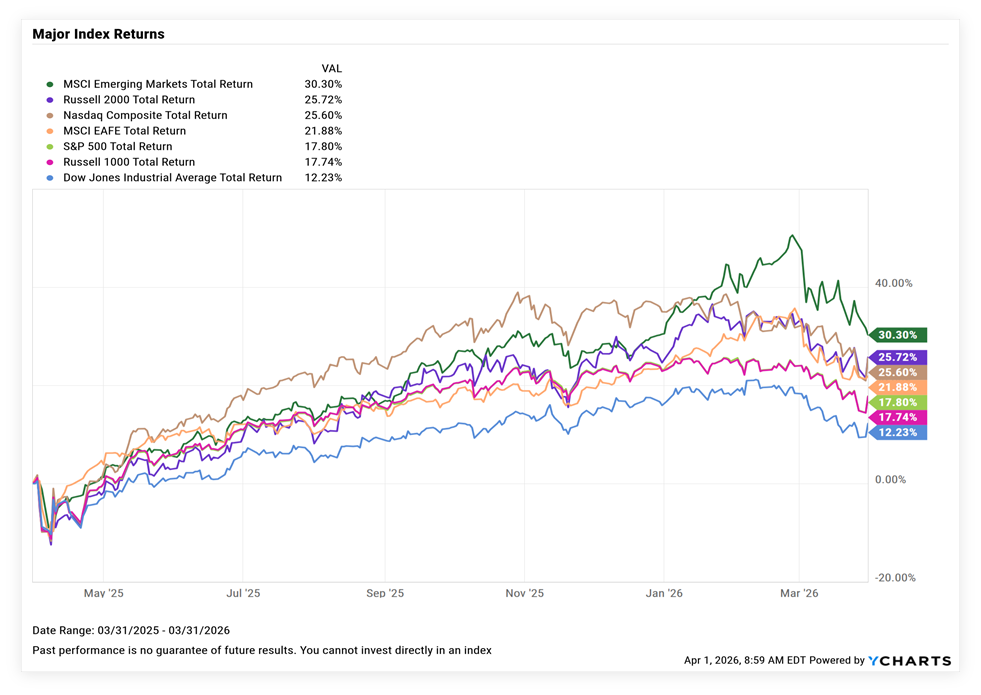

International stocks had a strong 2025 and, as markets rebound, we think in a lower priced oil environment these markets probably beat the US on momentum and low valuations. If energy stays high, there will be winners and losers.

Mark Cooper (long /short manager of MAC Alpha) points out how much more international value stocks will need to travel just to get to average valuations. International stocks, particularly small caps and value-oriented companies, are trading at some of the cheapest relative levels in decades and would need to return about 25%/year over 5 years to get back to their average over the last 50 years. His team highlights Japan and selected industrials outside the U.S. as particularly attractive. [3]

We also see growing opportunity in software and selected growth businesses that have sold off sharply. Periods of technological disruption often create both genuine losers and mispriced survivors — and that is where valuation discipline matters most.

Where This Leaves Us

We are holding our defense and exercising patience while markets digest war risk and a potential transition in market leadership. However, we are actively preparing for opportunity. If volatility creates better entry points, we would look to deploy capital into selected software businesses, international and value-oriented equities, energy and commodity-linked exposures, and other areas that could benefit from mean reversion and a weakening dollar.

The macro regime is shifting. The old playbook — own U.S. large-cap growth, trust the Fed, ignore the dollar — deserves serious scrutiny. We are doing that work every day on your behalf.

As always, our goal is not to predict every short-term move. Instead, we aim to position portfolios thoughtfully so that clients can participate in long-term opportunity while maintaining the resilience to navigate genuine uncertainty.

–Mike Mills & the Mills Wealth Team

Bibliography

[1] Leigh R. Goehring & Adam A. Rozencwajg, “When the Strait Closed: The Commodity Bull Market Has Barely Begun,” Goehring & Rozencwajg Q4 2025 Market Commentary, March 13, 2026.

[2] Adam Rozencwajg, “The Hormuz Supply Shock,” Goehring & Rozencwajg Blog, March 20, 2026.

[3] Mark Cooper, “VALUE: After Hours (S08 E13),” The Acquirer’s Multiple, April 12, 2026.

[4] Leigh Goehring, “Why Gold and Silver May Be the Last Defense Against Inflation and Debt,” Goehring & Rozencwajg Blog / VRIC Podcast, February 19, 2026.

[5] Jeffrey Gundlach, “Just Markets ‘Clue’ Webcast / Round Table Prime / Gundlach Unlocked,” DoubleLine Capital, January–March 2026.

Tax Corner: Double Check Your Return

Most people believe the IRS has three years to audit a tax return. In most cases, that’s true. But there are situations where that clock never runs out.

A recent case, Murrin v. Commissioner, highlights an important rule under Internal Revenue Code Section 6501(c)(1): if a return is considered fraudulent, the IRS can assess tax at any time. There is no statute of limitations.

In this case, the taxpayers hired a professional to prepare their returns. Years later, the IRS determined that the preparer had inserted fraudulent items without the taxpayers’ knowledge. The taxpayers argued that the unlimited audit window shouldn’t apply since they didn’t commit the fraud themselves.

The court disagreed. Because the return itself was fraudulent, the IRS was allowed to go back indefinitely, regardless of who caused the issue.

That’s the part that matters. This isn’t a new law, but it’s a reminder of how broadly it can apply. You are responsible for what gets filed under your name.

Hiring a CPA doesn’t transfer that responsibility. It adds expertise, but it doesn’t remove your exposure. For business owners and high-income households, this becomes even more important. The more complex the return, the more room there is for something to be misunderstood or done incorrectly.

The practical takeaway is simple. Review your return before signing it. Ask questions when something doesn’t make sense. Make sure you understand the major positions being taken.

It’s also one of the reasons we spend time reviewing client tax return. We’ll often run them through our internal systems to identify planning opportunities, inconsistencies, and areas that may deserve a closer look.

This isn’t about second-guessing your CPA. It’s about having another layer of insight and making sure everything lines up with your broader financial plan.

Because if there’s ever an issue, the IRS isn’t going to call your preparer first—they’re going to call you.

In the coming weeks we will be reaching out to you and your CPA to gather your 2025 tax return and run it through our system.

We will use that data for our meetings in the 3rd and 4th quarters to make sure that we are utilizing all available planning options for you.

Please feel free to upload your return HERE if you’d like to get it to us sooner.

Around the MWA Office

Back by popular demand, we are hosting our 2nd annual Kentucky Derby at Mike and Sheri Mills house on May 2nd at 4:45 PM. If you live in Texas, you should have received an invite. But, in case you didn’t, here is the invite link.

Along with this, in our annual client survey many of you requested opportunities to learn more in person and via web conference. We are working on a webinar for Q2, so be on the lookout for that evite as well.

Touching on the client survey from November, if you did not receive our email response or catch the video we created around it, here is the video link.

Thank you again for your participation and your continued trust in us.

Pictures Worth Looking At