(And What You Should Actually Pay)

Good financial advice earns its keep. Planning, tax strategy, investment discipline, a steady hand when the market throws a tantrum, all of it adds real value. How an advisor charges for that work, and how much, shapes everything else about the relationship.

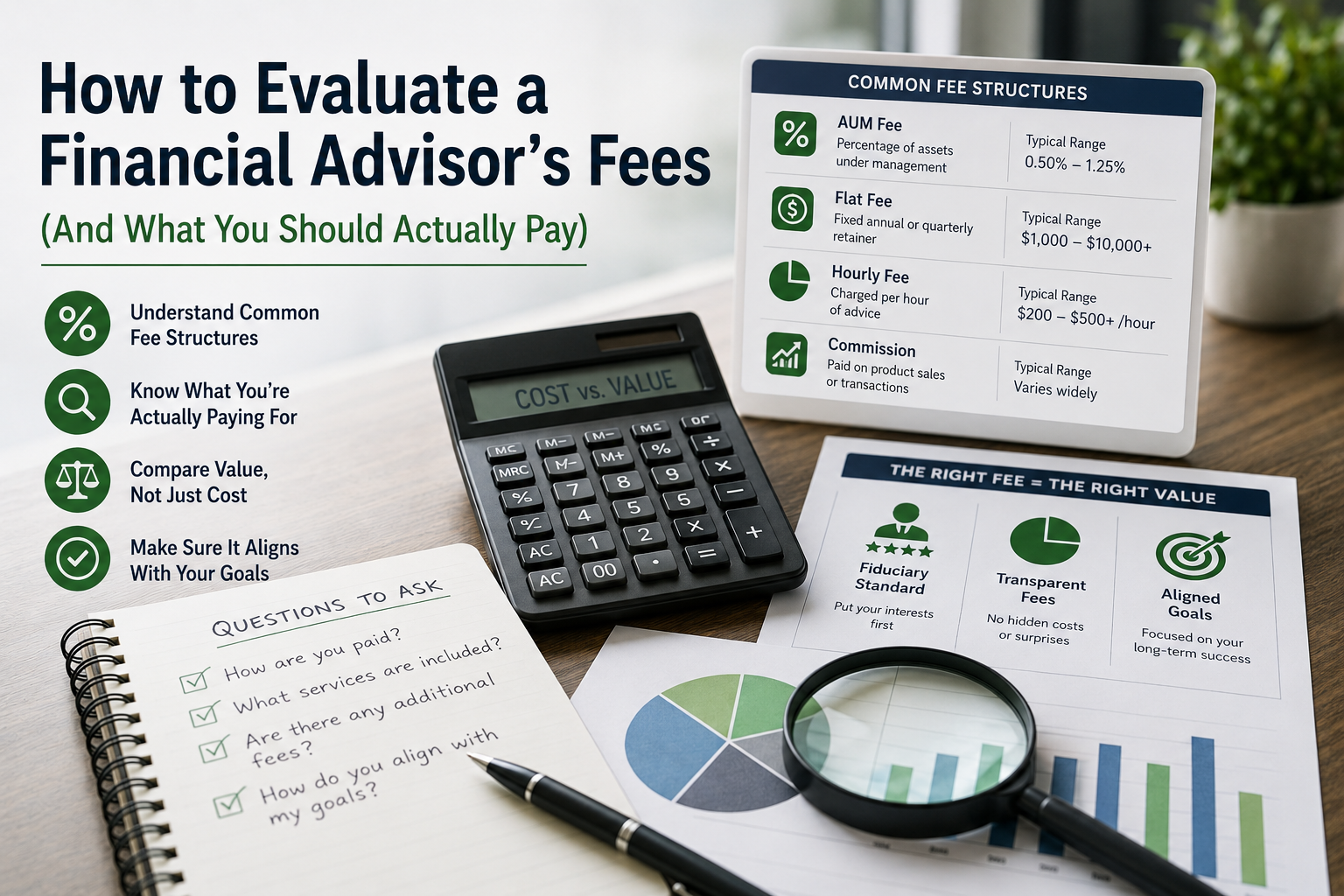

The Four Fee Models

• Assets under management (AUM). The advisor takes a slice of the portfolio they manage, usually 0.50 to 1.25 percent a year. The default model in the industry and the easiest to understand at a glance.

• Flat retainer. A fixed annual fee, typically $2,000 to $10,000, no matter the portfolio size. The bigger your account, the better the math. Often the winner past roughly $1.5 million.

• Hourly. Bills like a lawyer: $200 to $500 an hour. Perfect for a one time plan, a second opinion, or a single thorny question.

• Commission. The advisor earns a payment when you buy a specific product, often an annuity or insurance contract. Ask exactly how the math works so you know the true cost of each recommendation.

Why Fees Matter

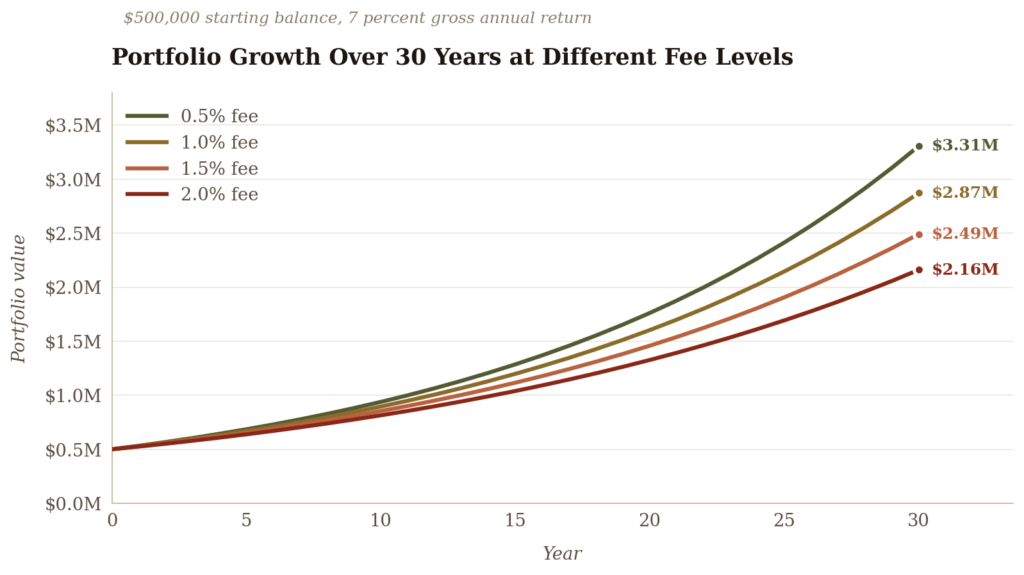

Fees compound. Returns get all the attention, but fees quietly do the same math in the opposite direction. On a $500,000 portfolio earning 7 percent a year, the gap between paying 0.5 percent and 1.5 percent over thirty years works out to roughly $815,000. That is not a typo.

Figure 1: Portfolio growth over 30 years at different fee levels ($500,000 starting balance, 7 percent gross return)

Good advice earns its fee. A Roth conversion timed at the right moment, a calm hand through a 30 percent drawdown, or a single smart tax move can pay back years of advisory billing in one decision. The cheapest advisor rarely wins. Cost matters; what you get for it matters more.

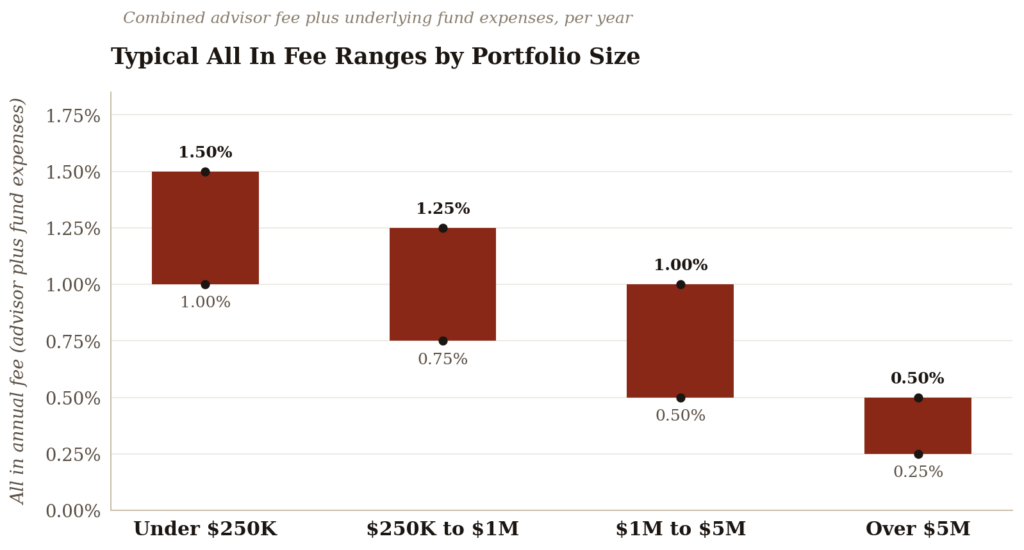

What You Should Expect to Pay

Fees scale with portfolio size and the complexity of your situation, and the market has organized itself into reasonably clean bands. Between $250,000 and $1 million, expect 0.75 to 1.0 percent all in. Past $1 million, push toward 0.5 to 0.75 percent. A standalone financial plan from a qualified planner usually runs $2,500 to $7,500 as a project fee.

The rate matters less than what comes with it. A strong advisor delivers portfolio management, retirement projections, tax coordination with your CPA, estate planning input, and at least one full review a year. The best ones throw in cash flow planning, insurance analysis, and the occasional family meeting. Get the scope in writing and comparing two offers becomes almost fair.

Five Questions to Ask Before You Sign

Bring these to your first meeting. A good advisor answers each one plainly and welcomes the conversation.

- What is my total annual cost, including fund expenses and platform fees?

- Do you act as a fiduciary one hundred percent of the time, in writing?

- How do you get paid beyond what I pay you directly?

- What services are included at this fee, and what costs extra?

- Can you show me, in dollars, what working with you will cost over twenty years?

Choosing well comes down to knowing what you pay and what you get for it. A good advisor makes that part easy.