Nestled into the DFW Metroplex, near Dallas/Fort Worth International airport, Grapevine, Texas offers the charm of a historic downtown, highly rated schools, and low crime. Paired with easy access to both Fort Worth and Dallas, without the congestion or costs associated with living in either city, the value of this location really speaks for itself. For families already here, that’s a lifestyle worth protecting financially. For those considering a move it’s a community worth planning toward carefully.

As a financial planner in Grapevine TX, we work with both groups every day. Many of the questions we receive stay the same. How do we afford a home here? How do we pay for school? How do we build something that lasts?

Understanding Grapevine’s Real Estate Market

Grapevine’s housing market is competitive, and it has remained resilient even as broader DFW markets have fluctuated. Median home prices have generally ranged from the mid-$400,000s to over $600,000 depending on neighborhood, school zone, and proximity to Lake Grapevine or Historic Downtown. This often positions Grapevine higher than neighboring cities like Euless or Hurst, but it also tends to remain more accessible than Southlake or Colleyville.

Common Challenges Buyers and Current Owners Face

Limited inventory is the most consistent pressure in Grapevine. The city is largely built out, with fewer new developments compared to neighboring suburbs, so move-in-ready homes (especially those located in desirable school zones) receive multiple offers within days. This creates an urgency that can, at times, lead buyers to overextend financially. If you are currently renting in Grapevine and watching the market, this dynamic likely feels familiar.

Texas property taxes are the second major challenge. Grapevine falls within Tarrant County (with portions touching Dallas County), and effective property tax rates often range between 1.8% and 2.4% of assessed home value. For a $525,000 home, that is $9,450-$12,600 annually, before including mortgage principal or interest. Sometimes this can be a considerable adjustment for families relocating from states with lower property taxes.

Grapevine vs. Surrounding Cities: What You’re Actually Buying

Families weighing Grapevine against nearby options deserve an honest comparison. Higher home prices here don’t exist in a vacuum, they reflect specific, tangible advantages.

For many families, Grapevine represents the sweet spot: exceptional schools and quality of life without paying Southlake prices. Affordability is personal, and a careful budget analysis should always precede any home purchase decision.

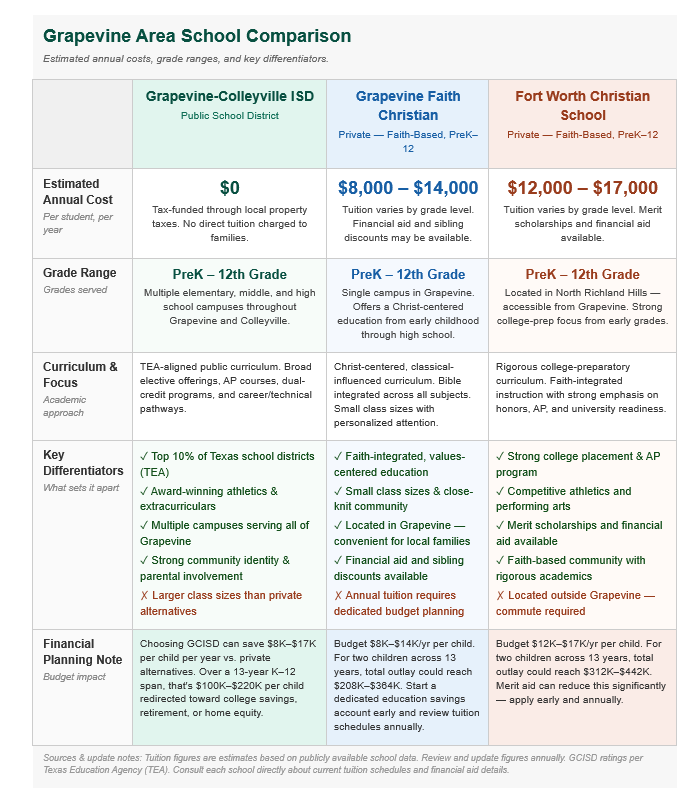

Planning Around Grapevine’s Schools

Education is one of the most financially significant factors in where a family chooses to live, and in Grapevine, the K-12 options are generally strong across both private and public schools. Understanding what each offers helps you plan not just your housing decision, but your overall education budget.

What Strong Schools Mean for Your Finances

Access to a top-rated public school is a benefit that can be easy to overlook. Families choosing Grapevine’s public schools may be avoiding $10,000-$17,000 per child per year in tuition. Over a 13-year span, that’s a substantial sum that could serve valuable alternative purposes including saving for college, retirement, or home equity.

For families who prefer private education for faith-based, academic, or other personal reasons, the financial planning picture shifts meaningfully. Budgeting for private school tuition while also saving for college requires deliberate planning well before your child reaches kindergarten.

Saving for College: Wherever K-12 Takes You

Regardless of which path you choose, college costs continue to climb. A four-year Texas public university runs $25,000-$30,000 per year, all in. A 529 Savings Plan offers the most tax-efficient tool available. With this tool, contributions grow tax-free, and withdrawals for qualified education expenses are never taxed. Under recent law changes, unused 529 funds can be rolled into a Roth IRA (if they are held in the vehicle for the required period). With this allowance, up to $35,000 can be rolled over, which lightens the burden of the “what if they don’t go to college” concern.

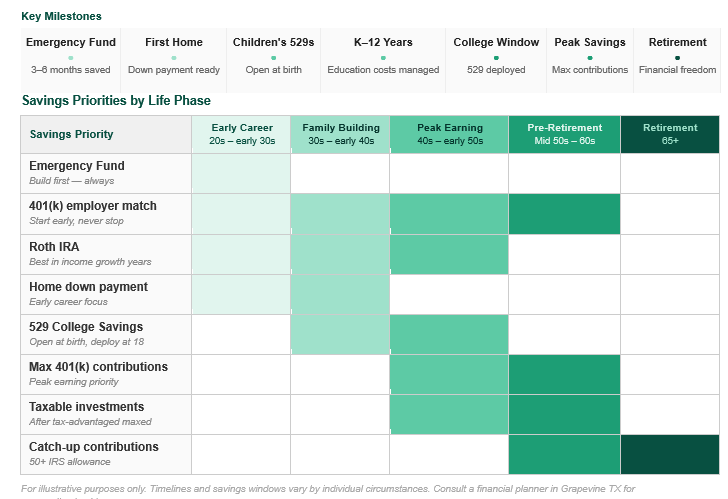

Setting Meaningful Long-Term Financial Goals

Oftentimes, the families we work with come to us looking for solutions for goals that are vague. They tell us that they are aiming to “retire comfortably” or “have enough saved”. The intentions are great, but we know our clients arrive seeking action and the uncertainty of what they want can delay the action they need to take. From our perspective, effective financial goals share four qualities: they are specific, measurable, they exist on a defined timeframe, and they are reasonable given your personal financial situation.

Here is a framework that works for many families:

- Name the goal precisely. Example: “fund four years at a Texas public university for our daughter, starting in August 2037, expecting $120,000 total in today’s dollars.”

- Attach a number and a date to all goals. A timeline without a dollar value is a wish. A dollar value without a timeline cannot be planned for.

- Check your goal against your current financial picture. Is it realistic now? Would it be realistic if a piece of your situation were to change?

- Decide how important your goal is, and how it compares to others. Rank the priorities of what you want to do with your money throughout your life. Considering timelines in this stage can be valuable.

- Review annually. Life changes: income grows, expenses fluctuate, goals evolve. Oftentimes, a plan you don’t revisit becomes a plan that no longer fits.

Family Financial Goal Timeline

Retirement: Simple Rules to Stay on Track

A reasonable target for most families is saving 15% of gross income toward retirement, including any employer match. If you are in your 30s with a 401(k) balance that feels behind, you are not alone. Catching up is normally possible with consistent contributions and time. A Roth IRA offers tax-free growth and can be a valuable resource for families that expect their income to increase over time.

Another foundational piece to savings can be an emergency fund that covers 3-6 months of expenses. If this is in an accessible place with growth exposure, like a high yield savings account or in a money market fund, you can use this as a safety net for whatever life throws your way. Without this, a single unexpected event such as job loss, medical bill, or major home repair could force you into debt or derail years of investment progress.

A Final Word-for Residents and Newcomers Alike

If you’re already in Grapevine, you’ve made a sound community choice. The work is now ensuring your financial plan is as strong as the community around you. If you are considering moving here, remember the financial planning starts before the moving truck. To thrive here, make sure you understand what this market requires, what the schools may cost or save you, and what goals you need to support your decision.

Either way, the path forward is the same: start with a clear picture of where you are, define where you want to go, and build a realistic, step-by-step plan between the two. Working with a financial planner in Grapevine, TX who understands the local market, Texas tax rules, and the real cost of raising a family in this community can make that path significantly shorter, while also giving you confidence in your ability to build the future you want.

Ready to take the next step? Schedule a conversation with our team to talk through your goals and build a plan that fits your family.