Two account types. Different costs, different relationships, different outcomes. Here’s how to choose wisely.

Whether you’re just beginning your investment journey or rethinking how you manage your wealth, the choice between a brokerage account and an advisory account is one of the most consequential decisions you’ll make — and one that most people make without fully understanding the difference.

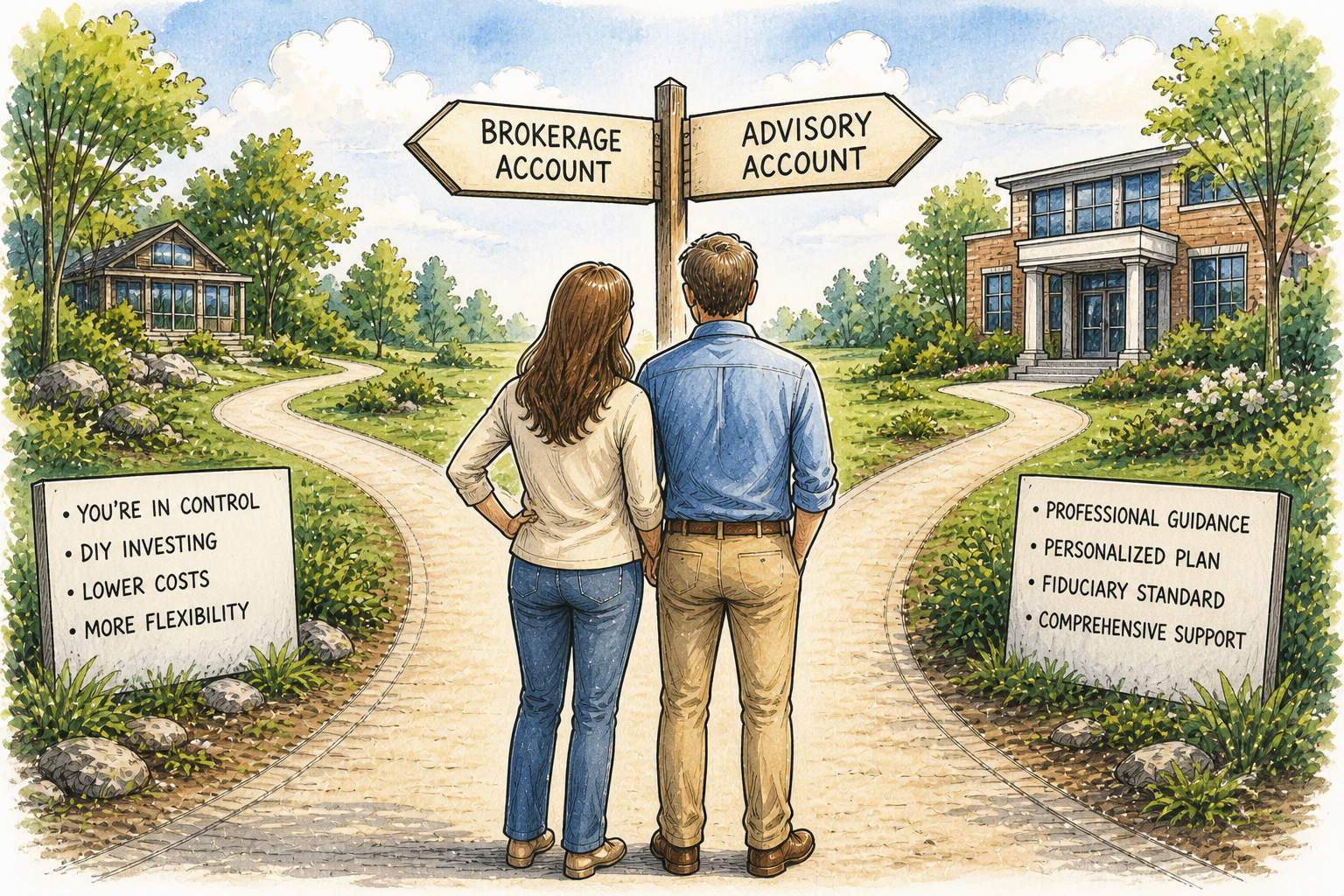

Both account types let you invest in stocks, bonds, funds, and other securities. But they operate on fundamentally different models: one puts you in the driver’s seat, the other hands the wheel to a professional. And their cost structures are just as different as their philosophy.

The Core Distinction: Brokerage vs. Advisory Accounts

The Self-Directed Brokerage Account

A self-directed account where you make all investment decisions. Your broker executes trades on your behalf but is not required to act in your best interest beyond the suitability standard. You own the assets; you call the shots.

The Fiduciary Advisory Account (RIA)

A managed account where a registered investment advisor (RIA) or advisory firm makes investment decisions on your behalf — typically under a discretionary or non-discretionary arrangement. Advisors are held to a fiduciary standard, legally obligating them to act in your best interest.

The fiduciary distinction matters more than it might initially seem. Brokers operate under a “suitability” standard — they must recommend products that are suitable for you, but not necessarily the best or lowest-cost option. Advisors, by contrast, must prioritize your interests above their own compensation. This affects everything from product selection to fee transparency.

“Suitability means the shoe fits. Fiduciary means it’s the best shoe for the run you’re doing.”

Understanding the True Costs and Hidden Fees

This is where most investors are surprised. The fee structures for these accounts are structurally different — and getting this wrong can cost you tens of thousands of dollars over a lifetime of investing.

| Fee Type | Brokerage Account | Advisory Account |

|---|---|---|

| Transaction-Based / Trade Commissions | $0 at most major online (DIY) brokers and 0.50%–2.50% of the principal value, subject to minimum charges at most wirehouses. Bond trades often include a 1–3% markup (or down) in the price paid (or received) per transaction. Options typically incur a fee of $0.50–$0.65/contract, subject to minimums. Mutual fund trades: Vary for each transaction depending on fund family, share class, and amount being invested. | Usually bundled into the advisory fee — no per-trade charge, ranging between 0.50%–2.00% annually. Some wrap accounts explicitly include commissions in the Asset Under Management (AUM) fee. |

| Management / Advisory Fee | None — you manage it yourself. Robo-advisors: 0%–0.25% AUM/year (e.g., Schwab Intelligent Portfolios, Fidelity Go). | Typically 0.25%–1.5% of assets under management (AUM) per year. Full-service advisors: 1%–2% AUM. Fee-only advisors may charge $2,000–$10,000+/year flat or $200–$500/hour. |

| Expense Ratios (Underlying Funds) | DIY investors can choose ultra-low-cost index funds. 0.03%–0.20% annually. No markup. | Advisors may place clients in actively managed funds with higher ratios (0.5%–1.5%), though fee-only advisors typically use low-cost index funds. |

| Account Minimums | $0 at most major online brokers. Fractional shares allow investing with any amount. | Robo-advisors: $0–$5,000. Human advisors: typically $100,000–$1,000,000+ minimum investable assets. |

| Other Potential Costs | Margin interest (if applicable), options fees, wire transfer fees, inactivity fees at some brokers. | Planning fees for financial plans, tax prep, estate coordination. Some advisors also earn commissions on insurance/annuity products. |

To put the AUM fee in perspective: a 1% annual advisory fee on a $500,000 portfolio is $5,000 per year. Over 20 years, even accounting for growth, that compounding fee drag can reduce your final balance by $100,000–$300,000 depending on returns — a figure that deserves serious consideration.

This is why the conversation about fees can’t end at the percentage. A 1% AUM fee is reasonable when it funds proactive tax planning, estate coordination, and risk management — services that typically save or earn back the fee many times over. But a 1% fee for portfolio management alone, with no broader planning attached, is overpaying. The question isn’t whether 1% is too much — it’s what you’re getting for it.

Which Account Type Is Right for Your Financial Situation?

The honest answer is that neither account type is universally better. The right choice depends on your financial complexity, time availability, investment knowledge, and how you react to market volatility.

| Brokerage Accounts Tend to Fit | Advisory Accounts Tend to Fit |

|---|---|

| • Those using a simple, passive index fund strategy (e.g., a three-fund portfolio) • Investors comfortable researching and selecting their own funds or stocks • Younger investors building wealth who have time to learn • Cost-conscious investors who want to minimize fee drag over decades • Traders using individual stocks, ETFs, or options • High-income earners with straightforward financial situations • Tech-savvy individuals comfortable with robo-advisor platforms • Investors who want tax-loss harvesting control on their own terms | • Retirees needing coordinated withdrawal, Social Security, and RMD strategies • Investors with complex financial situations: business ownership, stock options, trusts, or inheritance • High-net-worth individuals ($1M+) where personalized tax planning adds measurable value • Those who become emotional or reactive during market downturns and need behavioral coaching • Busy professionals who lack the time or inclination to manage investments • People navigating major life transitions: divorce, sale of a business, sudden wealth • Investors in high tax brackets who benefit from sophisticated tax strategies and municipal bonds • Those with concentrated stock positions needing careful diversification strategies |

The Robo-Advisor Middle Ground

It’s worth noting that robo-advisors occupy an interesting middle ground. Platforms like Betterment, Wealthfront, Schwab Intelligent Portfolios, and Fidelity Go provide automated, algorithm-driven portfolio management at advisory account-like efficiency — but at brokerage-level costs (0%–0.40% AUM annually).

For investors who want hands-off management without paying for a human relationship, a robo-advisor is often the optimal choice. They handle rebalancing, dividend reinvestment, and in some cases automated tax-loss harvesting. What they can’t replace is human judgment in complex situations.

Questions to Ask Before Hiring an Advisor

Before opening either account, be honest with yourself about the following:

For a brokerage account: Do I have the knowledge and discipline to build and stick to a long-term investment plan? Will I panic-sell when markets drop 30%? Am I willing to spend time annually reviewing my allocation?

For an advisory account: Is my financial life complex enough to justify the fee? Is my advisor a fiduciary? How are they compensated — fee-only, fee-based, or commission? What specific services am I getting beyond portfolio management?

The Bottom Line for High-Net-Worth Investors

If you’re an investor with a relatively straightforward financial picture and the willingness to learn the basics, a self-directed brokerage account with low-cost index funds can potentially outperform a managed account on a net-of-fees basis over time. Lower costs compound into meaningfully higher returns.

But for investors with complex estates, concentrated wealth, behavioral tendencies that work against them, or genuinely complicated tax situations, a quality fiduciary advisor can deliver value that far exceeds their fee. The key is knowing which camp you’re in — and being honest about it.

At Mills Wealth Advisors, we think the best place to start is just an honest conversation. We’re a fiduciary firm, which means we’re always working in your best interest — no hidden agendas, no product pushing. Whether you’re dealing with a complex estate, a big liquidity event, a tangled tax situation, or you just want a real financial plan you can actually follow through on, we’re here to help you figure it out. And if you’re not sure whether you even need an advisor? That’s a great reason to reach out.

We offer complimentary consultations, and we’re happy to give you a straight answer either way. Come find us in Southlake or give us a call — we’d love to meet you.