When business owners first hear the term “cash balance plan,” their reaction is often the same. They assume it must be some highly complex retirement strategy reserved for doctors, attorneys, or executives at large corporations. The name itself sounds intimidating. Add in phrases like “defined benefit plan” and “actuarial calculations,” and many business owners immediately decide it’s probably more trouble than it’s worth.

In reality, most solo cash balance plans are far less complicated than people imagine.

That doesn’t mean they’re simple. A cash balance plan is certainly more involved than opening an IRA or contributing to a SEP IRA. There are additional rules, annual filings, and calculations that need to be completed. However, many business owners are surprised to learn that the vast majority of the complexity is handled by professionals behind the scenes. From the owner’s perspective, a cash balance plan often functions much like any other retirement account. Contributions are made, investments are managed, and tax deductions are received.

The real question isn’t whether a cash balance plan is complex. The real question is whether the benefits justify the additional administration. For many successful business owners, the answer is yes.

What Is a Solo Cash Balance Plan?

A cash balance plan is a type of qualified retirement plan that allows business owners to make significantly larger tax-deductible contributions than they can typically make through a traditional 401(k), SEP IRA, or SIMPLE IRA.

Technically, it falls under the defined benefit plan category. However, unlike the traditional pensions many people think of, a cash balance plan is presented more like an account balance that grows over time. While there are calculations happening behind the scenes, most business owners simply see a contribution amount, a balance, and the tax deduction that comes with it.

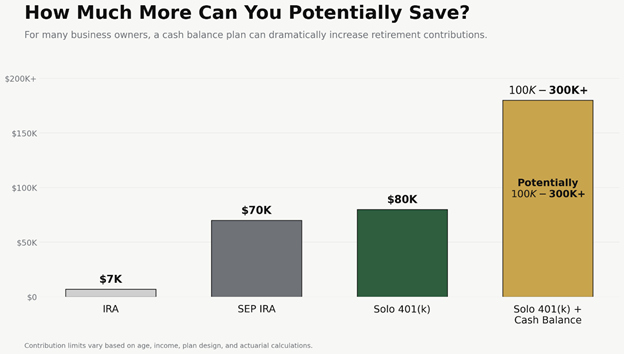

The amount you can contribute is based on factors such as your age, income, and retirement objectives. In many cases, business owners who have already maxed out their 401(k) can potentially contribute an additional six figures annually through a cash balance plan.

That is what makes these plans so attractive. They create an opportunity to accelerate retirement savings while generating substantial tax deductions along the way.

Why Business Owners Start Looking at Cash Balance Plans

Most business owners don’t wake up one morning and decide they want a cash balance plan.

Usually, they reach a point where the business is performing well, cash flow is strong, and taxes have become one of their largest annual expenses. They’ve already implemented many of the more common planning strategies. They’re contributing to their 401(k), funding investment accounts, and doing everything their CPA has recommended.

Yet every year they still find themselves writing large checks to the IRS.

At that point, the conversation often shifts from finding deductions to finding bigger deductions.

That’s where a cash balance plan enters the picture.

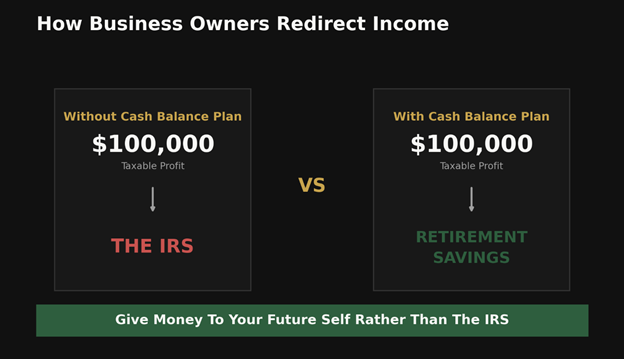

Rather than paying taxes on income today, a business owner can redirect a portion of those dollars into a retirement account that benefits their future while creating a current-year deduction. Depending on the circumstances, that deduction can be substantial.

For the right business owner, the tax savings alone can make the strategy worth exploring.

Where the Complexity Actually Exists

The biggest misconception surrounding cash balance plans is that the business owner is somehow responsible for understanding every technical aspect of the plan.

That simply isn’t true.

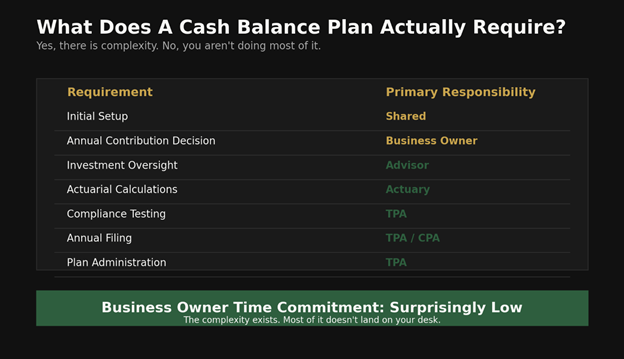

Yes, there are actuarial calculations involved. Yes, there are annual compliance requirements. Yes, there are funding ranges and regulatory rules that need to be followed.

But the business owner isn’t sitting at their desk performing actuarial calculations.

The actuary handles the calculations.

The third-party administrator handles the compliance work.

The custodian handles the account administration.

Your CPA coordinates the tax reporting.

And your financial advisor helps bring all of those moving pieces together.

The complexity is real, but most of it happens behind the curtain.

Think about it this way. The tax code is incredibly complicated, but most business owners don’t spend their weekends reading IRS regulations. They hire professionals to handle the complexity for them. The same principle applies here.

The Role of a Financial Advisor

One of the biggest advantages of working with an advisor who regularly implements cash balance plans is that they can manage much of the process on your behalf.

A good advisor helps coordinate with the actuary, the third-party administrator, the custodian, and your CPA. They help determine whether a cash balance plan is even appropriate in the first place. They assist with plan design, contribution strategies, investment allocation, and ongoing monitoring.

Most importantly, they help make sure the plan continues to align with your overall financial goals.

When business owners hear about cash balance plans, they often focus on the technical details. What they should really be asking is whether they have the right team in place to handle those details.

Because if you do, much of the complexity never reaches your desk.

Understanding the Trade-Offs

No planning strategy is perfect, and cash balance plans are no exception.

There are administrative costs associated with maintaining the plan. Contributions generally need to be made on an ongoing basis. There are funding obligations that don’t exist with simpler retirement plans.

Those considerations matter.

However, they should be evaluated alongside the benefits.

If a business owner contributes $200,000 and saves tens of thousands of dollars in taxes while accelerating retirement savings, the annual administration costs often become relatively insignificant in the bigger picture.

Too often, business owners focus on the existence of complexity rather than the value created by navigating that complexity.

The goal isn’t to find a strategy with no moving parts.

The goal is to find a strategy where the benefits meaningfully outweigh the effort required.

Why Solo Business Owners Often Benefit the Most

Cash balance plans become particularly attractive when the business owner has no employees or only a spouse working in the business.

When employees are involved, plan design becomes more complicated because benefits may need to be provided to eligible participants. That doesn’t mean cash balance plans stop making sense, but it does change the economics.

For solo business owners, the structure is often much cleaner.

The contributions primarily benefit the owner and potentially the spouse. The administration tends to be more straightforward, and the tax deductions can be substantial relative to the size of the business.

This is one reason cash balance plans are so common among consultants, physicians, attorneys, real estate professionals, and other highly compensated professionals operating owner-only businesses.

My Final Thoughts

I’ve noticed that many business owners automatically assume that the best tax strategies must be incredibly complicated. If they hear words like “defined benefit plan” or “actuarial calculation,” they immediately think it’s some advanced strategy that only works for billionaires or Fortune 500 executives.

The truth is that a solo cash balance plan is often much more practical than people expect.

Yes, there are rules. Yes, there are annual filings. Yes, there are professionals involved who help keep everything compliant. But compared to many of the moving pieces business owners already deal with every day, a cash balance plan is rarely the most complicated thing on their plate.

In fact, if you’re working with a financial advisor who regularly helps clients implement these plans, much of the complexity never reaches your desk. The advisor coordinates with the actuary, the third-party administrator, your CPA, and the custodian to keep everything moving in the right direction. The calculations get done. The compliance requirements get handled. The contribution recommendations get communicated.

From the business owner’s perspective, the process is often much simpler than people expect.

What I like most about these plans is that they solve a very specific problem. Many successful business owners reach a point where they are making good money, paying significant taxes, and looking for ways to save more for retirement. They’ve already maxed out their 401(k). They’ve already explored some of the more common planning opportunities. They simply need a way to put more money away while creating a meaningful tax deduction.

A cash balance plan can often accomplish exactly that.

At the end of the day, it’s really just another deduction your business gets to take. It’s a deduction that happens to come with the added benefit of building wealth for your future. Instead of writing another check to the IRS, you’re redirecting some of those dollars toward your own retirement goals.

Is it the right fit for everyone? Absolutely not. If your income fluctuates dramatically from year to year or you’re unsure whether you’ll have the cash flow to support ongoing contributions, there may be better options. But for the right business owner, it can be one of the most effective retirement planning tools available.

Sometimes good financial planning isn’t about finding the newest strategy or the most creative idea. Sometimes it’s about identifying a proven tool that has been around for years, understanding how it works, and applying it appropriately.

That’s exactly how I view a solo cash balance plan.

It’s not flashy. It’s not exotic. It’s not some secret tax loophole.

It’s simply a well-established planning strategy that helps many business owners save more, reduce taxes, and make meaningful progress toward their long-term goals.

And when I look at the tax savings, the additional retirement accumulation, and the amount of work that’s actually required from the business owner, I come back to the same conclusion every time:

The juice is worth the squeeze.