Most people are taught that debt is something to avoid.

Pay off your credit cards. Pay off your car. Pay off your house. Never borrow money if you can avoid it. If you follow that advice, you’ll probably stay out of a lot of financial trouble. You’ll avoid many of the mistakes that cause people to lose money, and you’ll likely sleep better at night knowing you don’t owe anyone anything.

For many people, that’s perfectly reasonable advice.

The problem is that avoiding debt entirely is not how many wealthy people build wealth.

Over the last 13 years, I’ve worked with everyone from young professionals just getting started to business owners completing eight-figure exits. One thing I’ve noticed is that successful investors rarely view debt as something that is inherently good or inherently bad. Instead, they view it as a tool. Like any tool, it can be incredibly useful when used properly and incredibly dangerous when used carelessly.

That’s an important distinction.

When most people talk about debt, they focus on the debt itself. I think they’re focusing on the wrong thing. In my experience, most people don’t actually have a debt problem. They have a risk management problem. The issue isn’t borrowing money. The issue is borrowing money without understanding the risks that come with it.

Debt Isn’t the Problem Most People Think It Is

When people get into financial trouble, it’s rarely because debt magically appeared and ruined their lives. Usually, there’s a series of bad decisions that happened long before the debt became a problem. Someone borrowed too much. Someone invested in the wrong opportunity. Someone convinced themselves that an investment couldn’t fail. The debt simply magnified the consequences.

That’s what leverage does.

It makes good decisions look better and bad decisions look worse.

When I hear someone say, “Debt is bad,” I understand where they’re coming from. If you’ve watched people get crushed by credit card debt, lose their homes, or file bankruptcy because they borrowed too much money, it’s easy to reach that conclusion. But the reality is more nuanced than that.

The same tool that destroys one person’s financial future can help another person build significant wealth.

The difference is usually not the debt.

The difference is how it was used.

That’s why I don’t think the conversation should start with whether debt is good or bad. I think the conversation should start with risk. Before borrowing a dollar, you need to understand exactly what you’re risking, how much you’re risking, and what happens if things don’t work out the way you expect.

Because eventually, something won’t.

The Mistake That Actually Destroys Wealth

One of the biggest mistakes I see investors make is becoming overly concentrated in a single opportunity. They find a deal they love and slowly convince themselves that the normal rules don’t apply. The returns look attractive. The people involved seem competent. The market opportunity looks strong.

Before long, they’ve committed far more money than they should.

I’ve seen people put 20%, 30%, 40%, or even 50% of their net worth into one opportunity because they believed it was a sure thing. The problem is that there are no sure things. Every investment looks good before it goes bad. Nobody raises money by explaining all the reasons their investment might fail. They talk about the upside. They talk about the growth. They talk about the opportunity.

Very few people spend enough time talking about the downside.

That’s where investors get into trouble.

What I’ve found is that most financial disasters don’t come from one bad investment. They come from overexposure. Investors simply have too much riding on one outcome. When that outcome doesn’t happen, the damage becomes difficult to recover from.

That’s not a debt problem.

That’s a risk management problem.

The Framework We Use Before Taking On Debt

Whenever we’re evaluating a leveraged investment opportunity with a client, we focus on three questions.

- How much exposure are we taking?

- What asset are we buying?

- What happens if we’re wrong?

Those three questions eliminate a surprising number of bad decisions.

The goal isn’t to eliminate risk entirely. That’s impossible. Risk and return will always be connected. If you want the opportunity for higher returns, you’ll have to accept some level of risk along the way.

The goal is something much simpler.

We want to make sure one decision doesn’t permanently damage your financial future.

Rule #1: Avoid Devastation, Not Discomfort

The first thing we look at is exposure.

How much of your net worth is actually tied to this opportunity?

As a general rule, we don’t like seeing more than approximately 10% of someone’s net worth exposed to a single leveraged investment. Notice I’m not talking about the mortgage on your primary residence. I’m talking about investments where you’re intentionally taking risk in hopes of generating a return. Real estate developments. Private investments. Business acquisitions. Opportunities that may or may not work out.

The reason is simple.

If you lose 10% of your net worth, you’re going to feel it. Nobody enjoys losing money. It will be uncomfortable. But you’ll survive. If you lose 50% of your net worth, that’s a completely different situation. Now you’re potentially changing retirement plans, changing lifestyles, and changing long-term goals.

The distinction we’re trying to create is the difference between discomfort and devastation.

Good investors understand that losses are inevitable. Not every investment will work. Not every opportunity will be successful. The goal isn’t to avoid losses altogether. The goal is to make sure a loss doesn’t permanently take you out of the game.

The investors who build lasting wealth understand this better than anyone.

They’re not trying to hit home runs on every investment.

They’re trying to stay in the game long enough for compounding to do its work.

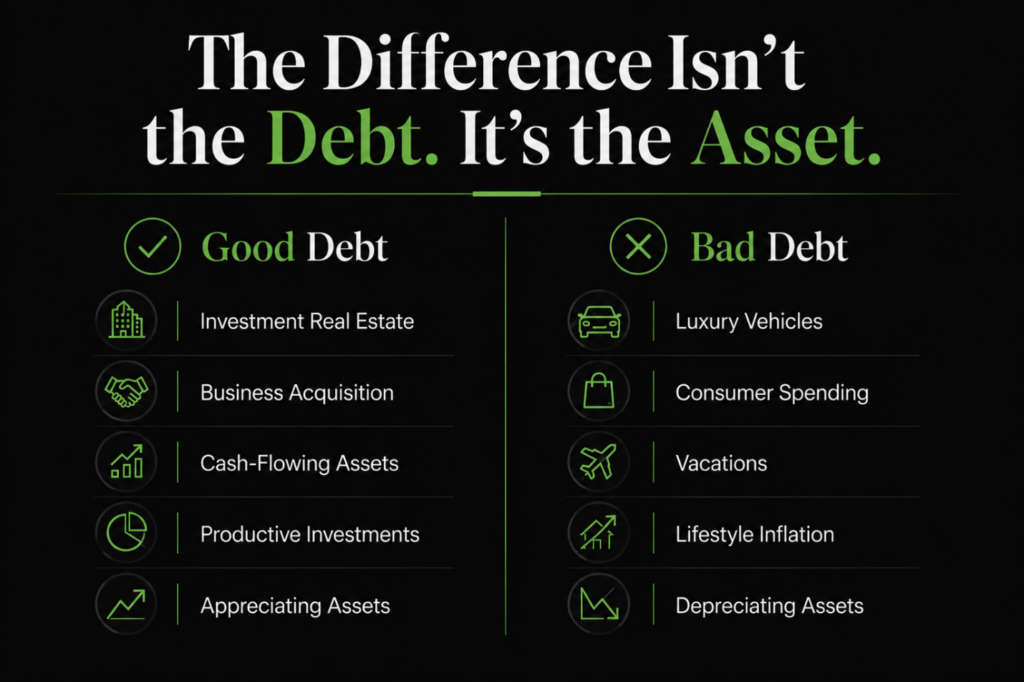

Rule #2: Make Sure the Asset Is Worth Leveraging

The second question is equally important.

What exactly are you borrowing money to buy?

Far too many people use debt to purchase things that immediately begin losing value. They finance expensive vehicles, support lifestyle inflation, or borrow money to buy things that don’t generate any future return. Then they wonder why debt feels like a burden.

That’s because it is.

Debt becomes much more dangerous when it’s attached to depreciating assets.

If you’re going to use leverage, it should generally be connected to something that has a reasonable chance of increasing in value over time. That could be investment real estate. It could be a business. It could be a business acquisition. It could be another productive asset that generates cash flow and has long-term growth potential.

The key is that you’re borrowing money to acquire something that creates value.

Not consumes it.

This is one of the reasons leverage is commonly used in real estate. If someone invests $200,000 and borrows another $400,000, they now control a $600,000 asset. If that asset appreciates by 10%, the gain is based on the entire $600,000 investment, not just the original cash contribution.

That’s powerful.

But it only works if the asset performs.

If the asset declines in value, leverage works against you just as quickly as it works for you when things go right. That’s why choosing the right asset matters so much.

A good financing structure cannot save a bad investment.

Rule #3: Ask What Happens If You’re Wrong

This may be the most important rule in the entire framework.

Before moving forward, I want to understand what happens if things don’t go according to plan.

Most investors spend almost all of their time evaluating upside. They think about how much money they can make. They think about the best-case scenario. They imagine everything working exactly the way they hope it will.

Very few people spend enough time evaluating the downside.

That’s a mistake.

Before investing, I want answers to questions like:

- What is the probability this investment succeeds?

- What is the probability it fails?

- Could additional capital be required later?

- If it fails completely, am I still financially secure?

- How would this affect my family?

- Would I still make this decision knowing the worst-case outcome?

Those questions aren’t exciting.

They’re necessary.

Recently, I spoke with a client who was considering pulling money out of his retirement account to purchase a business. Most of our conversation wasn’t about how much money he could make. It was about the risks involved. What if revenue didn’t materialize? What if the business underperformed? What if the assumptions proved wrong?

Those aren’t fun conversations.

They’re valuable conversations.

Because if you skip this step, you’re no longer investing.

You’re gambling.

Why Most People Blow Up Financially

Over the years, I’ve noticed something interesting. Most people don’t blow up financially because of one terrible investment. They blow up because they combine multiple mistakes together.

They put too much money into one deal.

They borrow too much.

They underestimate the downside.

They become overly confident.

Then when one thing goes wrong, everything starts unraveling at once.

That’s why risk management matters so much. You don’t need every investment to be a winner. You don’t need every decision to be perfect. You simply need to avoid the kind of mistakes that permanently damage your ability to keep investing.

That’s a very different mindset.

And in my experience, it’s one of the biggest differences between people who build long-term wealth and people who struggle to keep it.

My Final Thoughts

Debt should not automatically be viewed as good or bad.

It’s a tool.

Used recklessly, it can create significant financial damage. Used thoughtfully, it can accelerate wealth creation and create opportunities that otherwise wouldn’t exist. The key is having a framework that helps you control the risk before you ever borrow the money.

For us, that framework starts with limiting exposure, choosing the right assets, and stress testing every opportunity before moving forward. We’re not trying to predict the future. We’re trying to make sure that if the future doesn’t unfold the way we expect, we’re still standing.

Because the goal isn’t to eliminate risk.

The goal is to survive it.

When used properly, debt can be a powerful tool for building wealth. But the people who use it successfully understand something that many investors overlook: debt isn’t the real danger.

Overexposure is.

And that’s why most people don’t have a debt problem.

They have a risk management problem.