If you have spent years building a company in Westlake, your business is almost certainly your largest and most complex asset. It is also the one most likely to create problems for your family if you have not put a plan around it. Between the Solana office campus, Circle T

Building a successful business is one of the most effective ways to create wealth, but for many entrepreneurs in Colleyville, the business itself becomes both their largest asset and their biggest financial risk. While growing revenue and increasing profitability are essential, long-term wealth creation requires a broader strategy that extends

If you live in Southlake, you already know that building and protecting wealth here looks a little different than it does in most communities. It is about making confident decisions around retirement, taxes, college funding, business ownership, estate planning, and preserving wealth across generations. As net worth increases and financial

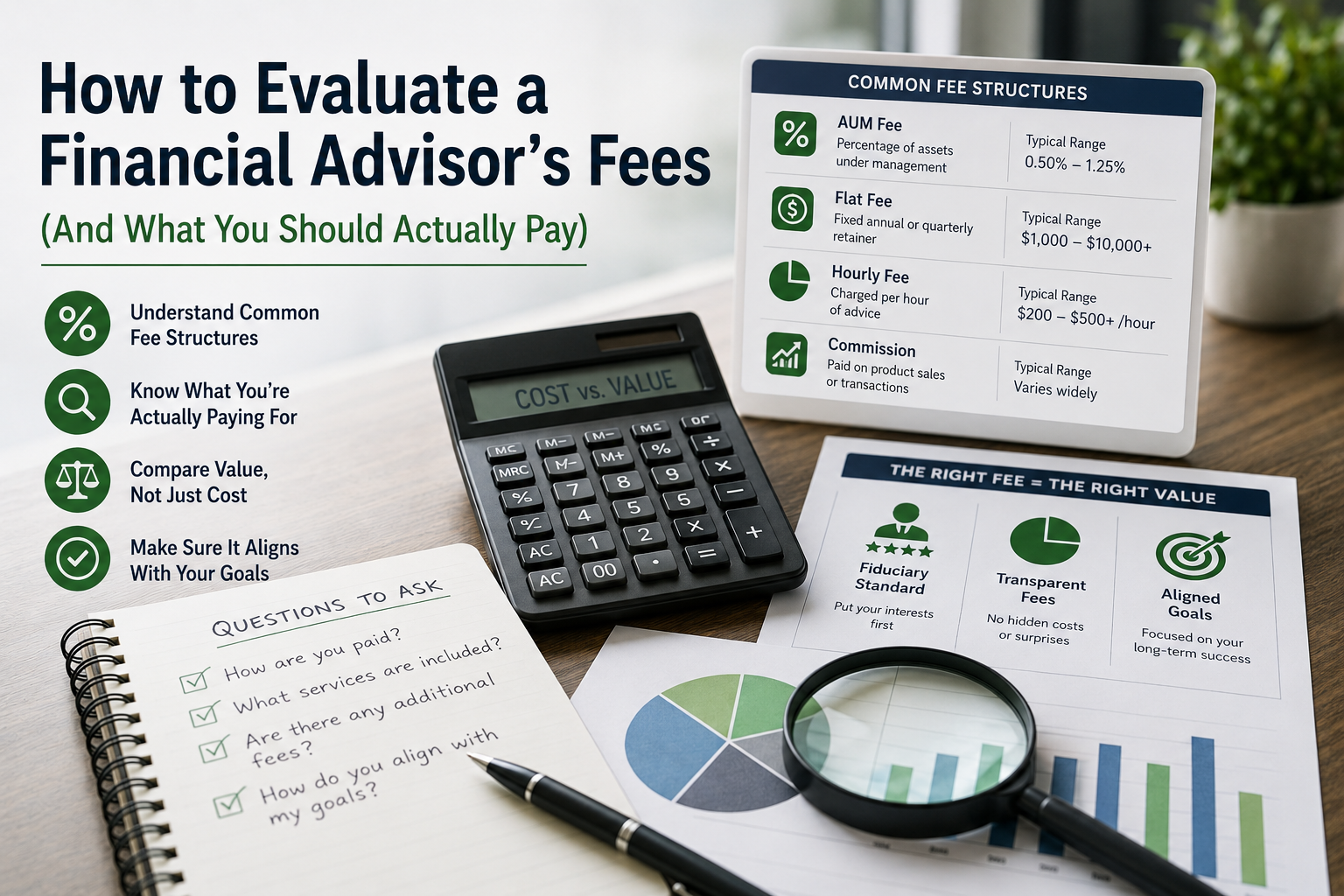

(And What You Should Actually Pay) Good financial advice earns its keep. Planning, tax strategy, investment discipline, a steady hand when the market throws a tantrum, all of it adds real value. How an advisor charges for that work, and how much, shapes everything else about the relationship. The Four

Memorial Day means different things to different people. For many families, it marks the beginning of summer, time spent outside, cookouts, baseball games, and long weekends together. But underneath all of that is something far more important. Memorial Day exists to remember the men and women who gave their lives

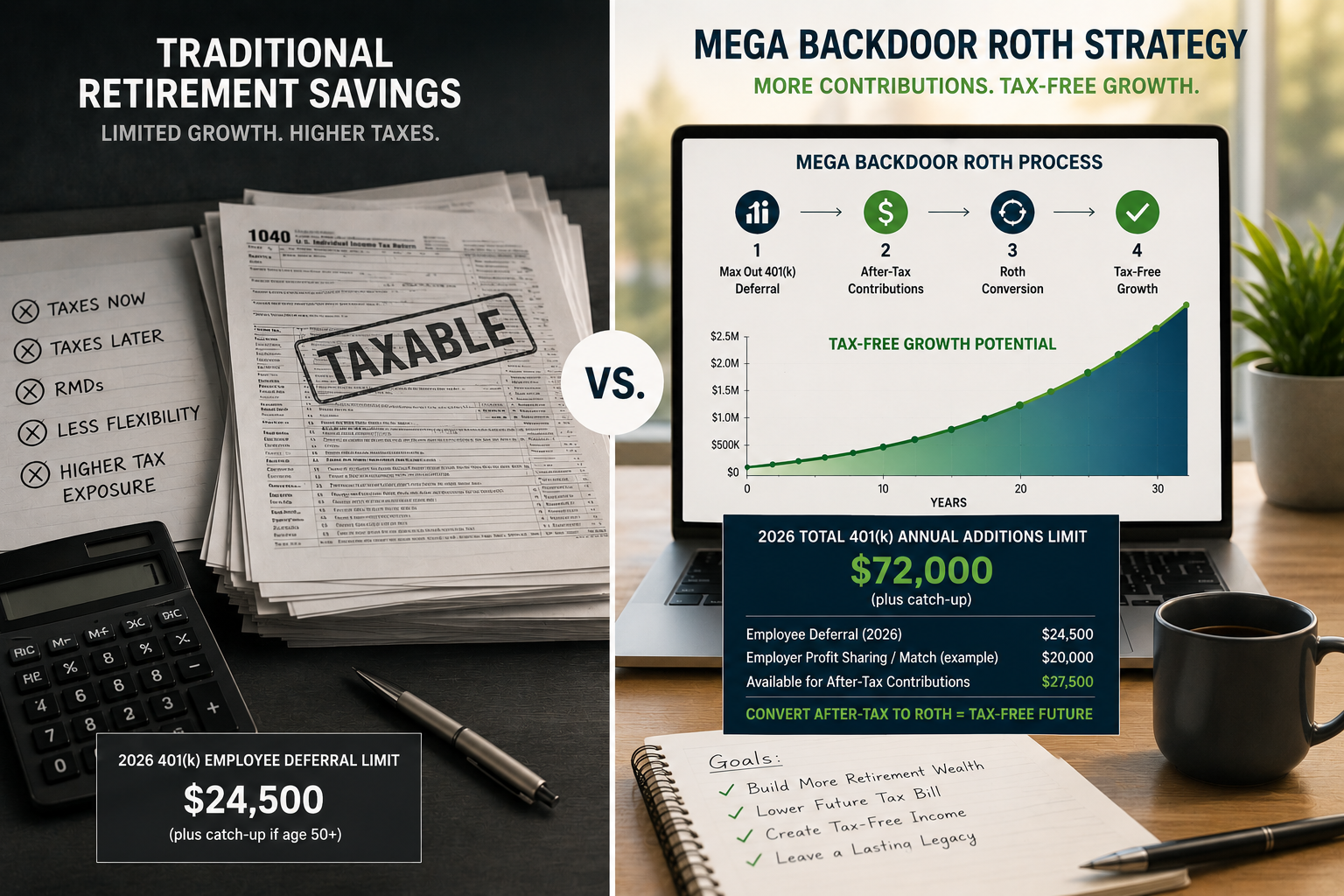

If you are a high-income earner or business owner, there’s a decent chance you’ve looked at your retirement plan and thought: “Wait… that’s it?” You max out your 401(k), maybe you do some additional investing in a brokerage account, and then you realize the IRS limits can feel restrictive pretty

Running a business in Grapevine brings opportunity and complexity. Smart tax planning helps you keep more of what you earn, manage cash flow with confidence, and make better long term decisions. The key is to stay proactive, not reactive. Below is quick reference table and a practical guide to help

If you live in Coppell and have kids in Coppell ISD, you’ve probably had this thought at some point: how are we actually going to pay for college? It’s a fair question. Costs keep rising, the rules change, and everyone seems to have a different opinion on what the “right”

So, the offer came through, the boxes are taped up, and somewhere between the goodbyes and the moving-truck deposit, you’re now a Trophy Club resident. Congratulations — you’ve landed in one of the most desirable suburbs in North Texas, with top-tier schools, a championship golf course in your backyard, and

If you live in Keller, there’s a good chance both you and your spouse are working. That’s just the reality for most families in this area. Strong job opportunities, great schools, and a high quality of life come with a higher cost of living, and two incomes are often what