If you work at a tech company, a startup, or any growth-stage business, equity is probably a meaningful piece of your total comp. And the odds are good that nobody walked you through how the taxes actually work. Most HR departments hand over a grant agreement and move on.

That gap is expensive. People receive life-changing equity packages and give a significant portion back to the IRS in ways that were entirely avoidable. The three main types, RSUs, ISOs, and NQSOs, each have different tax treatment, different planning opportunities, and different ways to get caught off guard. Here is what actually matters.

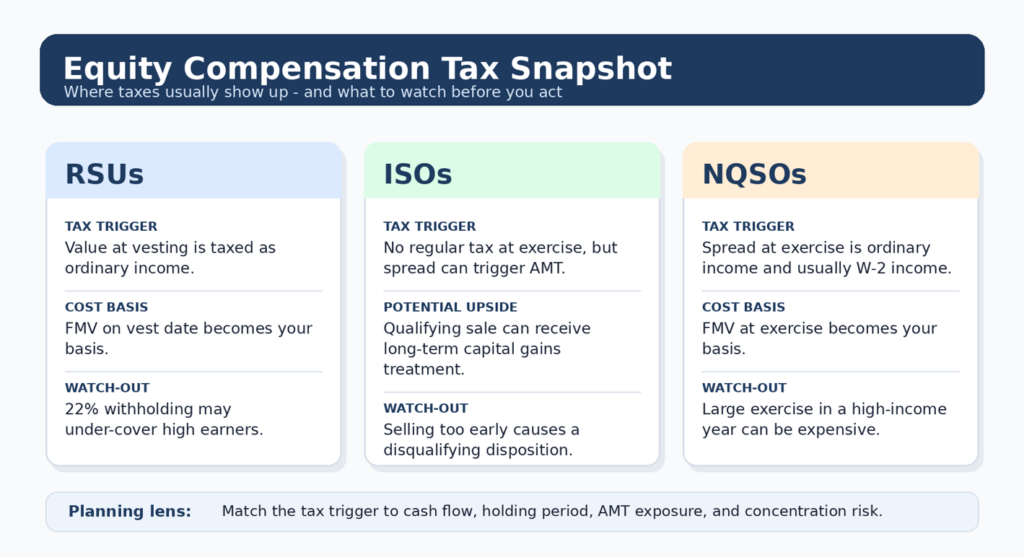

Equity compensation tax snapshot: RSUs, ISOs, and NQSOs each create different tax triggers and planning risks.

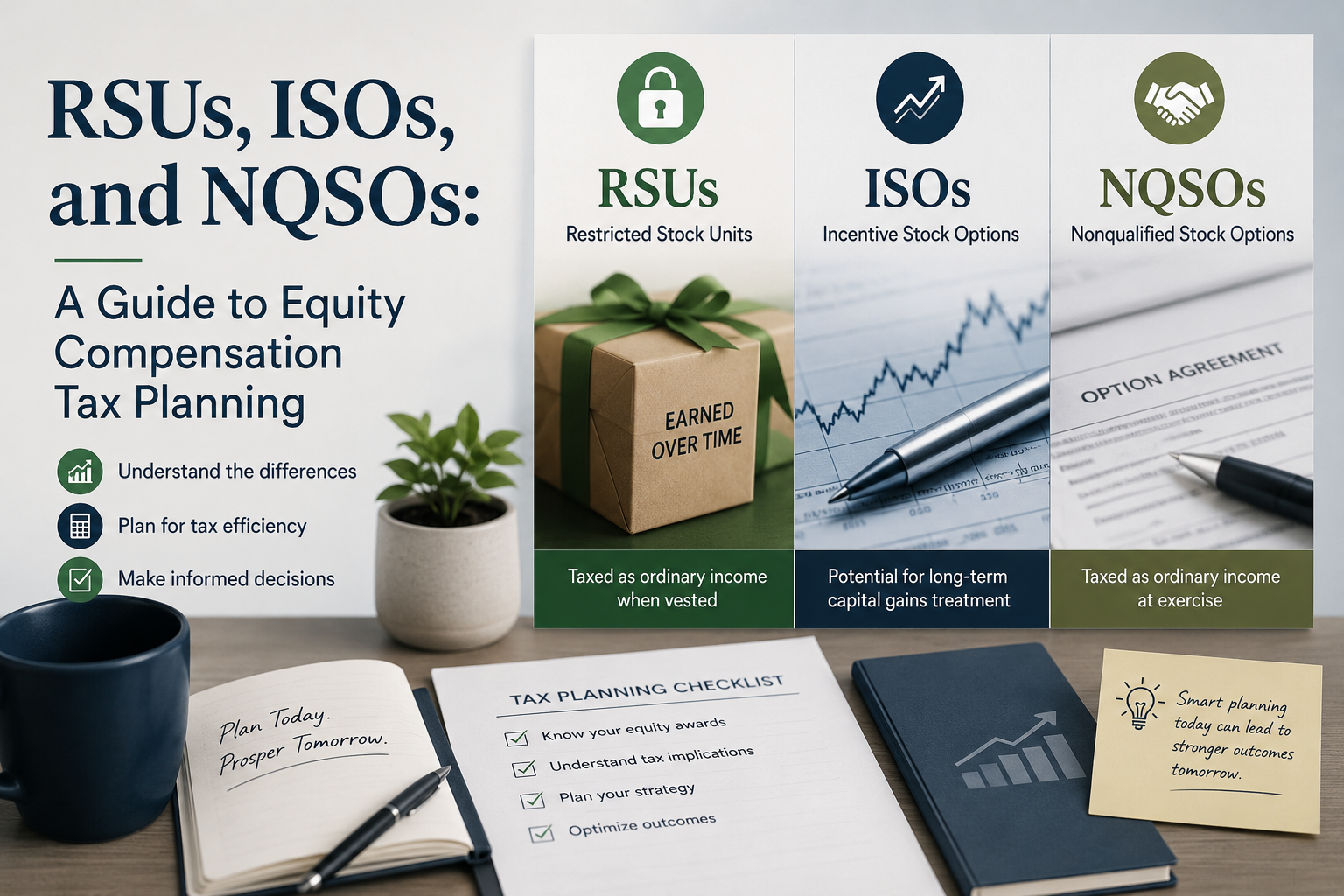

RSUs: The Straightforward One (Until It Isn’t)

Restricted Stock Units are the most common form of equity compensation right now, and the tax treatment seems simple on the surface: when your shares vest, you pay ordinary income tax on their value that day. No option exercise, no strike price to think about, no AMT exposure.

Your company will typically withhold shares automatically to cover the tax, usually at the 22% federal supplemental withholding rate. Here is where people get blindsided: if you are in the 32%, 35%, or 37% bracket, that 22% is not enough. There is a gap, and the IRS will collect it in April. Missing estimated payments on a large vesting event can mean a surprise bill plus underpayment penalties.

The other thing RSU holders miss is what happens after vesting. Once shares vest, you own stock with a cost basis equal to the fair market value on vest day, the same amount you paid income tax on. From that point, any appreciation is a capital gain. Hold for over a year and you are in long-term territory. Sell the day they vest and it is short-term, taxed as ordinary income.

Something worth knowing: if you believe in the company’s trajectory, holding vested shares at least 12 months before selling means any appreciation from the vest price forward is taxed at long-term capital gains rates rather than ordinary income rates. On larger positions, that difference adds up.

ISOs: The Tax-Advantaged Option With Hidden Landmines

Incentive Stock Options are the one form of equity compensation Congress designed to be favorable. Exercise your options, hold the shares long enough, and your gains get taxed at long-term capital gains rates rather than ordinary income. That is a meaningful difference, potentially 20 or more percentage points depending on your bracket.

To qualify, you need to hold shares for at least two years from the grant date and one year from the exercise date. Meet both thresholds and the entire spread from strike price to sale price is long-term capital gain.

Two things derail this in practice. The first is the AMT problem. When you exercise ISOs, you do not owe regular income tax at exercise. But the spread between your strike price and the fair market value at exercise is an AMT preference item. If that number is large enough, it can trigger the Alternative Minimum Tax, a parallel tax system that runs on its own rate schedule and ignores most of your deductions.

This matters because someone could exercise a large ISO block when the stock is high, hold the shares, watch the stock decline significantly, and still owe AMT on paper gains that no longer exist. This is not hypothetical. It happened to a large number of tech employees after the dot-com crash and in other down cycles since.

The second issue is the disqualifying disposition. If you sell before meeting both holding period requirements, the IRS taxes the spread at exercise as ordinary income, the same treatment as NQSOs. The preferential rate disappears entirely, and it can happen accidentally if you lose track of when you exercised.

Something worth knowing: exercising ISOs earlier in the year, or in lower-income years, can reduce AMT exposure. Some people exercise in January specifically to maximize the holding period and control which tax year absorbs the AMT hit. Modeling AMT exposure before exercising anything significant is worth doing with a tax professional.

NQSOs: No Special Treatment, but Simpler

Non-Qualified Stock Options do not get favorable ISO treatment, but they are also cleaner to think about and do not carry AMT risk.

When you exercise an NQSO, the spread between your strike price and the fair market value at exercise is ordinary income, taxed like your salary and subject to income tax and payroll taxes. Your company withholds, and it shows up on your W-2. From that point, your cost basis is the fair market value at exercise, and any further appreciation is a capital gain.

The flexibility with NQSOs is that you can exercise and immediately sell, often called a cashless exercise, without worrying about holding periods or disqualifying dispositions. The tax consequence is ordinary income on the spread.

Timing matters here. Exercising in a year when your income is lower, a career transition, a leave of absence, or a high-deduction year, means recognizing that ordinary income at a lower marginal rate. Stacking a large NQSO exercise on top of an already high-income year is the most expensive version of this decision.

A Few Things That Cut Across All Three

Concentration risk. Equity compensation often results in a significant position in a single stock, your employer. The tension between managing that risk and avoiding a tax event is real, but taxes should not be the only variable. Paying taxes on gains means you made money. A diversified portfolio that is slightly less tax-efficient is usually better than a concentrated position in a company whose stock turns.

Capital losses. If you have underwater positions, selling them generates losses that offset gains dollar for dollar. Beyond that, up to $3,000 per year can offset ordinary income, with the remainder carried forward indefinitely.

State taxes. Everything above is federal. Your state may have its own rules, and some states do not conform to federal AMT treatment. If you have moved states between grant and exercise or sale, you may have multi-state obligations worth reviewing with a tax professional.

The 83(b) election. If you receive restricted stock (actual shares that vest over time, not RSUs) or exercise options early when the spread is small, you can elect to pay tax now on the current value rather than at vesting. Miss the 30-day filing window and the option is gone permanently.

The Bottom Line

Equity compensation is genuinely complicated, and the stakes are high enough that the details matter. RSUs are straightforward but the withholding gap catches people off guard. ISOs offer real tax advantages but the AMT risk is serious and requires advance planning. NQSOs are taxed as ordinary income at exercise but give you flexibility and predictability.

What most people skip is thinking through these decisions before acting. A vesting notification comes in, shares appear in the account, and the choice is either sell immediately or hold indefinitely, without running the numbers on what either actually costs. Thinking through exercise timing, holding periods, and income scenarios in advance is where the real value is.