For many successful families in Southlake, building wealth has taken years of hard work, disciplined investing, and thoughtful financial decisions. However, accumulating wealth is only part of the equation. Preserving it and ensuring it passes to future generations according to your wishes requires a well-designed estate plan. Estate planning is

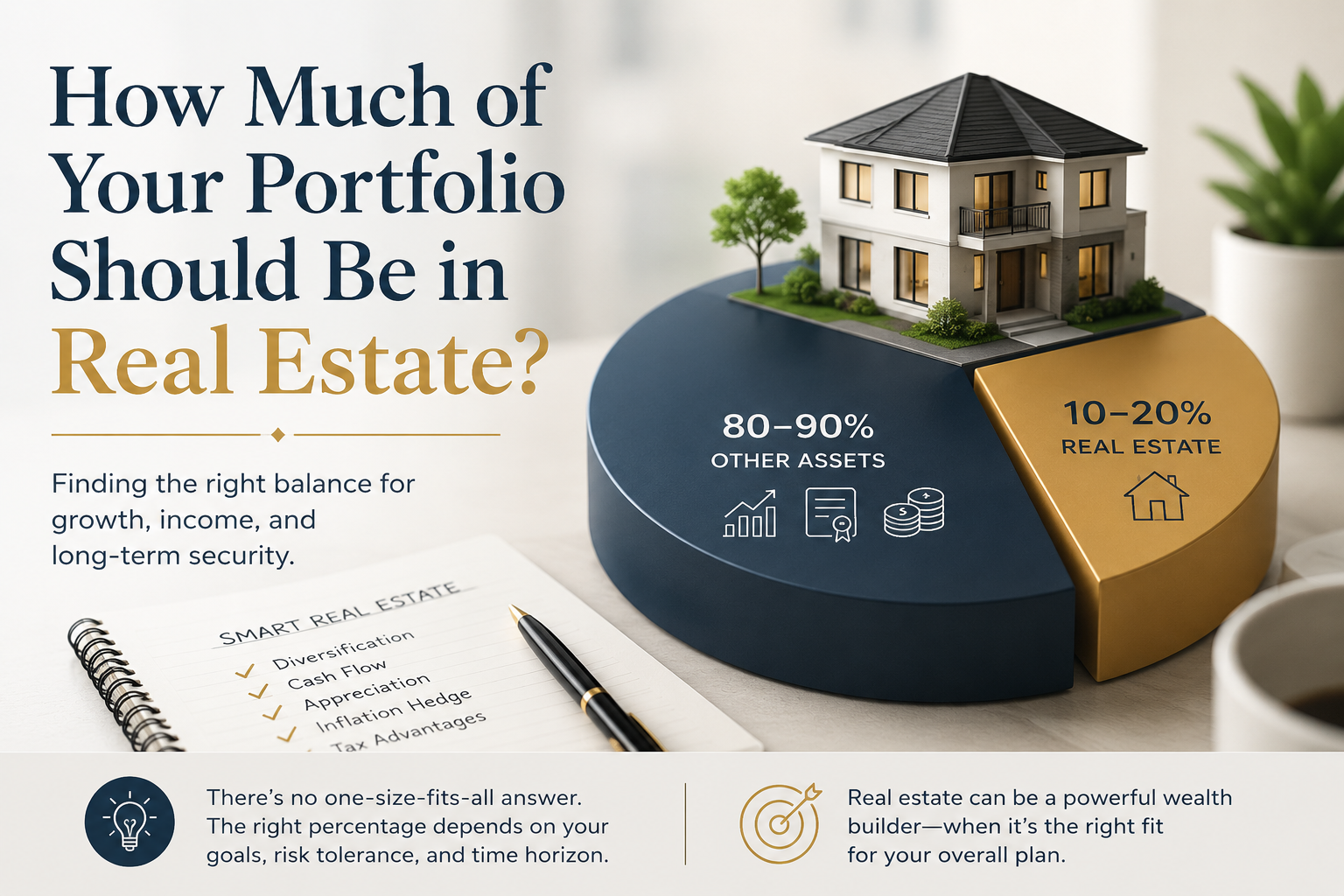

Finding the Right Balance for Your Goals and Risk Tolerance Real estate holds a natural appeal for many investors. It feels tangible, it can generate income, and it often behaves differently from stocks and bonds. Yet a common question follows close behind that appeal. How much of your portfolio actually

Selling a successful business can create life-changing wealth. It can also create one of the largest tax bills a business owner will ever face. Imagine selling a company and recognizing $15 million of capital gain. At the highest federal long-term capital gains rate of 20%, plus the potential 3.8% net

One of the great appeals of doing business in Texas is what the state doesn’t charge: there’s no personal income tax. But business owners who assume that means no state-level tax at all are often surprised by a letter from the Comptroller. Texas funds a meaningful share of its budget

Business owners often hear the same financial advice: spend less, save more, buy a house, follow your passion, and eventually sell the business to fund retirement. Some of that advice helps. Much of it becomes harmful without context. Building wealth does not require guilt every time you spend money, homeownership

DOWNLOAD THE PDF The second quarter of 2026 looked quite different from the first. After markets struggled in March, stocks bounced back as investors once again focused on artificial intelligence, strong corporate profits and the continued strength of the U.S. economy. Even with the war in Iran, higher oil prices

The second quarter of 2026 delivered strong gains across nearly every major market. Emerging markets led the way, surging 24.05%, followed by the U.S. stock market at 15.44% and Global Real Estate at 10.76%. International Developed markets also posted a solid 10.22%. Fixed income markets contributed positive returns as well,

Moving to Texas can create meaningful financial opportunities, especially for families and business owners relocating from states with high personal income taxes. Texas does not impose an individual state income tax, which can significantly improve cash flow for high earners, retirees, entrepreneurs, and investors. However, moving to Texas does not

Choosing a financial advisor is a major decision and shouldn’t be taken lightly. The process involves more than finding someone who has the best credentials, highest investment performance, or lowest fees. It’s about finding someone who understands your life, your goals, and the financial landscape you navigate every day. While

Life insurance is one of the most common tools for protecting your family’s financial future. But many people are surprised to learn that the death benefit they worked so hard to secure can be reduced by estate taxes (or tangled up in probate) if the policy isn’t structured carefully. An