We are happy with the returns your portfolios have received so far this year. Global diversification helped smooth out the tariff bumps. Our low-cost investments are performing as expected and have added value. Given the recent run up in AI Optimism, we think now is a great time to reevaluate your investment allocation, giving yourself the opportunity to review your overall risk and run the “fire drill”. Below we dive deeper into today’s valuations and concentration in major US Indexes. We find similarities with the late 1990s and try to provide a few comparisons.

My friend, ChatGPT, pulled some stats to help quantify today’s optimism in prices. It also pulled some key points from a few of the top investment managers’ recent letters to shareholders, which mostly reiterate the same point. While prices are high in some areas of the market, they are low in others. Markets are complex systems made up of buyers and sellers best guess of the future, and, for that reason, prices are mostly right, and we may learn that indeed today’s valuations may in fact be justified; markets can always go higher. I want our clients to be asking themselves: “When is the right time to make adjustments to maximize my plan’s success and build the highest level of confidence?”.

On a separate note, I wanted to brag about our experienced team. Crystal just celebrated her 9th anniversary with us, and I’m sure you see Stephen all over the internet. We are very proud of the advisory team that is helping you reach your financial goals. They will be available to help you think through this risk/return decision. I also want to announce that because of great clients like you, our assets just crossed over $500 Million in assets, so thank you for your continued trust and support.

In a few days you will be receiving a very short anonymous survey. We would love it if you could take the time to give us some quick feedback. It has been a pleasure to serve you, your family, your employees, and those you care about. If we can ever be of assistance, please don’t hesitate to reach out.

SECTION I – Q3 2025 Market Review – Global & U.S. Performance Highlights

SECTION II – Mike’s Advisor Commentary: Market Lessons & Investor Questions

SECTION III – Tax Corner: Donor-Advised Fund Strategies for 2025 Giving

SECTION IV – Inside Mills Wealth: Team Updates & Milestones

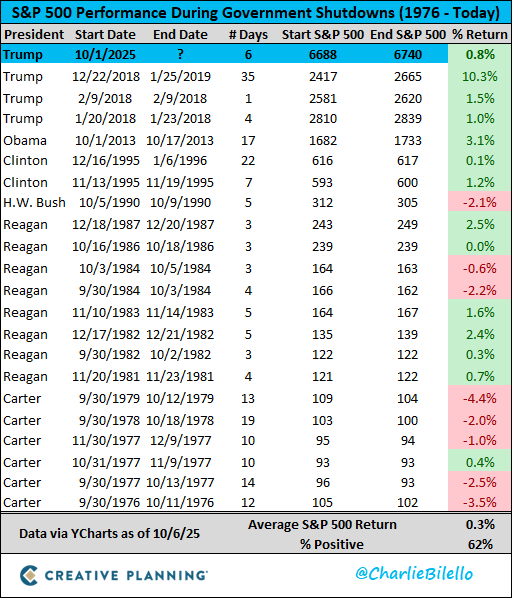

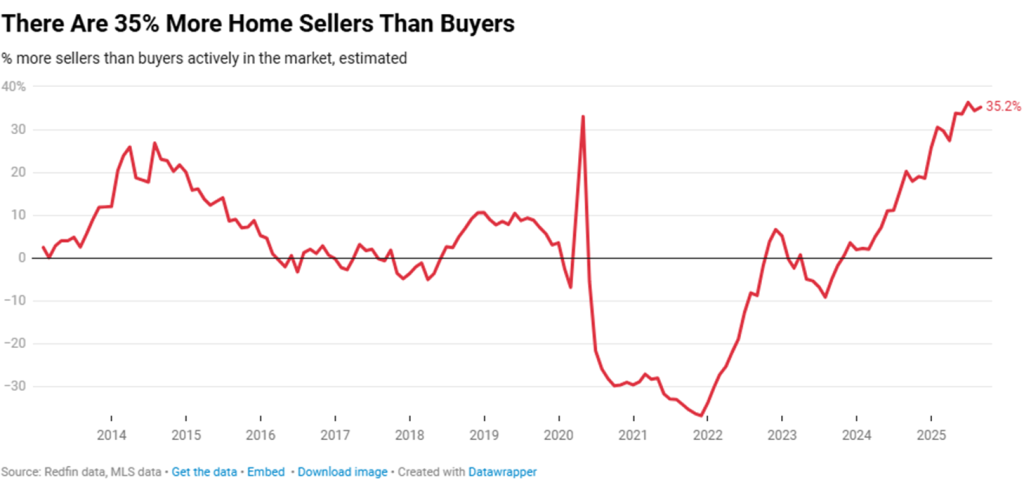

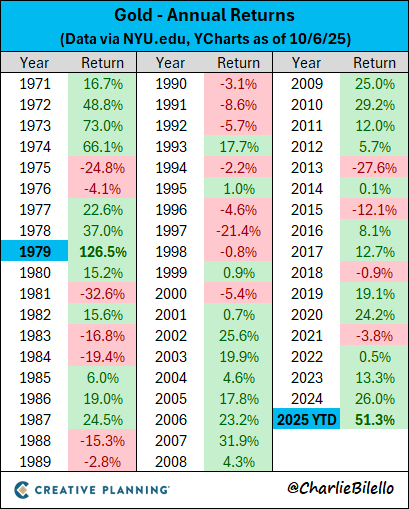

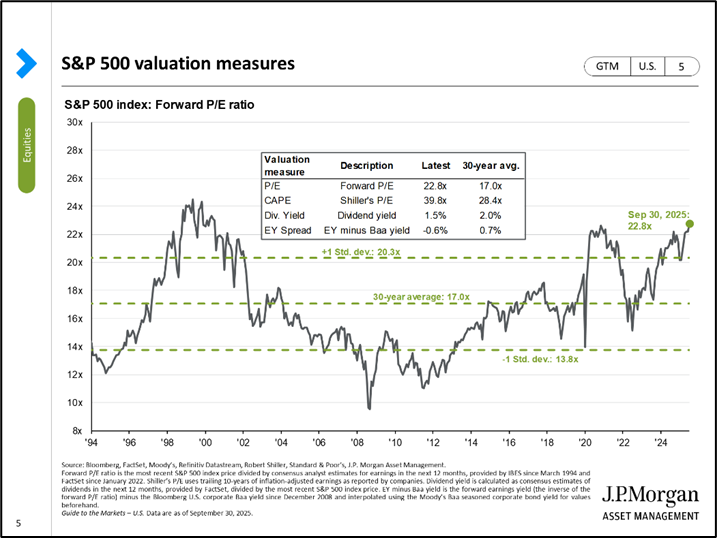

SECTION V – Market Charts & Visual Highlights from Q3 2025

Q3 2025 Market Review – Global & U.S. Performance Highlights

The 3rd quarter of 2025 delivered strong performance across global stock markets, with Emerging Market Stocks leading the gains at 10.64%, followed by U.S. Stocks at 8.18%, International Developed Stocks at 5.33%, Global Real Estate at 4.22%, the U.S. Bond Market at 2.03%, and the Global Bond Market at 0.49%. Encouragingly, all these markets—except the U.S. Bond Market and Global Real Estate—have posted positive returns over the past 1-, 5-, and 10-year periods., CLICK HERE.

Mike’s Advisor Commentary: Market Lessons & Investor Questions

“The best investment strategy is one you can stick with.”

If you regularly read my quarterly letters, you will notice I try to repeat the same information over and over again, but in slightly different ways. Investment success is captured often by those that diversify, keep cost low, and stick to their strategy. Warren Buffet and his partner, Charlie Munger, both shared that “Investing is simple, but not easy.” This paradox highlights that while the underlying logic of sound investing is straightforward, human behavior and emotions make it challenging to execute successfully over long periods of time. I think FOMO (the Fear of Missing Out) is one of the recurring reasons throughout history that leads human beings to make unwise investment decisions, which can then lead to bubbles. Behavioral finance has documented that we experience the pain of loss twice as much as we relish in success. The emotions of loss can be felt both when markets rise and fall.

In the internet stock boom of the late 1990s, the technology stock bubble literally sucked the money out of other profitable investments that didn’t seem as fashionable at the time. “Old-timers” warned of the rampant speculation and of the high valuations on low quality stocks without earnings, but their fruitless warnings lost out to the call of “easy money.” Investing in unprofitable tech IPOs was just too hard to resist as money poured into this hot area. “Between 1995 and its peak in March 2000, investments in the NASDAQ composite stock market index rose by 600%, only to fall 78% from its peak by October 2002, giving up all its gains during the bubble.”

Source: https://en.wikipedia.org/wiki/Dot-com_bubble

For a short recap of what the Tech Boom & Bust was really like read this Wikipedia page https://en.wikipedia.org/wiki/Dot-com_bubble

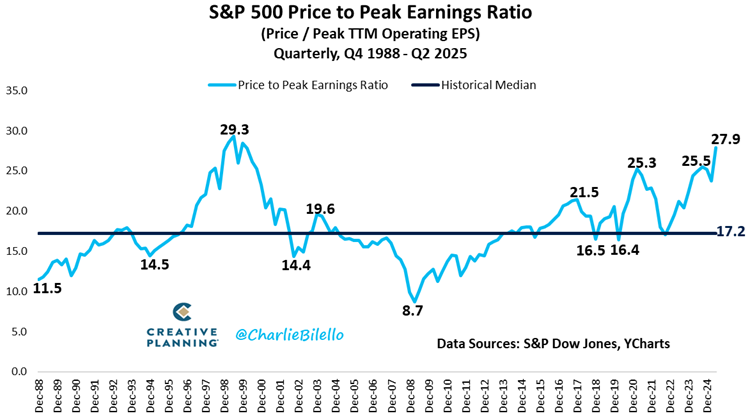

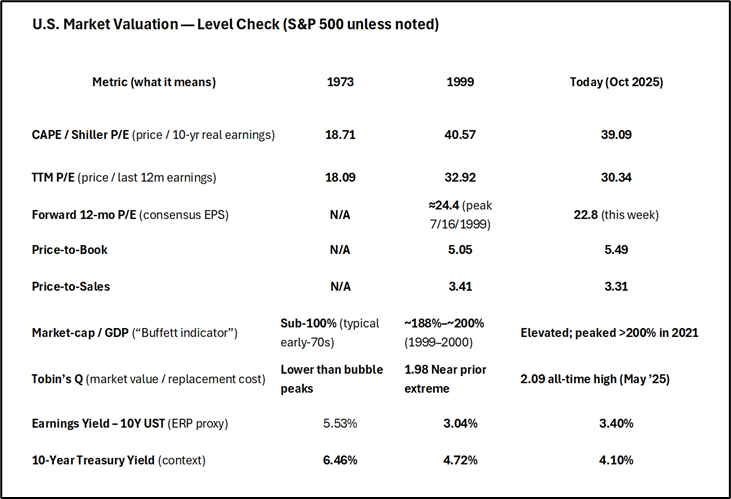

Today, we see similar valuations to the late 1990s in the S&P500 (see chart below), and similar speculation in a few areas of the market, namely AI and crypto. However, unlike the Internet bubble, the bulk of the largest companies in the S&P500 have tremendous earnings and are some of the best businesses ever built. They have redirected their profits toward buying Nvidia chips and datacenter construction attempting to win in the AI race. What I think is interesting is the sheer size of how much money these companies are investing.

“Microsoft, Google, Amazon, and Meta are the main players investing at staggering levels to build and upgrade data centers that support the exponential demand for AI computing power, with those four companies alone forecasting a record $364 billion of capital investment in 2025. Combined, the so-called Magnificent Seven tech giants spent more than $100 billion on data center projects in just the past three months, as calculated by the Wall Street Journal’s Christopher Mims.

All this spending has to have an impact on the economy. Analyst estimates from Renaissance Macro Research indicate that so far in 2025, the dollar value contributed to GDP growth by AI data center expenditure surpassed the total impact from all U.S. consumer spending—the first time this has ever occurred.

Source: https://finance.yahoo.com/news/spending-ai-data-centers-massive-150110727.html

It is often said that history rhymes, but it never unfolds the exact same. The trillion-dollar question is will this shift in strategy eventually result in future profits that justify today’s higher valuations, or will these dominant companies all end up furiously competing in a red ocean, with a “winner take all” market that eventually leads to the destruction of trillions of dollars of capital and forces a falling stock market?

Client Question: How should your investment strategy change with rising valuations and lower expected future returns? Do you just continue to focus on the long-term, stay diversified and ride the wave; do you take some profits and play it safe; or do a little of both?

Our Advisors are ready to think through this conversation formally via a meeting or informally on the phone, by Zoom, or in person.

I’m encouraging every investor to run a portfolio “fire drill”. Be confident in your plan whether markets continue to rise or begin to fall. If the music stopped tomorrow and valuations collapsed back toward their average, would you feel comfortable waiting 3-10 years for your offensive investments to rebound? Do you feel like your plan has the proper amount of defense to fund your future expenses plus a little extra to buy equities if they were to go on sale? I’m a huge fan of rebalancing and taking profits while markets are high (even if markets go higher). In most market selloffs, stocks typically decline quickly because once fear sets in, selling is off the table. (This past week was a good example of this as fears of additional China tariffs spooked markets).

Emotionally, once markets decline, I think it is easier to ride through the valleys with a mindset that views market declines as “sales” where investors are opportunistic buyers, not forced sellers. With all this “fire drill” talk I may sound negative, but between the AI spend, investor optimism, Trump rate cuts, and the effects from the One Big Beautiful Bill, I think it is also wise to consider how you would feel if markets continued to rise. While markets appear expensive today compared to historical levels, they looked that way in 1997 as well, yet 1998 & 1999 were some of the strongest years on record as markets rose in a feeding frenzy of internet optimism.

Structural Points to Remember about today’s Index Funds: Market Size Weighted Indexes (like the S&P500 & NASDAQ) are exhibiting the highest concentration in their history, basically making it a growth fund, the instead of broadly diversified large cap index that made it popular. Half of the index is in just a few large positions. “Over the period 1880–2024, the top 10 stocks’ share of the index has fluctuated, typically in the mid-20s (percent) for much of the 20th century but rising toward 38% in recent years.” (Source Visual Capitalist) 1929, 1973, 2000, and 2024 were all years of high concentration in just a few names. Three of these periods preceded some of the largest declines of the stock market on record. I’m not trying to say this is the top, but I am firmly stating that everyone needs to reassess their risk, time horizon, targeted allocation, and the strategies they are comfortable owning for the next decade.

I believe the future returns for the S&P 500 index will likely offer investors lower returns than can be realized in other market areas or in areas that have less exposure to the largest US companies. Today’s optimism has pulled future returns forward. Investors are paying more than ever for each dollar of revenue the S&P 500’s members produce. At some point, increased competition with each other and the switch to other capital-intensive strategies are likely to weigh on their future multiples and returns. If the largest companies decline, even a little, the size weighted indexes will struggle to be positive because of the sheer size of the top 20 companies relative to the rest of the index. We favor other, more diversified options that own assets outside of the largest US companies.

The Big Idea behind these metrics and the portfolio manager summaries:

All these metrics are just different lenses illustrating the same picture: How expensive are U.S. stocks compared to what companies actually earn or own — and how does that compare to history?

When most of these gauges sit near historical highs, it means expectations for future profits are already baked into prices. That doesn’t predict an immediate drop, but it does mean the margin for error is thin, and future returns usually end up well below average. We think this means investors should reassess their portfolio allocation and risk parameters, as well as err a little more toward the cautious side of their playbook.

It doesn’t yet feel like 1999. Markets can get much crazier than they “feel” right now. The AI buildout and reshoring of supply chains could result in 3% GDP with favorable interest rates. If housing gets going markets could grow much farther from here. This is one reason we are rarely all In or all out.

The major point I am trying to get across is “are you comfortable with your investing approach?” If markets rise quickly from here (and markets rise 2-3x more than they fall) how will you react then? How will you deal with FOMO?

I would like to end where I started, the best portfolio is one you can stick with.

Quarterly commentaries (Q3 2025) from some of the top active management companies I thought you might find these useful.

- Ray Dalio (Bridgewater Associates): The founder has recently expressed concerns about rising U.S. debt and political division, warning of a “debt bomb” and a growing “civil war” of irreconcilable differences. He compared today’s economic landscape to the 1970s and advised investors to hedge against risk by holding gold.

- Ken Griffin (Citadel): Griffin cautioned that the U.S. economy is on a “sugar high” created by fiscal and monetary policies better suited for a recession. He noted the rally in gold—which has surged over 50% year-to-date—as a sign that investors are concerned about U.S. sovereign risk and inflation.

- David Einhorn (Greenlight Capital): Einhorn raised concerns about the massive capital expenditures pouring into artificial intelligence (AI). He questioned whether this spending—totaling hundreds of billions, or potentially a trillion dollars—will lead to capital destruction for the companies involved, even if the technology itself proves transformative.

- Bill Ackman (Pershing Square): In Q3 2025, Pershing Square made strategic portfolio adjustments, including a new stake in Amazon. In the August 2025 H1 letter, Ackman noted that market volatility from tariffs and geopolitical issues created opportunities to add to holdings.

- Ariel Investments: In their Q3 2025 letter, managers discussed the “staggering differential” in returns between large and small companies and argued that negative sentiment toward small- and mid-cap stocks presents a rare opportunity for long-term investors.

- Polen Capital: The Polen Focus Growth Portfolio had an underwhelming Q3 2025 compared to its benchmark, lagging due to a “concentrated ‘risk-on’ environment” that favored AI-related stocks. The commentary emphasized that the fund would stick to its quality-driven investment approach.

- ClearBridge Investments: The Q3 2025 commentary from ClearBridge highlighted that equities historically perform well after the Fed begins a soft-landing rate-cut cycle. Managers also suggested a soft landing is possible given earnings-per-share (EPS) growth expectations.

Please don’t hesitate to call or text or email with any questions you might have.

All the Best,

–Mike

Tax Corner: Donor-Advised Fund Strategies for 2025 Giving

Using your Donor Advised Fund in 2025 may be one of the best tax decisions you make in the next decade.

Starting in 2026, high earners face two hidden hurdles around charitable deductions.

1️⃣ The first 0.5% of AGI donated each year isn’t deductible.

2️⃣ Deductions are capped at the 35% rate

(even if you’re in the 37% bracket).

Now Let’s put some numbers to this:

Income: $800,000 AGI

Tax Rate: 37%

Giving: $15,000 per year

Today (2025 rules):

– Deduct $15,000

– Save $5,550 in taxes

2026 & Beyond (new rules):

– First $4,000 doesn’t count

– Remaining $11,000 only saves 35%

– Tax savings: $3,850

👉 That’s a $1,700 annual loss.

👉 Over 10 years? $17,000.

But there’s a fix; instead of giving $15k each year under the new “haircut” rules, frontload 10 years of charitable donations into a Donor Advised Fund (DAF) all in 2025 and get the full deduction!

✅ Contribute $150k now

✅ Deduct at the full 37% rate

✅ Still give $15k/year from the DAF in future years

Same charities funded.

But $17,000 of tax savings is preserved.

For high earners, 2025 may be the last chance to lock in today’s full deduction before the haircut kicks in.

Inside Mills Wealth: Team Updates & Milestones

Helen Esomo passed her hours requirement and is a fully fledged Certified Financial Planner™ Professional. And for those who don’t know, getting the CFP® is no easy task. It requires passing 6 individual tests, passing a capstone course, and then passing a 6-hour test that combines the 6 previous tests in one. Then on top of that you need between 4,000-6,000 hours in the profession to be able to call yourself a CFP®.

Helen passed the exam in 2024 but was able to get all the hours required in 2025. We are proud of her, and proud to have 5 advisors who hold the CFP.

Mike Mills CFP® CLU CEPA®

Stephen Nelson CFP® AIF® CEPA®

Matthew Brown CFP®

Emily Lopez CPA CFP®

Helen Esomo CFP® MBA

Here is a press release that was posted in the USA Today about this exciting news around the MWA office.

Market Charts & Visual Highlights from Q3 2025