We received a really good question that I wanted to share with all of our clients and those who follow us online.

“An old and trusted indicator in the bond market is warning about possible trouble ahead in the economy and the stock market. What should I do?”

In the following New York Times article, a market prognosticator addressed a topic many investors worry about — the possibility of a stock market decline. The fact is that we should expect a decline every few years. We have had a long spell without a decline, so it is eventually bound to occur. What will you do when it happens?

We frequently receive this question: Should we just sell everything, avoid the pain, and wait for the decline in cash, or should we stay invested and execute the plan?

I think this is a question many investors hear from that little voice in the back of their heads. I hope every investor will contemplate this question and resolve to create a desired plan now while everything is calm and before the next stock correction arrives.

What is your bear market contingency plan?

Quick story: When I was younger (and thought I was smarter), we followed the indicator mentioned in the above article. However, now that I’m older, more experienced, and filled with gray hairs (each caused by a pain, mistake, or worry), I feel that predicting market declines is unreliable. More money is lost preparing for bear markets that do not arrive than is lost in the bear markets themselves.

A much wiser approach is to set aside a little portfolio defense that can be added to markets should they decline.

I think Warren Buffett’s approach to long-term buy and hold investing makes the most sense. As the adage goes, “Investing is like a bar of soap; the more you handle it, the smaller it gets.” Markets rise more than they fall, and investors can make thousands of percent return to the upside and only about fifty percent to the downside. I advise most savers that trying to correctly time a market decline is dangerous, as you need to be right twice to profit (when to get out and when to get back in). A strategy that relies on market timing for profit is a classic bad bet.

The strategy we favor, which has a long history of success, is simple to execute, but it involves tolerating some short-term pain while maintaining a long-term view. When tempted to accept the strategy of prognosticators who call for imminent market declines, remember that these same blowhards were screaming about the market going lower when it had fallen to less than 7,000 on the DOW (now it’s over 21,000). At MWA, we think the most prudent solution is to set aside enough defense in fixed income and emergency funds so that when the correction happens (and it will happen), you have enough reserves available to confidently redeploy some of them. These reserves are typically stored in fixed income and can be shifted into the equity markets while prices are depressed. This ensures a decent price on funds deployed after the correction. This low-risk solution helps investors buy low.

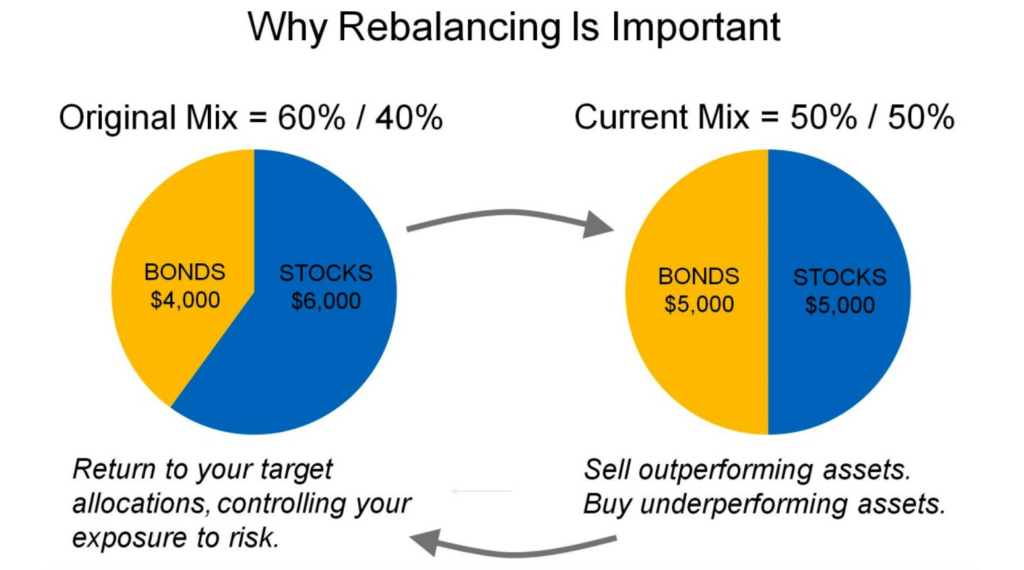

This strategy capitalizes on a correction through simple, unemotional rebalancing in which we sell winning positions and buy losing positions. When a pullback occurs in stocks or real estate, our high-quality fixed income is designed not to decline, and it often rises a little as investors scramble for safety.

At MWA, we have a twofold rebalancing methodology (threshold and time-based). We evaluate a threshold-based rebalancing trade once markets decline 20%. This trade occurs intra year at the time of the correction. We also utilize time-based rebalancing depending on tax efficiency by rebalancing accounts at annual intervals in tax-deferred accounts (or with new savings when they are placed in accounts). This unemotional rebalancing helps force us to sell high and buy low.

Here is another often-overlooked point concerning how a temporary market decline could affect the portfolio of someone who intends to work for the foreseeable future. Future savings are a big hedge to market declines. The biggest risk investors face is not a once-in-a-decade 50% decline in stocks, but rather missing a 2x, 4x, or 10x run in prices over time. These inevitable gains are virtually assured if investors can tolerate the pain of temporary short-term losses. This reminds me of a great anonymous quote: “The temporary declines are the price paid to receive the permanent ups.” Even investors who systematically invest on the worst day of the year (right before a correction) still produce attractive long-term returns, albeit a few percent lower than those who invest on the best day. The difference between investing on the best day or the worst day is pretty narrow over the long run, and the amount can typically be earned with 4–6 months added to a retirement date. I think Buffett says it best: “Corrections are when stocks return to their rightful owners.”

Let me make one last point: Taxes and turnover costs are punitive over time. I would much rather see investors stress test their portfolios along with their emotional capacity for risk so that when the bear market shows up, they readily greet it. Although their future wealth will not be realized for 2–5 years, wise investors put themselves in a position to be rewarded when they accept the fact that much more wealth is created by the actions taken (or not taken) when fear is at its highest and many investors are running for the exits.

Let me leave you with yet another Buffettism: “Investing is simple, but not easy.”

I hope this short analysis of MWA’s defensive strategy encourages you to reassess your core beliefs about how to deal with a market decline. While our approach is simple, it is “not easy,” and we have invested much thought and research into its execution.

If you would like to stress test your portfolio or revisit how much defense you might need, we are always happy to discuss this important topic with you. Remember that while US markets are rather expensive, much of the rest of the world offers much greater long-term values. Our portfolio is designed to capture returns throughout the world, not just in US markets. Sometimes diversification helps and sometimes it hurts in the short run, but it nearly always helps in the long run.

Thank you for the trust and support you have placed in us.

– Mike