College costs continue to rise, and families across the country feel the financial pressure. What once seemed manageable has become one of the largest long-term expenses for parents and students. Tuition, housing, meals, books, and other fees increase year after year. Preparing for college now requires more than just hope. It calls for a thoughtful and proactive financial strategy.

Understand the True Cost of College

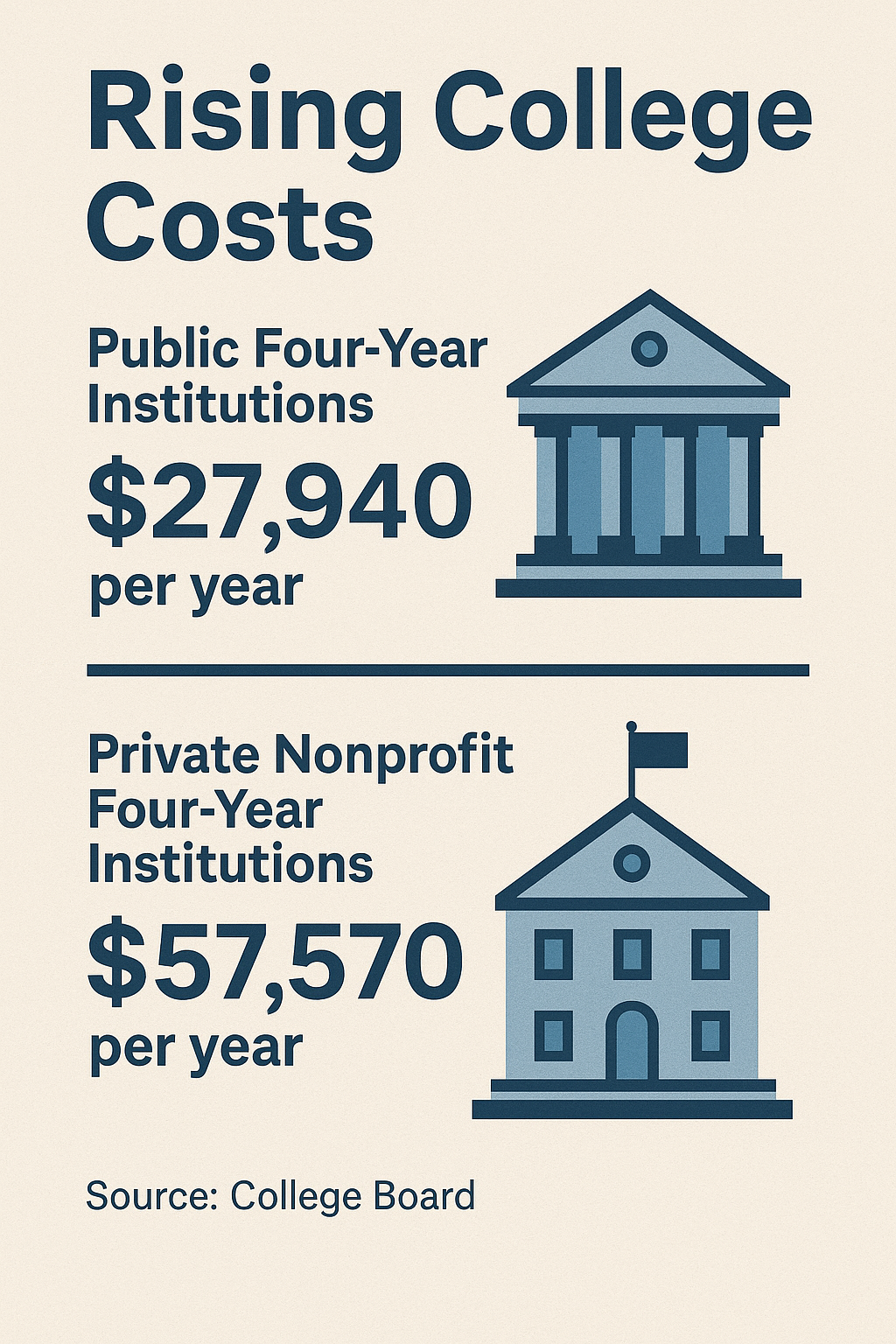

The numbers speak for themselves. According to the College Board, in-state students at public four-year colleges now face annual costs exceeding $27,000. Private universities often charge more than $55,000 per year. These totals include tuition, room and board, transportation, and personal expenses.

Over four years, a single degree can cost well into six figures. Many families underestimate the full cost or wait too long to prepare. As a result, students often rely on loans that can take decades to repay.

Recognize the Factors Behind Rising Costs

Several factors continue to drive college expenses higher. Colleges invest heavily in campus facilities and administrative staff. State governments reduce public funding for higher education. Meanwhile, demand for college degrees continues to grow.

Scholarships and grants offer some help, but they rarely cover everything. Families need to treat college planning as a core part of their financial strategy.

Take Smart Steps to Prepare for College

You can protect your financial health while planning for college. Starting early gives you more options and greater flexibility. Here are key steps to take:

1. Open an Education Savings Account

Start a 529 plan or another education-focused savings account. These accounts provide tax benefits and allow your savings to grow over time. Many states offer additional tax incentives to encourage contributions.

2. Set Clear and Achievable Goals

Decide what type of college experience you plan to support. Will your child attend a public university or a private college? Will they live at home or on campus? These choices will determine how much you need to save.

3. Maintain Balance with Other Financial Priorities

Support your child’s education without sacrificing your own financial goals. Avoid using retirement savings to cover tuition. A balanced plan helps you stay on track for both college and long-term financial stability.

4. Involve Your Child in Financial Conversations

Discuss college costs and expectations with your child. Encourage them to apply for scholarships, pursue financial aid, and consider part-time work. Shared responsibility eases the financial burden on everyone.

5. Learn How Financial Aid Works

Submit the Free Application for Federal Student Aid (FAFSA) early. Research available grants, scholarships, and work-study opportunities. Many families qualify for aid but miss out by missing deadlines or failing to apply.

Avoid the Consequences of Poor Planning

Families that delay planning often face difficult financial decisions. They may need to take out high-interest loans, postpone retirement, or struggle with unexpected expenses. Without a clear plan, college costs can disrupt long-term financial security.

College provides meaningful opportunities, but those opportunities come at a price. Families that plan early and act with intention are more likely to manage the cost successfully. When you incorporate college savings into your overall financial plan, you create more possibilities for your child without putting your own future at risk.

Education remains one of the most valuable gifts you can give. Careful planning makes that gift more accessible and more sustainable. Start early, make informed decisions, and take confident steps toward a future that benefits the entire family.